12/10/2023

I recommended selling last and then the market rallied. It was looking like I missed that call until the sell off mid week. Overall the class 3 market is in-balance, and domestic demand is good. This is normally not a sell signal but this is the holidays and should be very strong demand which is not what we are seeing. I think what we are seeing is pocket books are a little tighter after a couple of years with high inflation and consumers have cut back on there holiday spending.

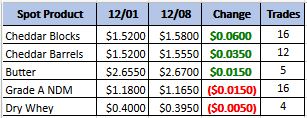

Weekly Spot Prices

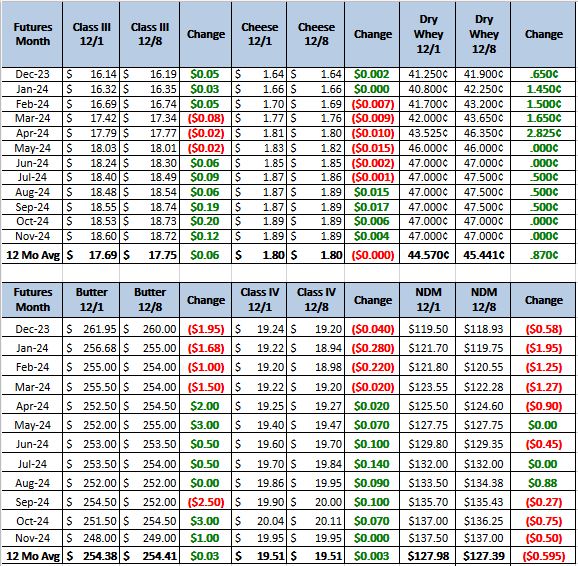

Weekly Future Prices

Cheese: Milk demand from Class III processors is steady to stronger in the East. Plant managers note production schedules and inventories are strong. Retail demand is strengthening ahead of end of year holidays, while foodservice demand wanes. Milk supplies are reportedly balanced in the Central region, where spot loads of milk were reported from $4 under Class to $1 over Class. Cheddar and Italian-style cheesemakers note demand is strong, and spot cheese loads are sparse. Cheese processors in the West relay comfortable cheese inventories and spot availability. Contacts share that while domestic and foreign cheese prices have become more competitive, recent movements have not strengthened export demand. (USDA Cheese Highlights)

Butter: Cream is mixed this week. Stakeholders in the west region report some improvement in cream volumes and spot load availability. Stakeholders in the east and central regions indicate cream supplies are tightening and somewhat available. Retail butter production schedules are strong to steady, and some butter makers have more comfortable December retail inventory levels than others. Some stakeholders indicate bulk butter and unsalted butter spot loads are tight. Domestic demand is strong to steady. Bulk butter overages range from 3 to 8 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Dry whey prices moved higher on the bottom of the range and top of the mostly price series. Some processors report being tight. They say end-of-year interests from domestic customers have kept loads moving, while others simply say they are unable to offer any extra loads outside of contractual arrangements the rest of the year. Negotiations for Q1 continue to be worked through. Milk availability is seasonally increasing for Class III processing. Contacts are waiting to see if the availability is simply a holiday-related trend, or a longer-term situation, akin to last year at this time and early in the upcoming year. Still, as high protein whey complex markets continue to firm, more whey solids are going into whey protein concentrate 80% and whey protein isolate. Animal feed whey prices increased, despite slower reported trading activity this week. All said, edible and feed whey market tones are steady to firm. (USDA Dry Whey)

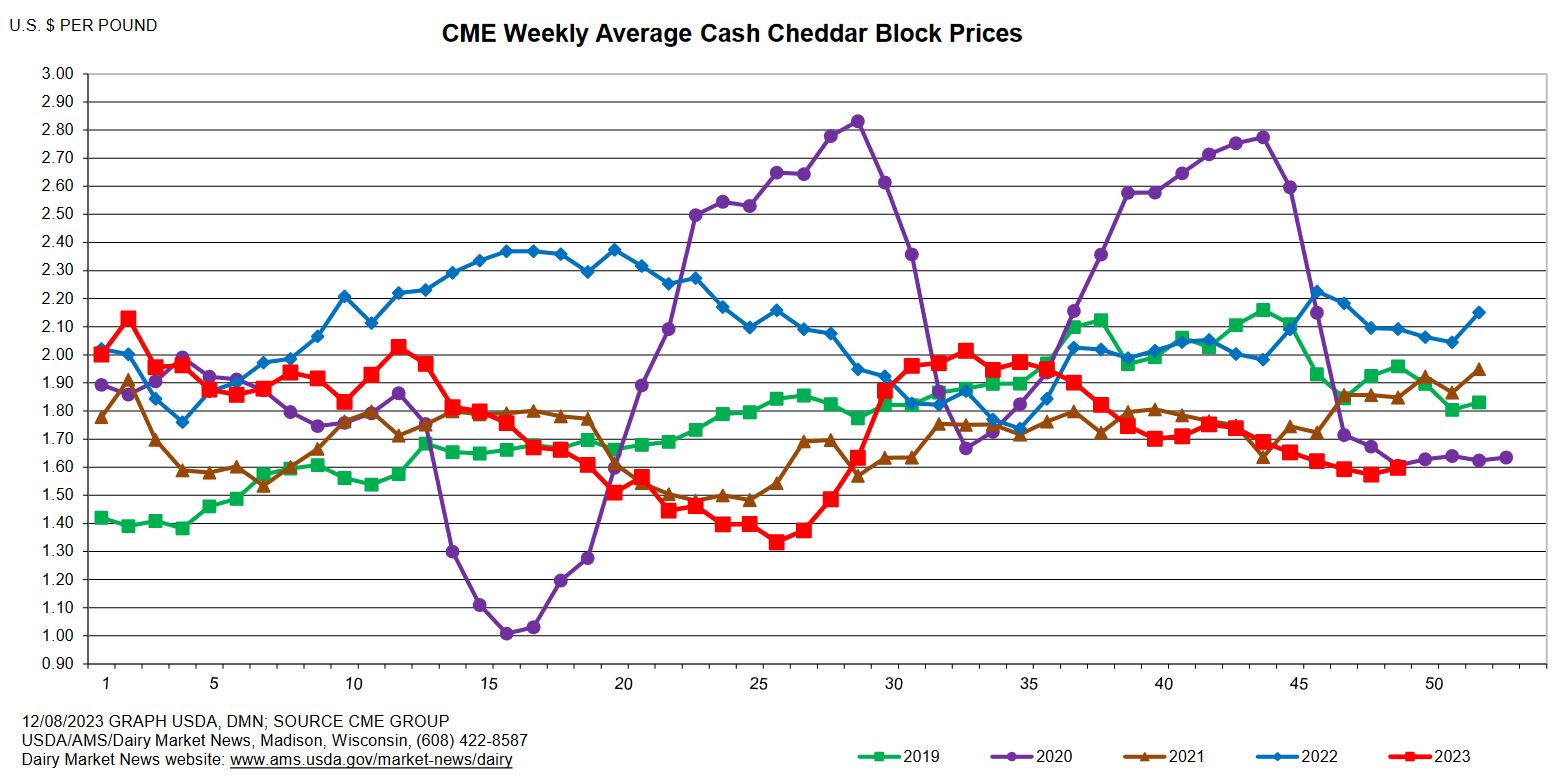

It has been one of the lowest years for block pricing in the last 5 years. If you look at the brown line for 2021 and the blue line in 2022 there was an uptick around week 44. These are the typical holiday demand bumps. This year the market did not see that. It is just a slow slide lower. So with a technical look at the graph cheese is still a sell this week. I know this is below cost of production so recommendation this week: put spread, for Jan – Apr step into the spread. Buy a 40 to 60 cent put and then move a dollar lower and put in to sell a put for 20 to 40 cent. For May – Dec buy 1800 put sell the 1650 for 40 cent.