12/17/2023

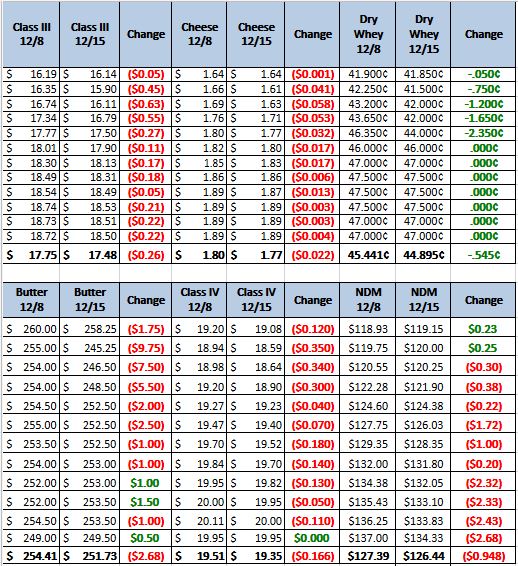

New lows in class 3 this week on the futures as the blocks and barrels moved lower on Friday. Holiday demand has not tightened up the cheese this year and some extra loads have been making their way the the cme spot market. January ended the day on Friday putting in new lows for futures contract. This is all bearish news and technically class 3 is still a sell at this point.

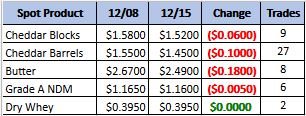

Weekly Spot Prices

Weekly Future Prices

Cheese: Spot milk demand remains strong in the Eastern states. Plant contacts report robust production schedules with inventories growing week over week. Retail demand is strong ahead of end of year holidays. Contacts note mozzarella and cheddar demands are especially strong. Cheesemakers in the Midwest report ample milk availability, with Class III spot milk prices ranging from $4-under to $1-over. Production schedules remain steady. Demand for cheese barrels has softened. In the West, cheese processors have shared their inventories are comfortable. Spot availability is variable, though, as contractual obligations are being fulfilled before the end of the year. Domestic cheese prices have become more competitive with international prices, but industry sources share export demand has not yet picked up in response. (USDA Cheese Highlights)

Butter: Domestic retail butter demand is strong to steady in the lead up to the winter holidays. Cream supplies for churning remain mixed. Stakeholders in the west and central regions indicate spot loads of cream are more available. However, contacts in the eastern region indicate spot loads of cream for butter churning are tighter than in recent weeks. Butter makers anticipate milk clearing to Class IV to increase in the second half of December. Manufacturers report strong to steady retail production schedules. Some stakeholders indicate

spot loads of unsalted butter are somewhat looser. Bulk butter overages range from 1 to 8 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Prices contracted slightly for the range and moved lower on both ends. More activity from spot buyers contributed to an increase on the bottom of the price range. Demand is steady domestically. Amongst spot purchasers, baking manufacturers are more seasonally active. Export demand is moderate. Some stakeholders relay sentiments that declining pig herd sizes in Asia is negatively impacting overall demand from international buyers. Production is steady with liquid whey volumes meeting drying needs. That said, a comparatively stronger whey protein concentrate market is incentivizing some manufacturers, who can shift over to whey protein concentrate production, to do so. A few manufacturers indicate spot load inventory is somewhat tight. (USDA Dry Whey)

The graph above has tells the story of the class 3 through the holidays this year. There have been a couple of rallies that have sputtered out and the over all market has been bearish going through the holidays. Lack of demand has been the over all theme this season and this last year. The question at this point is where is the bottom. As we are below cost of production for most producers I hesitate to suggest selling but graph says sell. On a more positive note, cold storage has not grown which means production and demand is relatively in balance. The world prices are higher then the US which could lead to more exports. Recommendation, sell and then as we move into the first quarter look to cover all your sold contracts with calls.