4/7/2024

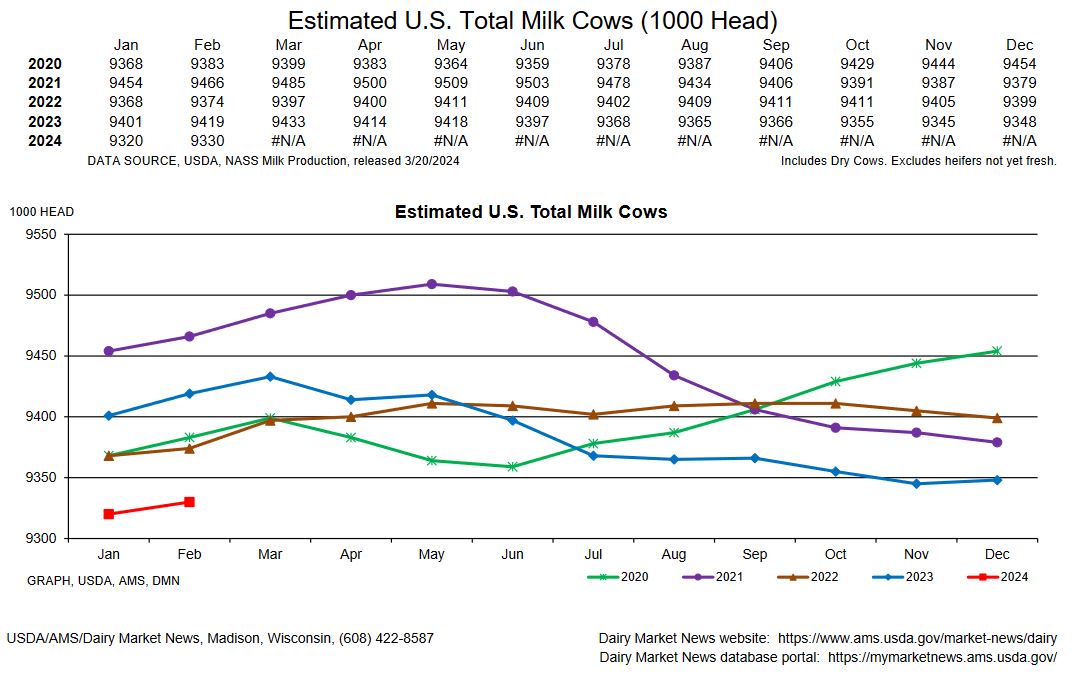

It has been a couple of weeks from my last report. Easter is now in the rear view mirror and there is only one more game left for college basket ball. Domestic demand is running steady with a little uptick on pizza cheese. The last production report showed an increase in cow numbers which has weighed on the market this last couple of weeks. I do not think next months will continue that trend. The price on beef has kept the cull rate strong and with more dairies going to action the herd should shrink in size. Spring flush is on in most of the country and cheese plants are running at full schedules. There was some good news at the end of this week as buyers returned to the spot market and drove the prices on blocks and barrels back up. Still looking for sustained demand to say that this market has turned a corner and is ready to head higher.

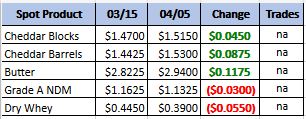

Weekly Spot Prices

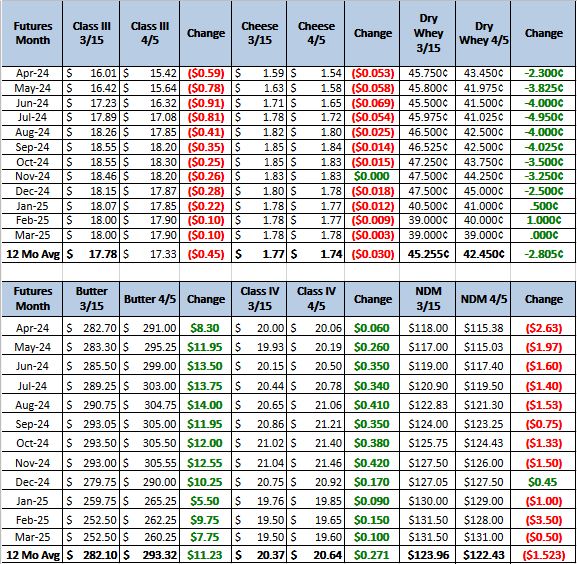

Weekly Future Prices

Cheese: Eastern contacts share milk production continues to trend steady to higher. Cheese plant contacts note steady to lighter production schedules, citing weak block cheese demand as a reason to scale back cheese processing. Block cheese inventories remain comfortable in the region, namely of American-type cheese varieties. Cheesemakers in the Central region share ample milk availability has kept production schedules in line with recent weeks. Contacts note plant downtime and the recent holiday weekend have loosened already abundant milk volumes. Spot milk prices were reported at $5 to $3-under Class III. Cheese manufacturers in the West share robust cheese production schedules. Contacts share that contracted cheese demand is steady. Spot demand is steady to stronger, as is demand from international purchasers. (USDA Cheese Highlights)

Butter: Domestic butter demand varies some region to region. Industry participants convey domestic demand is strong to steady in the West, steady in the Midwest, and steady to lighter in the East. Cream volumes are reported as widely available and at comfortable amounts. Butter manufacturers continue to run busy production schedules overall while cream volumes are seasonally larger. However, whether butter makers indicate churning is focused on immediate retail needs or building bulk butter stocks varies. Planned summer churn maintenance is noted by some butter manufacturers. Stakeholders, in the West region particularly, relay unsalted butter spot load availability is tight. Bulk butter overages range from 3 to 12 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Dry whey prices are unchanged for both the range and mostly price series. Domestic and export demands are steady. Busy cheese manufacturing is supplying plenty of liquid whey for drying. Dry whey production schedules are strong to steady. However, some manufacturers indicate production has been lower compared to the prior year. Industry participants convey varied spot load availability. Some manufacturers say spot load interest is on pace with production, while others say production is staying ahead of

spot load interest. Stakeholders indicate west region inventories are comparatively tighter than the neighboring central region. Sweet whey market tones are firmer. (USDA Dry Whey)

Cow numbers gains from January to February are typical but with lower future prices, a tight heifer supply, and high beef prices I do not expect to see the typical gains in cow numbers continue. With that said there is still a demand problem. The Asian markets are still weak and exports to Europe are below previous years. We are still looking for a little more demand to swing the pendulum in the positive direction. Recommendation, Put spreads as I feel the down side it limited. August to September buy the 1800 put sell the 1700 put for 35 cents, and if the front months make a run over 1750 look to lock in 1700 puts.