12/3/2023

The Cheese market has turned more negative in recent weeks as the holiday buying period has not produced a rally. Overall cheese is relatively in balance. Cold storage came down a little last month but was up over last year. Production is lower and cow numbers continue to come down. These are all things that should be pushing the market higher. Inflation has taken a big chunk out of the consumer and it has also weakened cheese demand.

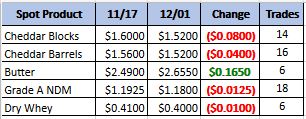

Weekly Spot Prices

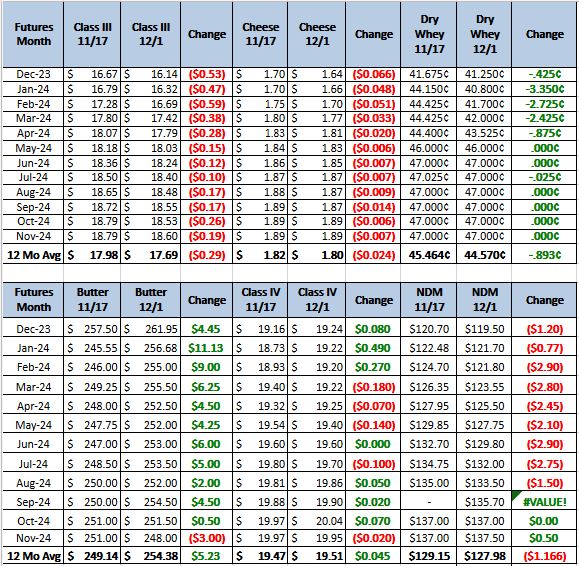

Weekly Future Prices

Cheese: Milk volumes available for cheese processing are ample in the East. Plant managers relay production schedules are steady, though demand has plateaued. Retail demand is noted to be steady, but contacts noted food service demand continues to be lackluster. In the Central region, milk prices have bounced back from the Thanksgiving week, ranging from flat to $1 over Class. Cheese demand is holding a steady pattern, and contacts share surplus loads of cheddar are generally spoken for. Barrel quantities have increased. In the West, Class III demand is steady to stronger for cheese processing. Spot milk availability ranges from strong to abundant, though some plant managers relay cheese production schedules are below capacity. Retail cheese demand continues to outpace food service demand in the West. (USDA Cheese Highlights)

Butter: Cream volumes are reported to be tighter in the eastern region compared to the central or western regions. Cream is indicated to be widely available in the central region, while processors in the southern part of the eastern region indicate not quite tight but not ample cream volumes. Butter production was mixed during the recent holiday weekend with some butter makers running busy production schedules and others slotting in some downtime. Plant managers relay strong to steady post-holiday weekend production schedules. Many manufacturers note comfortable December retail inventory levels. A few western butter makers relay availability of unsalted butter spot loads will be tight for the remainder of the year. Domestic demand is mostly steady. Bulk butter overages range from 3 to 10 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Prices moved higher on both ends of the range and mostly price series. Steady domestic demand has picked up again following the holiday weekend. Activity from spot load buyers for nonpreferred and preferred brand loads improved. Although demand from ice cream manufacturers is seasonally lower, demand from baking manufacturers is seasonally higher. Demand from international buyers is moderate. Some stakeholders suggest declining pig herd sizes in Asia have negatively impacted U.S. dry whey export demand, but

continuing preparations for a large yearly Asian celebration may improve export demand. A few manufacturers note inventories for spot load buyers are on the tighter end. Dry whey production schedules are steady with ample amounts of liquid whey from strong to steady cheese production schedules. (USDA Dry Whey)

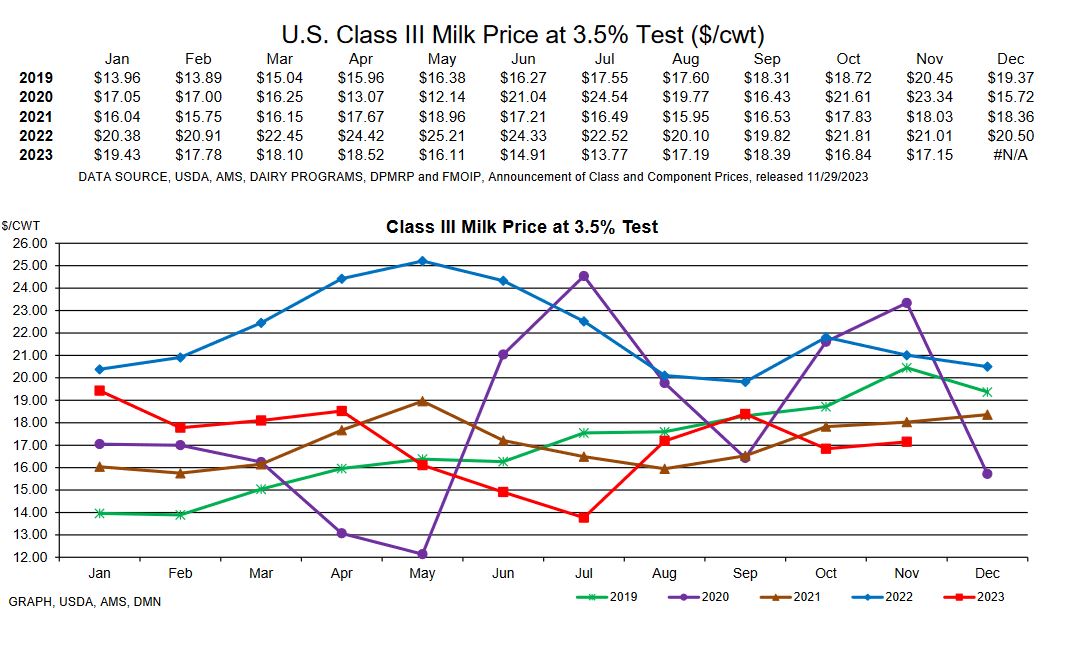

It is looking a little bearish for class 3. The economy is rolling along pretty well. People have jobs going into this holiday season but it just has not translated into spending. Part of this is inflation, so those pay checks do not go as far. There is also a mental side, consumers are not optimistic about where their finances are and for the future. This has all lead to some cutting back and restaurant traffic has seen a drop this holiday season where it typically gets a bump. Recommendation, sell. It is time to get covered for the first half. There could be some rallies so buying calls to cover your sold positions is a good idea, but the direction in the market is down so technically it is a sell.