4/21/2024

Good rally this week as the class 3 market pushes into the 18s for most months left in 2024. Friday had the strongest showing in the spot market with blocks moving 7 cent higher and barrels 5 cent higher. This pushed May future’s price into territory that we have not seen since late February. At this time cheese has not gotten tight, but the dairy herd is shrinking, and buyers maybe jumping in before that eventually happens.

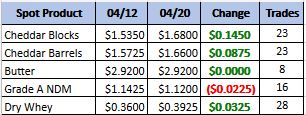

Weekly Spot Prices

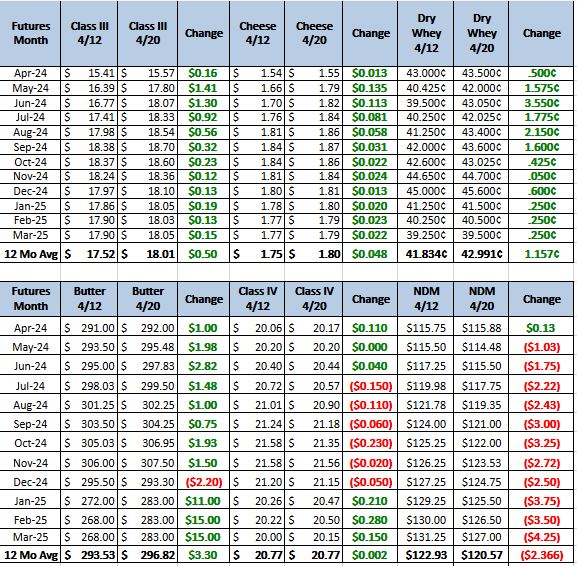

Weekly Future Prices

Cheese: Production schedules across the U.S. are generally steady to stronger. In the Eastern region, cheese plant contacts report seasonally steady production schedules, supported by strong milk production and ample cheese inventories in cold storage. However, light foodservice demand contrasts with steady to stronger retail demand as grilling season approaches. In the Central region, cheesemakers note an increase in curd demand compared to the same period in 2023, with comfortable cheese inventories. Spot milk availability is not as abundant as in previous weeks, with spot milk prices reported slightly below Class III prices. In the West, cheese manufacturers maintain robust production schedules, with adequate inventories to meet both contractual and spot needs. Regional spot demand is described as moderate, while demand from international buyers remains steady to stronger. Despite this, some processors highlight that cheese production continues to outpace demand. (USDA Cheese Highlights)

Butter: The demand for domestic butter varies across regions. In the Western region, demand is mixed, with some industry stakeholders observing diminished interest in retail and bulk purchases from buyers. In contrast, in the Central region, demand remains stable. In the Eastern region, reports indicate a consistent demand for retail products and a seasonally elevated demand for foodservice applications. Stakeholders consistently report ample cream volumes available nationwide. Butter manufacturers generally experience robust churning activities, with production occurring for both salted and unsalted varieties. Nevertheless, several industry sources note a constrained availability of unsalted butter loads. Bulk butter prices typically exceed market rates by 2 to 13 cents across all regions. (USDA Butter Highlights)

Dry Whey: Prices moved lower on the top of the price range and top of the mostly series this week. Some preferred-brand, single-spot-load trades, which have kept the top of the range intact over multiple recent weeks, were not reported this week. Additionally, the active trading pricing window has shifted from the low-$.40s to the middle/upper-$.30s. Some processors say they are not seeing inventory levels rise compared to previous months, but market pressures have pushed them to make necessary adjustments in order to move volumes. End users say offers are steadily incoming. Some are still finding values on high-protein blends, nonetheless dry whey

trading activity was somewhat busy this week. Animal feed whey trading was quiet, comparatively, but steady when compared to feed whey activity in previous weeks. (USDA Dry Whey)

With class 3 prices pushing back into profitable territories hedging is starting to look a little better than it has in recent weeks. As far as we know at this time cheese is not tight and there is plenty to fill current demand. That said cheese in the 1.60s is not going to scare of any buyers as it still is the cheapest in the world. Recommendation, buy 1700 puts for 30 cents average, May – Nov 2024. Then look to sell the 1600 puts in those same months for 20 cents average on a pull back in the market.