09/11/2020

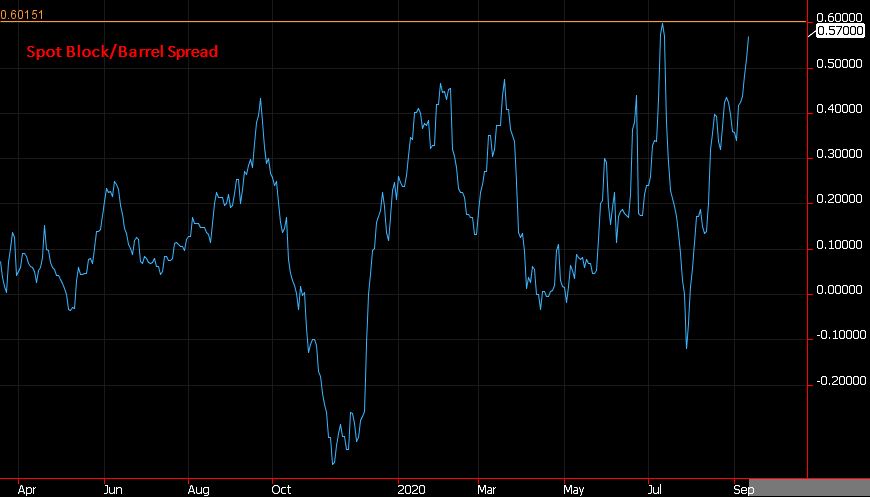

Block cheese found support this week as government food programs gave buyers confidence to bid for physical product, but barrel cheese couldn’t gain any traction off the news and went the other direction. Their divergent paths put the block/barrel spread at 57¢, perilously close to the all-time record wide spread set just this past July at 59¾¢. And as one can see from the chart below, wide spreads don’t last for very long.

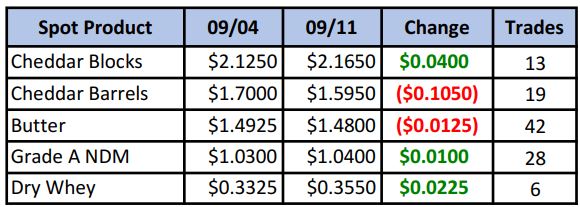

Spot Market Recap

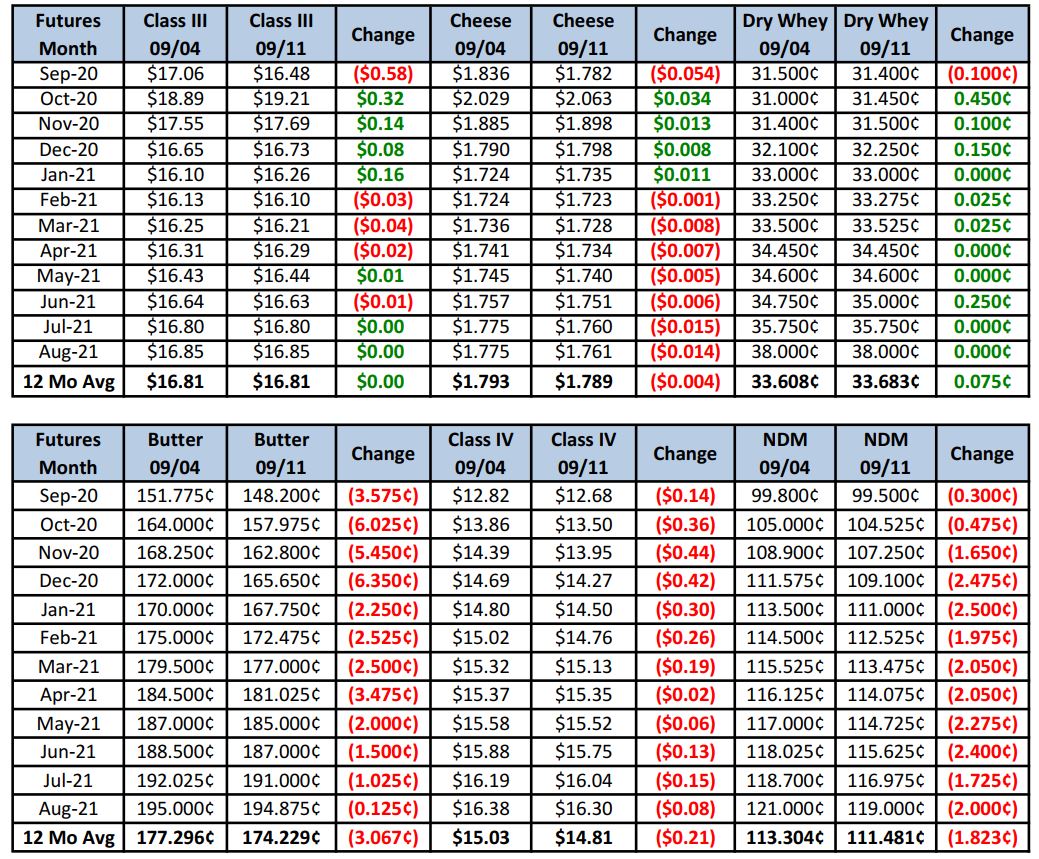

Futures Recap

Dairy Market News reports milk production in the Northeast and Mid-Atlantic regions is flat, but adequate for needs. More milk is heading into Class II and III channels due to lower Class I demand from schools. Milk remains tight in the Southeast, however, as output is being hampered by very humid conditions and a heat index in the low 100s. Bottlers are taking all the milk with nothing left for manufacturing. Output is not expected to increase until after September. In the Central region, milk production is rising slightly as cooler weather has set in. Cheese and balancing plants have ample supplies. California remains hot, though milk output is stable to slightly lower. Currently there is not much left for spot sales, however. Milk output remains strong in the Pacific Northwest, with some discounted loads available. Manufacturers are running at or close to capacity to keep up with the milk supply.

Surplus cream across the country has butter manufacturers churning at a high rate. Stock levels are seeing some growth, but seasonal demand is beginning to kick in, nudging up orders.

With strong cheese output, dry whey production is robust, putting a damper on prices. However, there has been an uptick in demand from Southeast Asia as it rebuilds its pig farms.

NDM prices are shifting higher, with buyers noting it’s getting harder to find anything priced below $1. Stocks are available, but now average just 1-2 months old, whereas a month ago they were 4-5 months old. Domestic sales are good, with steady interest from Mexico.

There were no major reports released this week, but noteworthy was a USDA Section 32 Solicitation for 82.6 million lbs of Mozzarella Cheese. It may be hard to find as contacts we talked to this week described it as tight. Dairy Market News also reports that in the Northeast, current demand for Italian-type cheese is outstripping supply. In the Midwest, cheese output is strong, but contacts report loads are moving out the door, most likely in response to the latest food box program. In the West, contacts suggest cheese demand has been strong for American type block cheese, with no trouble selling supplies. Demand for Italian cheese is good in the region as well, despite a lack of enthusiasm for the upcoming NFL season. Frozen and pizza delivery sales have remained strong.

After a holiday Monday, early on this week looked like a “sell the news” type of situation, with futures selling off, post “government food box” news from last week, even in the face of rising block prices. But that all changed. October Class III futures put in a nearly picture-perfect 50% retracement on Wednesday, hitting a low of $18.28, and has since bounced and put in higher settlements.

The short-term momentum appears to be to the upside at this point. Recall again the chart of the block/barrel spread and how little time it resides there. Then consider that block cheese is in good demand and Mozzarella cheese is tight, so ask yourself what is the more likely scenario for the spread to close, blocks down or barrels up? It may be that blocks will decline and barrels increase, or even that blocks crash to close the spread, but current fundamentals would suggest blocks have more support than barrels. We would expect volume for barrels to pick up next week, with sellers eventually allowing the barrel price to rise. That said, it’s going to need to in a hurry to justify current pricing. October Class III settled at a lofty $19.21 today, but current spot prices work out to about $17.70. October cheese futures settled at $2.06, so clearly the market is pricing in a further spot rally. We still would recommend our trade from the past two weeks, targeting Nov Class III at $18.00 and Dec at $17.50. The government can keep on extending programs, but farmers are responding. The latest culling data for the week ending 08/29 show just 54,100 head went to slaughter, down 12.3% vs. the same period a year ago. Milk is coming.

Have a great weekend! Never forget!