08/28/2020

Spot cheese prices look like they may have bottomed out as they bounced back to levels about equal to two weeks ago. Just when most fundamentals were pointing more bearish, the government announced on Monday afternoon that they would be pumping in an additional $1 billion into the Food Box program, and it would be spent by the end of September. Futures raced higher Monday and Tuesday, but then gave up much of those gains as they sputtered the rest of the week.

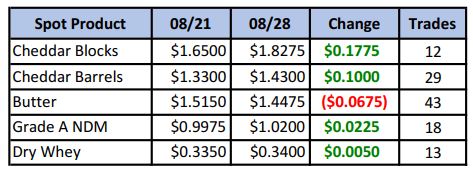

Spot Market Recap

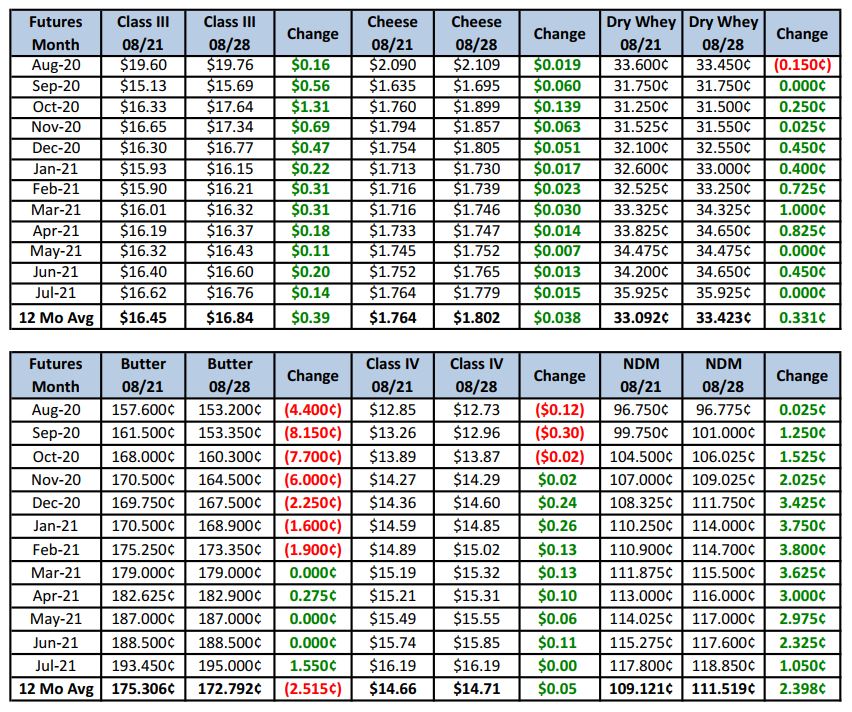

Futures Recap

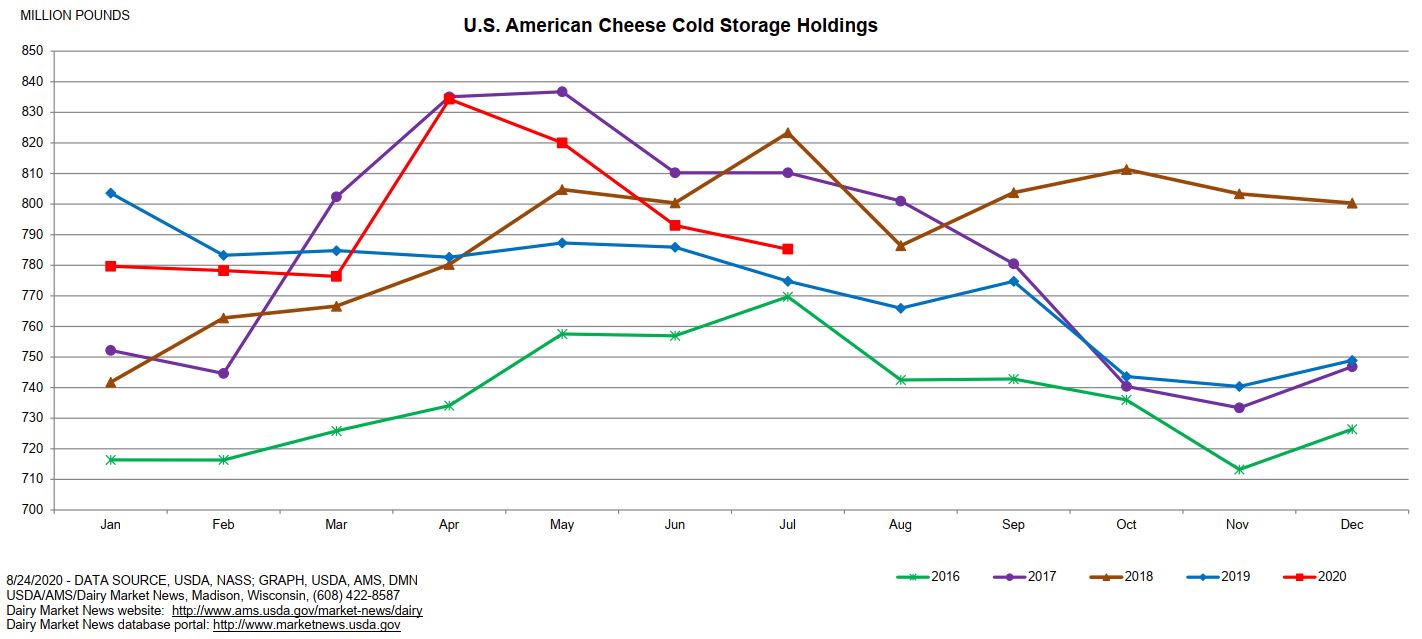

Only one major report out this week, the Cold Storage Report was released on Monday. American cheese stocks at the end of July were 2% higher than in 2019, but below 2017-2018 levels.

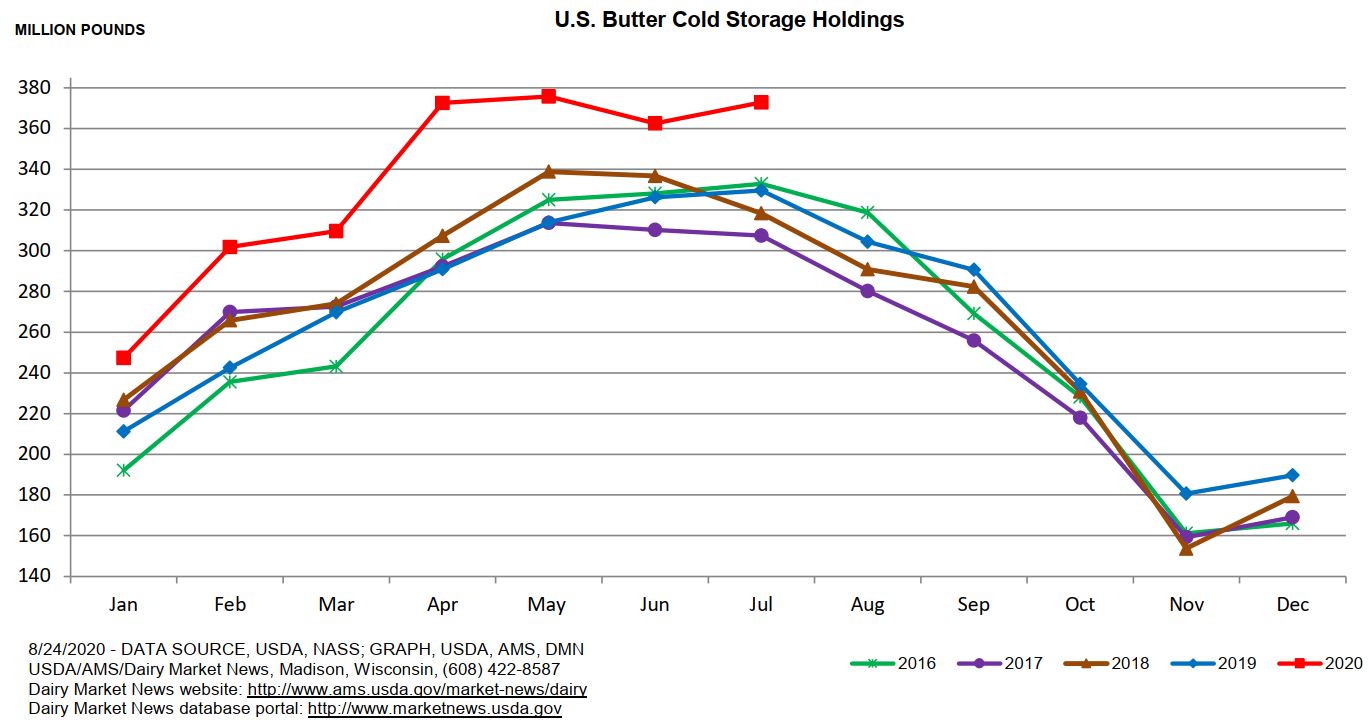

Butter stocks surged, however, a full 13% higher than year ago levels, helping explain some of its current price weakness.

The report had minimal affect on the market as the government headline held the dominant role. We’ve heard reports of increasing cheese orders following the news, but the spot market did little to reinforce the sentiment. After peaking at $1.8725 on Wednesday, blocks retraced the rest of the week. Barrels made less of a move, but nonetheless gave back ground after peaking on Thursday. During each session, cheese offers were much more prevalent, sometimes 4-5 deep, with very few, if any bids. Likewise, most of the trade volume occurred during the last minute of spot trade. Perhaps we’re just consolidating, but the technical action certainly didn’t feel bullish.

Dairy Market News reports fluid milk output in the Northeast is stable, with all classes of milk receiving stable volumes. Hot and humid conditions in the Southeast are tightening the milk supply. Most milk loads are clearing to Class I, with some milk being imported into the region. Cream availability is tighter, with demand higher than current supply. Triple-digit heat in Texas is causing a decline in milk yields, but in the Midwest, with lighter Class I demand, manufacturers are receiving plentiful milk supplies. Spot loads in the Central region continue to trade at a discount to class. Heading West, the recent heatwave in California has caused a decrease in milk output, with several plants now saying they have extra processing capacity. Arizona as well has been affected by the heat, but the milk supply is mostly in balance with needs. Milk production in the Pacific Northwest remains strong, with some plants in Idaho struggling to keep up with the supply. Spot loads in the state are available at $5 under Class IV, with some distressed loads even lower.

Butter output across the country is lighter with the generally tighter cream supply, but most market participants are not that worried, due to the large amount of butter in inventory. Most buyers believe they will be able to secure what they need for fall/holiday needs and thus see little incentive to buy ahead.

Dry whey prices have slid a bit across the country. With less milk heading into school lunch programs, cheese production has remained elevated, increasing the whey supply. Buyers expect inventories to remain available.

NDM prices have improved as inventories have tightened a bit in some regions. Some processors are drying less, while demand from bakers and cheese manufacturers continue to take consistent loads. International interest has also picked up, especially from Mexico.

Cheese sales in the Northeast from the food service sector are softer as restaurants continue to struggle. Inventories are growing in some storage facilities. In the Midwest, cheese demand varies from steady to busier. However, some producers say orders are slowing and inventories are growing, though not yet burdensome. Western cheese plants report the barrel supply is loose, but blocks are tighter. Cheese is moving well, but retail orders are cooling and food service sales are still slow. With ample milk supplies, cheese plants are running at or near capacity.

The best way to describe this week’s market is whippy. After writing a fairly bearish report last week, fundamentals remain largely unchanged, except for the government aid announcement. It goes to show how big an impact that single factor can be, and is totally unpredictable. Forecasts for a quick move to $2 blocks never materialized, leading to choppy price action the rest of the week. Today’s settlement was solidly in the green, however, so perhaps spot buyers will get more aggressive next week. At this point, it’s a complete guess though. Our best advice for producers would be to set some high targets in Q4 for any unprotected milk and see if they hit. With daily ranges hitting over $1 from low to high this week in some contracts, you never know when one of your resting orders might get filled. Consider sales of Oct Class III at or near $18.50, Nov at $18.00 and Dec at $17.50.

Have a great weekend!