07/10/2020

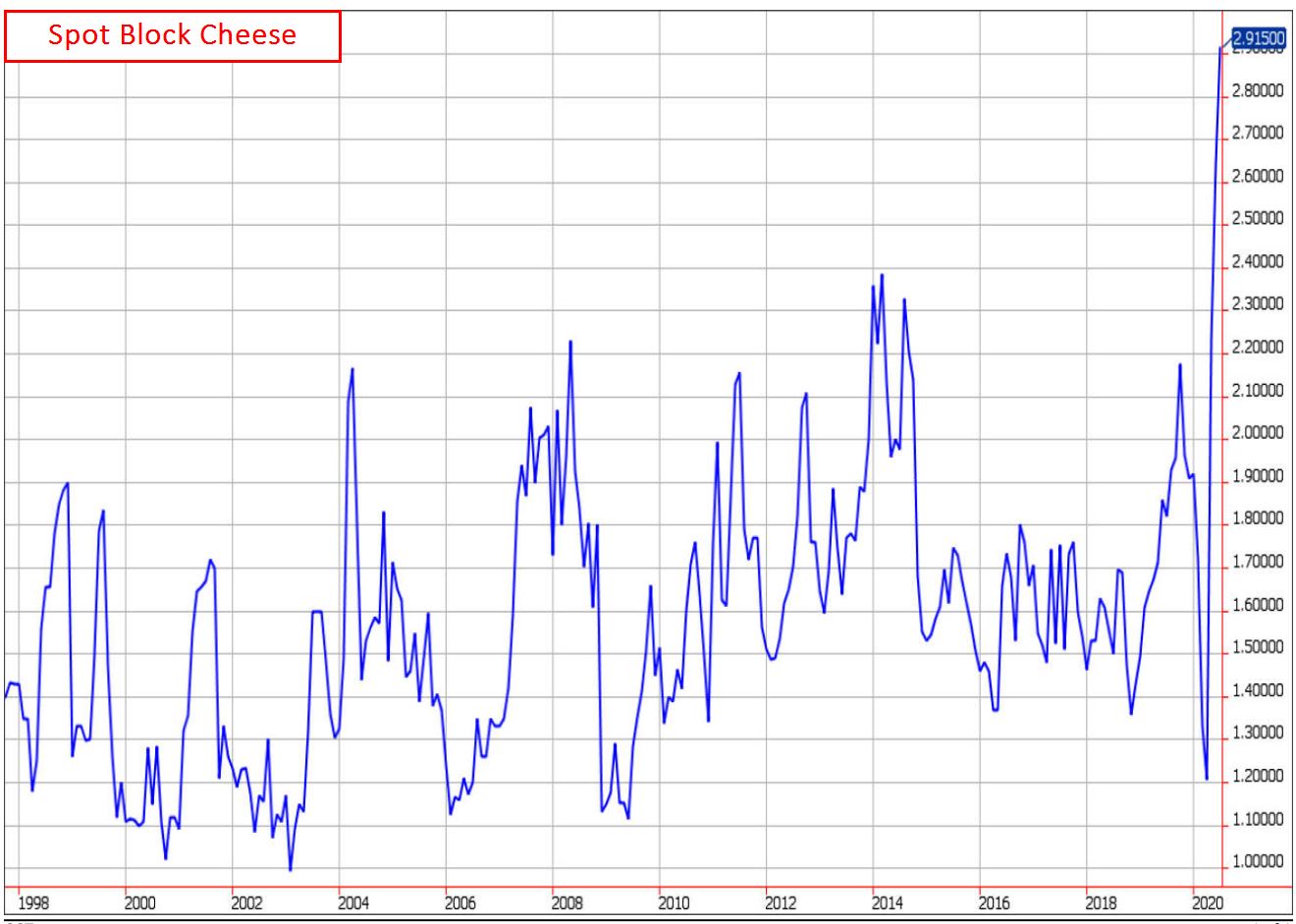

Records were made to be broken, and spot block cheese did that with gusto this week, jumping 24¢ to set a new all-time record high. Sellers were willing to part with product all the way up as blocks traded healthy volume, but after several loads were sold each session, bidders had more bullets left than those offering did. The chart below shows just how epic a move the block price has made.

Spot Market Recap

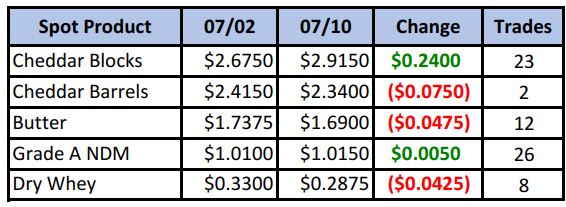

On the flip side, barrel cheese lost momentum and ground this week, along with butter and dry whey. NDM took the volume prize with 26 loads exchanging hands.

Futures Recap

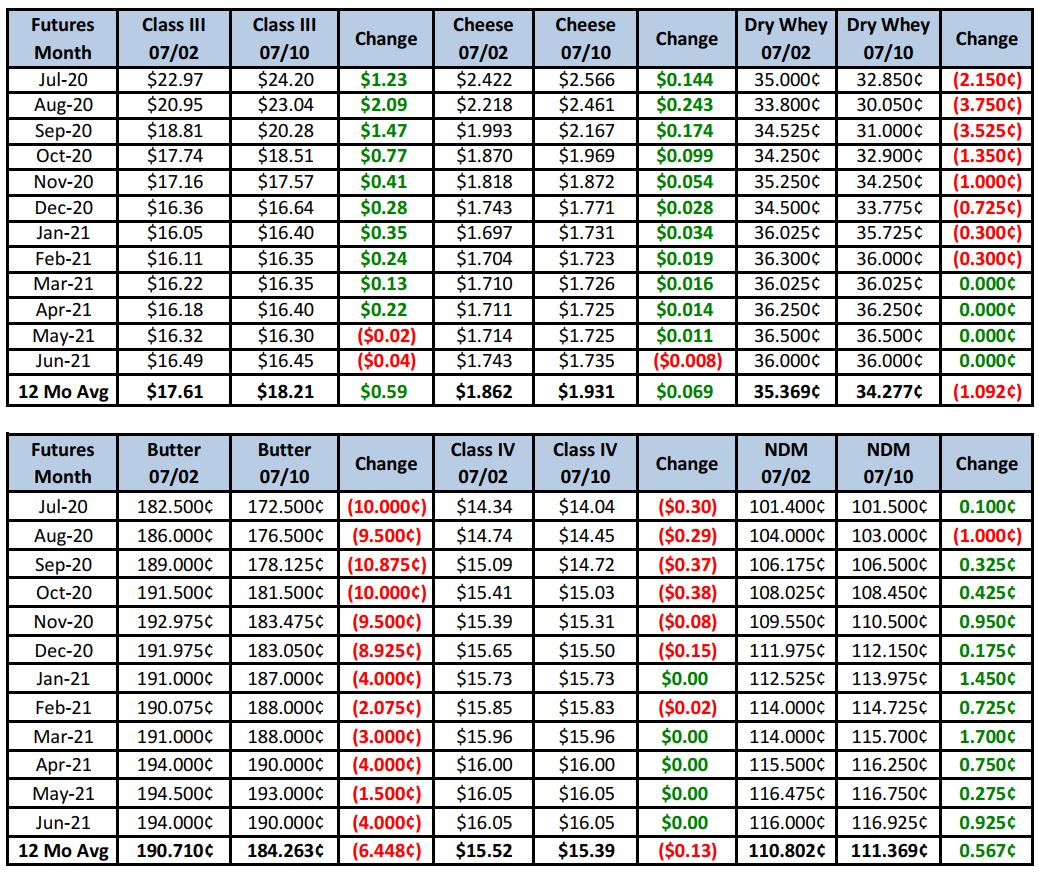

With the relentless move high in the block price, the block/barrel average reached a new record high of $2.63/lb, despite the price decline in barrels. Front month futures finished the week sharply higher, with the August contract seeing the largest gain. August begins pricing after next week and is still trading at a decent discount to spot, which calculates out to about $24.90/cwt.

The U.S. Dairy Export Council reported at the end of last week that U.S. dairy export volume hit a 2-year high in May, and up 18% compared to a year ago. Gains were led by a 24% increase in NDM/SMP exports of 79, 163 MT, the most ever. Southeast Asia jumped above Mexico again as the number one destination. Cheese exports also had a good month, with exports up 8% and shipments to South Korea and Japan at multi-year highs. Exports as a percentage of milk production hit its highest level since 2018, at 17.4%

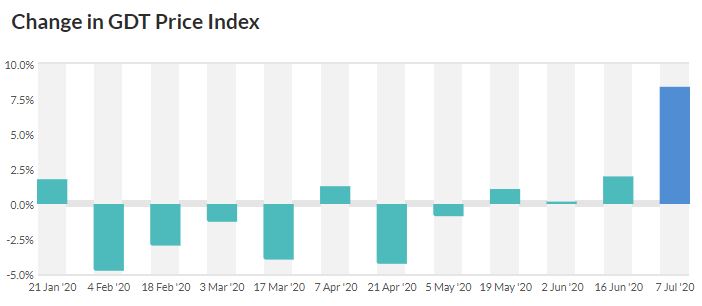

Tueday’s GDT auction saw the Dairy Price Index shoot up 8.3%, its biggest increase in over 3 years. Gains were led by WMP up 14%. Cheddar cheese increased 3.3%.

Butter production across the country is slower as ice cream plants pull the majority of available cream. Sales have declined as more restaurants are being affected by the resurgence of COVID-19.