07/02/2020

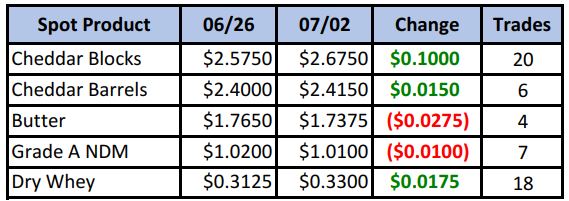

A new government Section 32 bid for 17 million lbs of cheddar cheese seemed to give block buyers enough confidence to begin buying again after last week’s sell-off. At these elevated spot prices, more loads are shaking loose, with block volume at 20 loads this week. Still, buyers seemed to have the upper hand, as with each passing day, a certain number of loads were bought, until offers disappeared the remainder of the spot session. Barrels managed to finish in the green as well, which helped us set a new all-time block/barrel weekly average of $2.54/lb.

Spot Market Recap

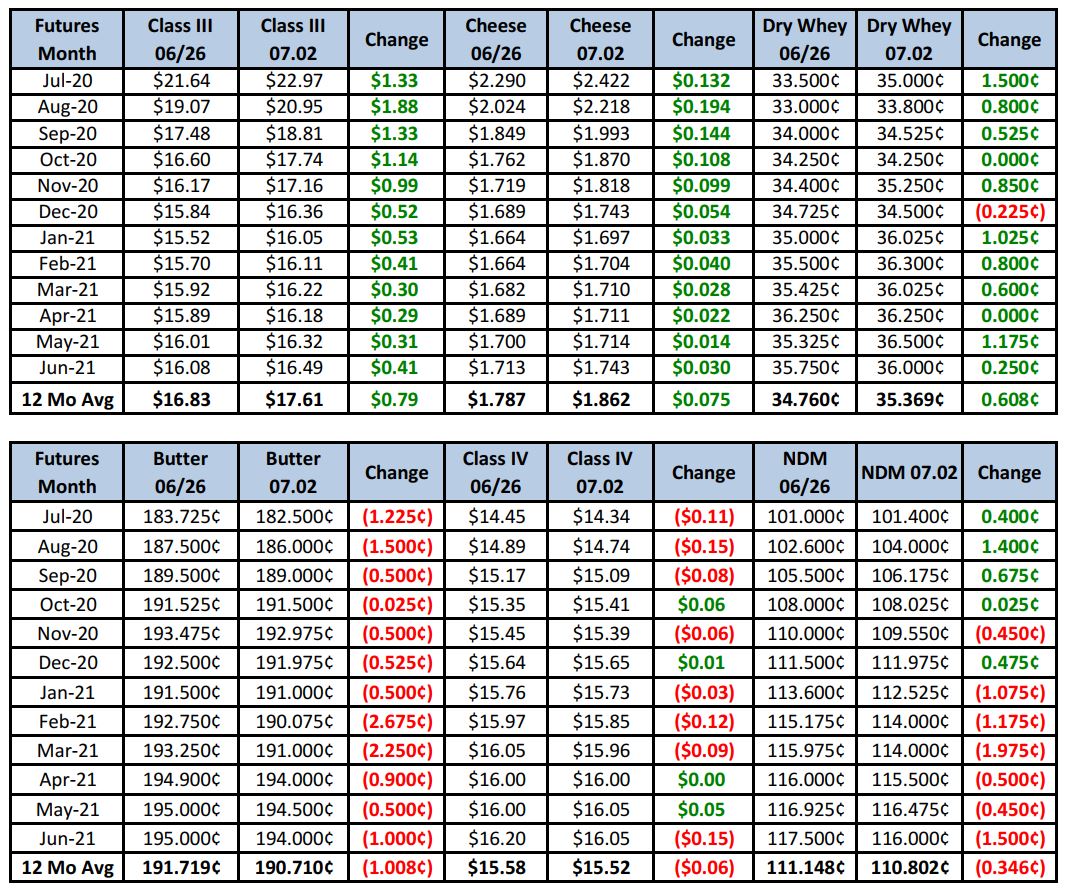

Futures Recap

Nearby Class III contracts saw impressive weekly gains, with the August contract outpacing the others. With sky-high milk prices, producers have slowed down culling in dramatic fashion. This week’s total was down 9% compared to a year ago, and is the seventh consecutive week of below year-ago totals. But that hasn’t resulted in any excess milk yet.

The Dairy Products Report was released on Wednesday. There was nothing there to impact the markets near term, but the following was reported in regards to output in May:

– Cheddar cheese output down 0.5% vs. 2019

– Total cheese output down 0.7% vs. 2019

– NDM output down 9.2% vs. 2019

– Butter output up 4.9% vs. 2019

Finally, we don’t usually mention the milk-to-feed ratio very often, but this week’s Ag Prices Report pegged it at 1.77 for May, the lowest since Aug 2013.

Current spot prices work out to about $24.35 (using July whey futures). With July Class III settling at $22.97 today, and two weeks of it’s calculation in the books, it could still push quite a bit higher in the weeks ahead, should spot hold. And this helps explain why the August contract saw the largest gain on the week. With just two weeks before it starts pricing, and fundamentals telling us strong domestic demand and government buying will likely support prices, it had traded in the upper-$18’s as recently as Monday. Like the contracts before it, it seems to be begrudgingly closing the spread with spot, while kicking and screaming all the way up. Expect more two-sided trade in next week’s spot market, but we’d expect the front months to keep grinding higher in the short term.

Producers should be looking at price protection up front. Option spreads may not be a bad idea. For example, the Aug 19.00 PUT settled at 50¢, while the $23.00 CALL settled at 36¢. For a net of 14¢ premium, a producer could establish a $19.00 floor, but rally with the market all the way to $23.00, where they’d be capped. That’s pretty cheap insurance. Likewise for September, the $17.50 PUT settled at 70¢ and the $20.25 CALL at 55¢, so a net of 15¢ would yield that min/max. Call us next week if you are interested in looking at these, or others.

Have a great weekend, and enjoy your freedoms! Happy Independence Day!

Note: Our offices will be closed on Friday (markets are closed as well), but will reopen on Monday.