4/14/2024

A little life on Friday. Still looking at class 3 in the 15s on spot market, but still moved higher on good volume. Currently there is enough milk for manufacturing. Although there are more reported dairies going to auction, and with high beef prices, a good number of those cows are going to beef. Demand has been lackluster this spring as the market looks for bullish news to support a rally.

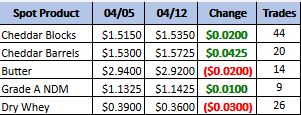

Weekly Spot Prices

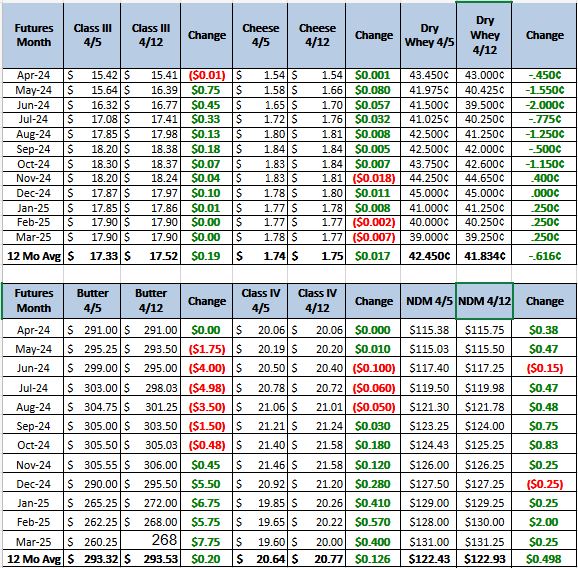

Weekly Future Prices

Cheese: Cheese production schedules are trending steady to stronger throughout the U.S. Milk production continues to trend higher in the East. Cheese plant contacts report steady to stronger production schedules as well as increases in demand. Inventories are comfortable. Contacts share foodservice demand remains light. In the Upper Midwest, farm level milk production is increasing. Spot milk prices were reported as low as $6-under Class III. Contacts say cheese plant downtime has kept milk volumes loose. Barrel inventories are comfortable. Retail demand for cheddar and Italian-type cheeses is steady. In the West, cheese production schedules are strong. Farm level milk outputs are increasing, and cheese inventories are ample. Spot cheese demand is light. Some contacts share production continued to be outpace cheese demand. (USDA Cheese Highlights)

Butter: Domestic butter demand varies across the nation. Industry participants note domestic demand is strong to steady in the West, and steady in the Central and East regions. Cream volumes are widely available throughout most of the country. Butter manufacturers continue busy churning schedules overall, while cream volumes are readily available. Some butter makers convey non-contracted unsalted butter loads are tight and more actively sought by spot buyers. Although many manufactures are working to build inventories, some processors in the Central region convey an expectation of lighter churning over the next few weeks. Bulk butter overages range

from 3 to 13 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Prices contracted slightly for the range. The bottom end of the mostly price series is unchanged and the top end of the mostly price series moved lower. Plenty of liquid whey is available for drying with busy cheese manufacturing schedules. Dry whey production schedules are noted as strong to steady. Healthy demand and good markets for higher protein concentrates are drawing some liquid whey away from more robust sweet whey production schedules and into higher protein concentrate production schedules for some processors. Domestic demand for dry whey is steady. Buyers indicate availability of sweet whey loads is neither overly tight no (USDA Dry Whey)

With enough milk for manufacturing and price holding in the 15s this market need a kick to get dairy balance sheets out of the red. There are continued reports of dairies going to action but those are mostly in the south west and on the west coast. These tend to be areas that split there production between class 3 and class 4. That is a big reason for butter holding up close to $3. When summer heat hits milk should tighten with the lower cow numbers. The question is will demand hold or increase to give the class 3 market the kick it needs to push price up. Recommendation buy puts on what you need to still cover for this year. Anything you have sold look for calls on pull backs. This market looks to be a bumpy ride which should give opportunities to cover either side. As grilling season gets going I expect the overall direction to be bullish.