09/04/2020

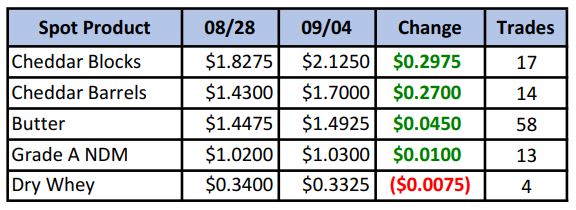

Another week, another headline, another major move in spot markets, this time to the upside. There is plenty of cheese in the country, but when the government issued real Section 32 solicitations for cheese on Tuesday, suddenly the sellers didn’t have any. Block bidders tried mostly in vain to shake loose some product, with only mild success. The week’s gains put blocks back above $2/lb.

Spot Market Recap

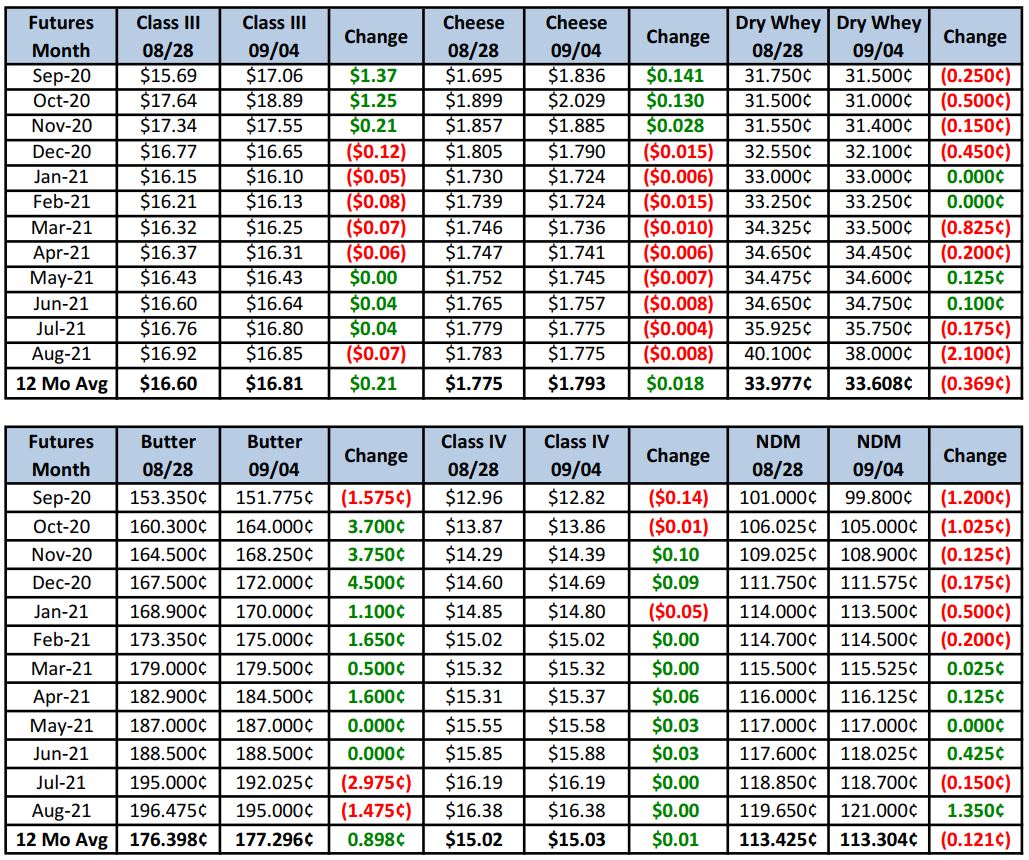

Futures Recap

Sep and Oct Class III futures saw the largest gains, as they will benefit the most from this short-term demand binge. That said, intra-day price action continues to show wild swings. Wednesday through Friday saw spot blocks add more than 30¢ to it’s price, but after peaking at $19.64 on Thursday, we hit a low of $18.45 on Friday. After both spot sessions, sellers seemed to tap bids aggressively. There is a real lack of belief in this current rally, and maybe they’re right.

Dairy cow slaughter remains in the dumps, with this week’s total down 9% compared to the same period a year ago.

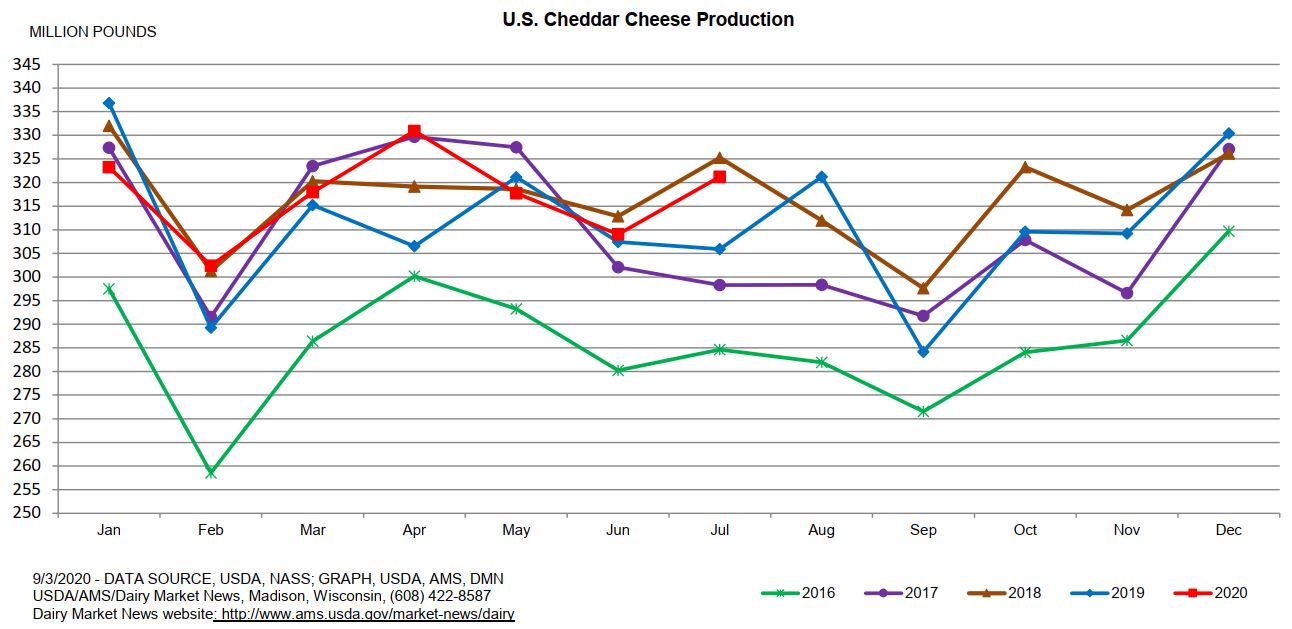

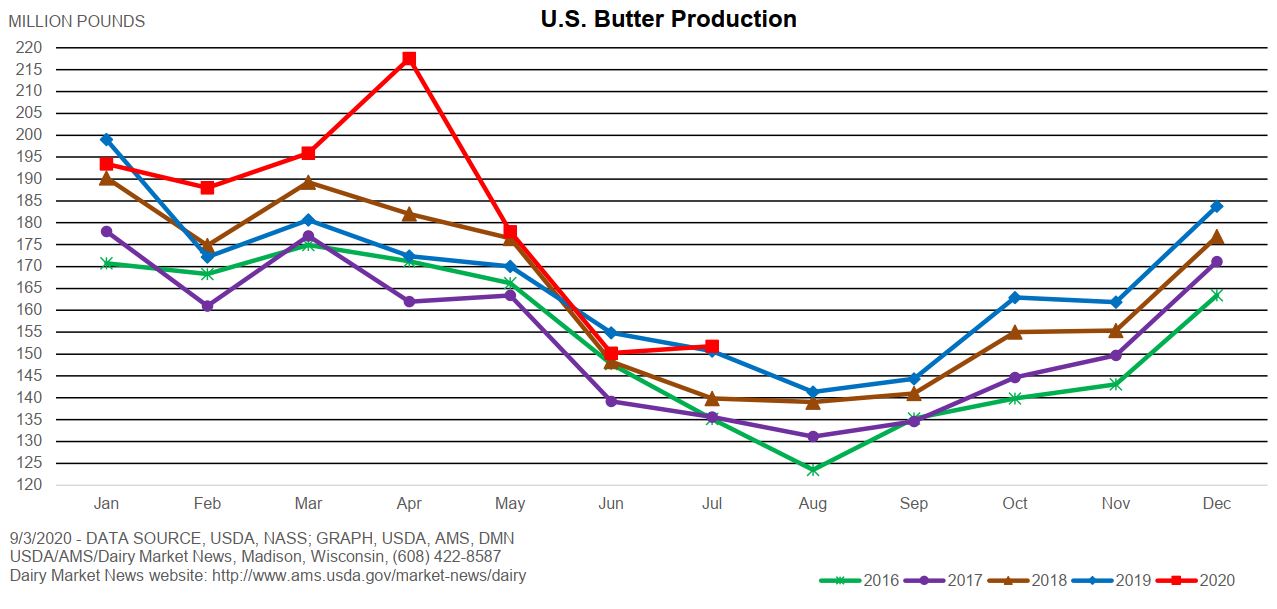

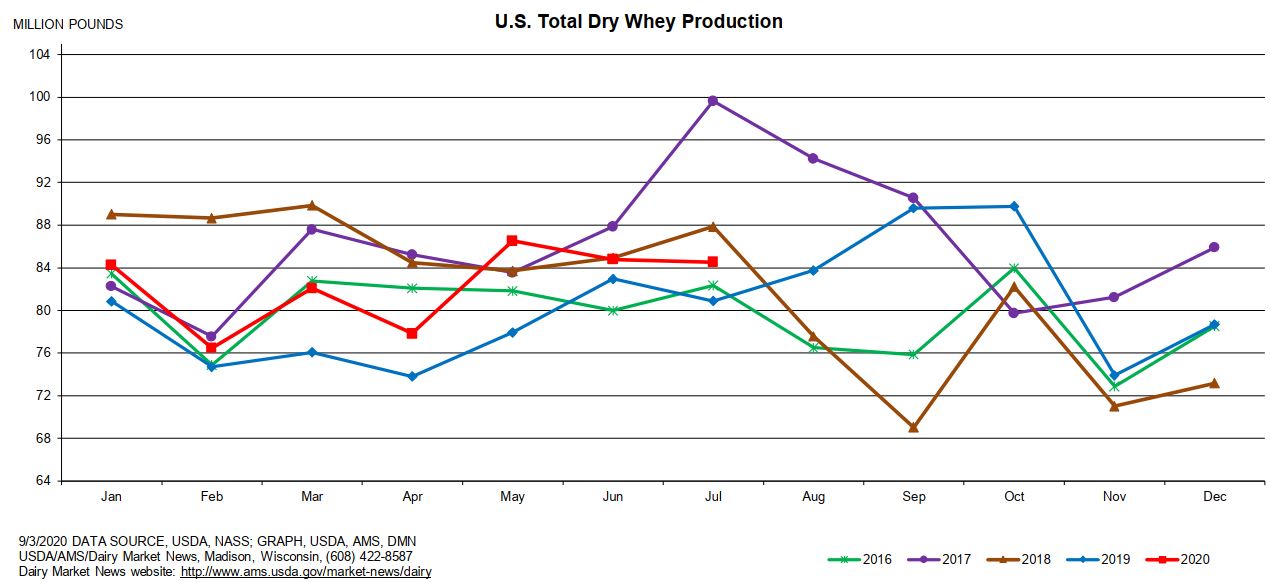

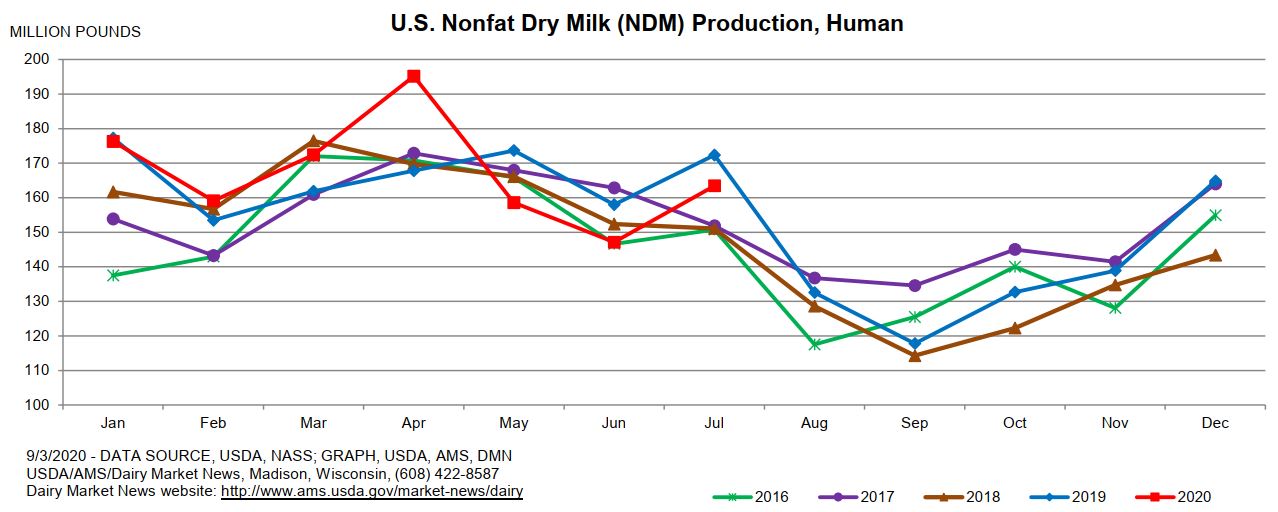

The Dairy Products Report was released this week; cheddar cheese output in July was up 5% YoY while total cheese output increased 1.8% Butter production was just 0.7% higher than last July, dry whey output up 2% and NDM output fell 5.2%.

Butter stocks surged, however, a full 13% higher than year ago levels, helping explain some of its current price weakness.

Dairy Market News reports milk output in the Northeast is mainly flat, but supplies are tighter in the Southeast due to heat. Cooler weather in the Central region has cows happier, with increases in yields expected. In the Southwest, milk remains tight in California and Arizona due to recent heat, but output remains heavy in the Pacific Northwest. There is plenty of milk to make cheese, however, with the significant drop in fluid needs from schools, moving into manufacturing streams. Cream for butter output is becoming more available as draws from ice cream manufacturers wanes. Inventories are starting to build again. Demand for cheese is up with buyers looking to fill government contracts. NDM in parts of the country is committed through Q4 and supplies are beginning to tighten. Demand is good for cheese fortification, while bakery demand is reported as good.

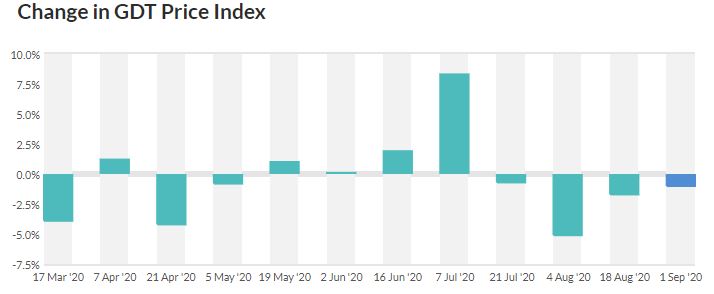

On the international front, The GDT Dairy Price Index fell 1% this week, marking the fourth consecutive decline in the twice-monthly auction.

New Zealand is off to a fast start in their new milking season, but a souring relationship between Australia and China has cancelled a Chinese-led purchase of an Aussie dairy processor. There are worries over a retaliatory trade war beginning, which could result in China seeking dairy products elsewhere. Finally, late summer heat in the EU has curtailed growth in milk output on the continent.

There was some good news on the export front. U.S. Dairy Export Council reported July dairy exports jumped 23% compared to a year ago. Most of the growth was seen in NDM/SMP shipments to Southeast Asia, which climbed 52%. Cheese exports were up 5% while total whey exports increased 30%. Total dairy exports were equal to 16.9% of total U.S. milk production in July, vs. 14% a year ago.

The sell-offs after this week’s gain in the spot market means there is a lack of belief that current demand will last very long. Last week we put in targets for Oct – $18.50, Nov – $18.00 and Dec – $17.50. Both the Oct and Nov hit those targets this week. While October looks like it could continue to move higher next week if spot bids persist, the November sold at $18 is looking like a good hedge so far. Were it not for the government injection of demand, we feel markets would have continued grinding lower as excess milk from lack of school demand and much lower culling has resulted in very available milk supplies. Hedgers should continue to view strength in the markets as a gift and look to get hedges done in Q4 and Q1 2021. Target Q4 at $18.60 average (which very nearly hit this week).

We expect more volatility next week as there is so much unpredictability right now. How long with government buying last and how much? Will COVID-19 get behind us sooner or drag on? Will schools be in full attendance mode by Jan 1? Will global economies continue to pick up and increase export demand (looking good so far). All of these questions make it very difficult to predict for the long term.

Have a great weekend!