4/28/2024

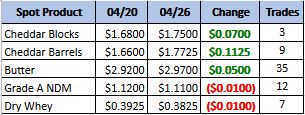

Spot market continued to push higher this week as spot cheese got into the mid 1.70s. From reports domestic demand has picked up heading into grilling season. Exports to Asian countries have been slow this year but the peso has gained on the dollar and Mexico has had strong demand.

Weekly Spot Prices

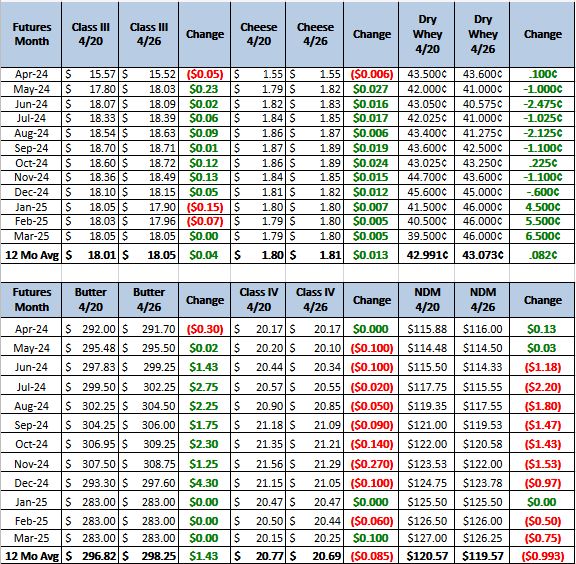

Weekly Future Prices

Cheese: Cheese production schedules are trending steady to stronger throughout the US. Some Eastern cheese plant contacts share that seasonally strong milk availability has enabled steady cheese production. Cheese inventories in the area are comfortable, but demand has increased in recent weeks, as have prices for both blocks and barrels on the CME. Foodservice demand is light. Retail demands in the region are steady to higher. Central area cheese manufacturers share, too, notable increases in cheese demand. Curd, cheddar, and Italian-style cheese demands are all stronger than in recent weeks. Spot milk prices were reported at $5- to $1-under Class III. Cheese manufacturers in the West note strong cheese production. Milk handlers share milk availability is adequate to meet processing needs. Contacts share cheese inventories are available for spot purchasers. Western contacts say demand from domestic buyers is steady to moderate, while international interests are quiet. (USDA Cheese Highlights)

Butter: In the West region, domestic butter demand ranges from slightly higher to slightly lighter compared to the week prior. However, domestic butter demand is unchanged for the Central region. In the East region, foodservice demand is unchanged, and retail demand is following seasonal expectations. Cream is widely available throughout the country, and some butter manufacturers convey securing additional cream volumes. Butter makers are running busy production schedules and continue to build bulk butter inventory for late summer and fall needs. Some stakeholders note unsalted butter loads are tight. Bulk butter overages range from 2 to 10 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Prices moved lower for both ends of the range and mostly price series. Busy cheese manufacturing is keeping liquid whey readily available for drying. Dry whey production schedules are steady. Some manufacturers have committed most of their anticipated remaining Q2 production to already established obligations during Q2. However, dry whey loads are available for spot buyers’ needs. That said, stakeholders indicate loads produced in the Central region and clearing into the West region have been slightly more frequent during April. Domestic demand varies from steady to moderate. Demand from international buyers is moderate. (USDA Dry Whey)

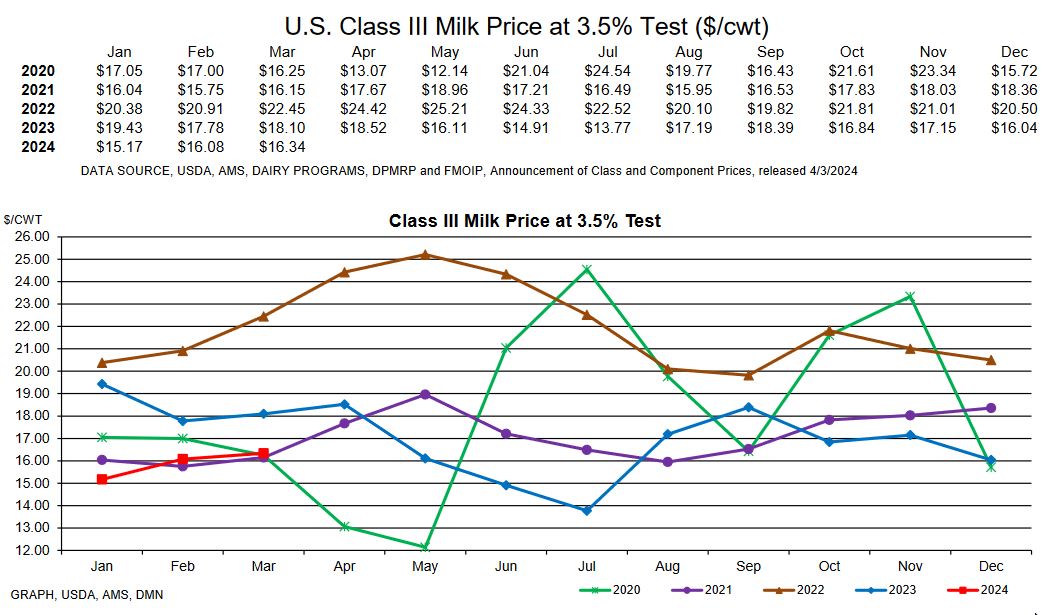

Demand is overall lack luster for the first quarter of this year and that has done some damage to dairy producers. Production report has cow numbers down 71 thousand head from last year as of the end of March. At this point it looks like it will be May before producers shipping to class 3 plants will see a break even pay check. I expect to continue to see the dairy herd shrink until $18+ checks hit mail boxes. With that said there is still enough milk to meet manufacturing needs. This will be a bumpy ride but we should see higher numbers as we move forward. Recommendation, Buy call on pull backs, $1900 calls for 50 cents Jun-Aug 2024 then look to sell $2100 call for 30 on a rally for those same months.