3/17/2024

A little life in class 3 this week. With the news of a virus drying up cows in Texas class 3 futures took a run higher. From what we have heard the virus is effecting 10 to 15 percent of the herds it infects and after a month 5 percent of the cows do not come back and need to go to beef. This on its own would not have much effect on the overall market but combined with the financial damage dairies are sustaining this year it could further tighten up the milk available for class 3.

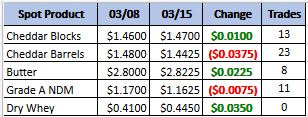

Weekly Spot Prices

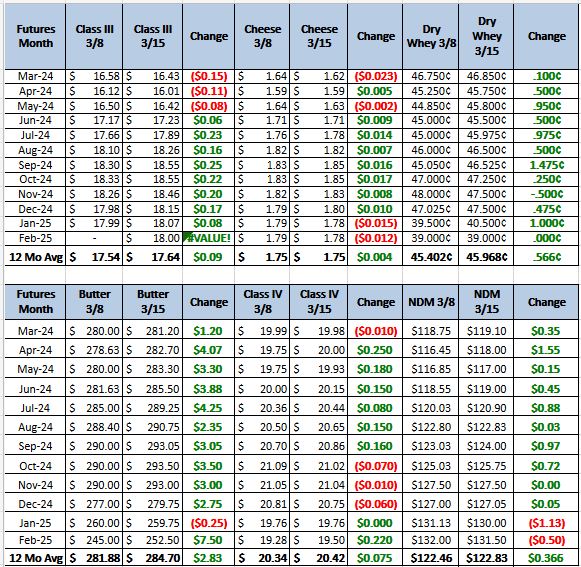

Weekly Future Prices

Cheese: Farm level milk production continues to grow in the East region. Contacts share Class III spot milk demand is growing as spring holidays inch closer. Contacts share cheese inventories are ample. Barrel demand has dropped, and the block/barrel inversion on industry cash exchanges resolved as a result. Retail demand is steady to stronger. Demand for cheese in the Central region is growing. Contacts suggest increased demand is due to both bearish cheese prices as well as seasonal holiday demand. Milk availability is growing, and cheese production schedules are steady. Spot milk prices range from $3.50-under to $.50-over Class III. Cheese inventories are noted to be generally available. Retail demand in the west is noted to be weaker to trending flat. Class III milk is readily available for cheesemakers in the region. Processors are running steady production schedules, and inventories are noted to be ample. (USDA Cheese Highlights)

Butter: Retail demand is strong to steady across the country. However, demand to secure loads for upcoming spring holidays vary. For the West, contacts note earlier spring holidays are encouraging more consistent Q1 activity. For the Central, contacts note customer interest has been slower to pick up ahead of the spring holiday season. Some stakeholders say food service is weakening in the West region. Some distributors indicate buying interest is stronger from Canadian purchasers. Cream remains readily available for most of the nation. Butter

makers are running strong to steady production schedules. However, tight unsalted spot load availability through Q2 is noted by some manufacturers. Bulk butter overages range from 3 to 12 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Dry whey prices are unchanged for both the range and price series. Some index-based spot prices held the top end of the range steady. Stakeholders note domestic demand is weaker and trading is quieter this week. Demand from international buyers is steady to lighter. Industry sources indicate earlier 2024 Q1 year-over-year comparing shows an increase in export demand. A few manufacturers convey bleached dry whey and Grade A dry whey are somewhat tight for spot buyers. Processors relay steady production schedules. Some plant issues in other regions continue to limit capacity for sweet whey production nationally. Stakeholders indicate this

has contributed to tighter dry whey spot load availability. (USDA Dry Whey)

The class 3 futures as moved higher but the spot market has not. With futures trading at such a premium to spot the logical thing to do is to protect the down side in case spot stays at that level and drags down the futures. With the amount of damage these prices are doing to the average producer I am going to recommend the opposite. Recommendation, buy calls, start in May and go out to the end of the year. There still is some needed demand as there is plenty of cheese around at this point, but production is dropping as cow numbers continue to drop and when demand finally out paces supply price will head higher.