06/26/2020

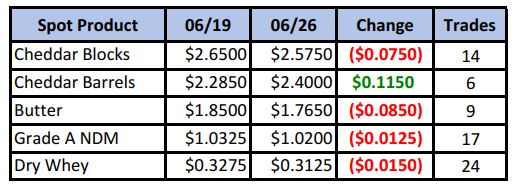

What a wild week! Spot blocks set a new all-time high of $2.81/lb on Tuesday, only to be followed by a 23¢ drop on Wednesday. Meanwhile, barrels kept their cool and began closing the spread with blocks. Volume was fairly light, considering the price action in blocks.

Spot Market Recap

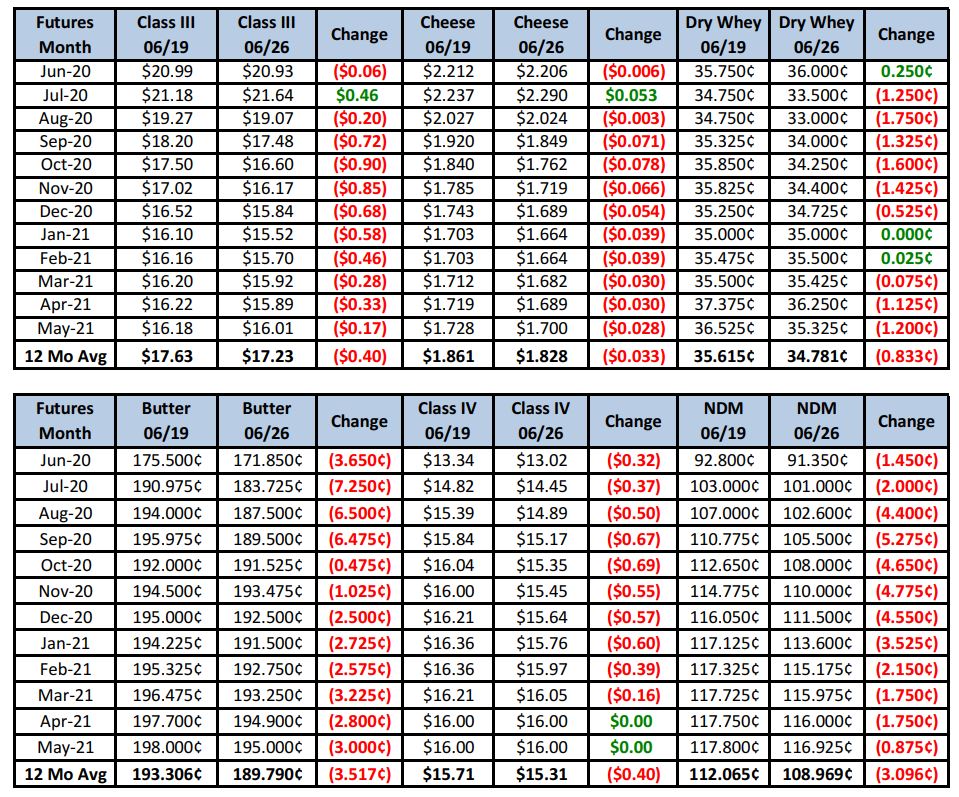

Futures Recap

And wow, did futures ever react! With July Class III pricing a steep discount to spot at the beginning of the week, expanded limits saw both the July and August futures contracts trade intraday more than $1.00 higher. But the joy was short-lived as the spot crash on Wednesday saw up front futures limit down, followed by another steep sell-off Thursday, in what was likely heavy producer selling and long profit-taking. But there’s more! On Thursday afternoon, USDA announced two Section 32 purchase solicitations; one for 11.4 million lbs of process cheese, and another for 11.5 million lbs of butter. Markets started to push well off their lows for the day, even putting in new intra-day highs up front. Finally, on Friday, another USDA Section 32 purchase solicitation for 17.4 million lbs of NDM was released after the close.

The government continues to be a significant factor influencing the market with the “food box” program. Suddenly the spot market looks supported again as buyers look for product. The impact of the program may be reflected in the weekly cold storage numbers that came out on Wednesday. Cheese holdings at USDA-selected storage centers are down a strong 14% (13.2 million lbs) over just the first 22 days of June.

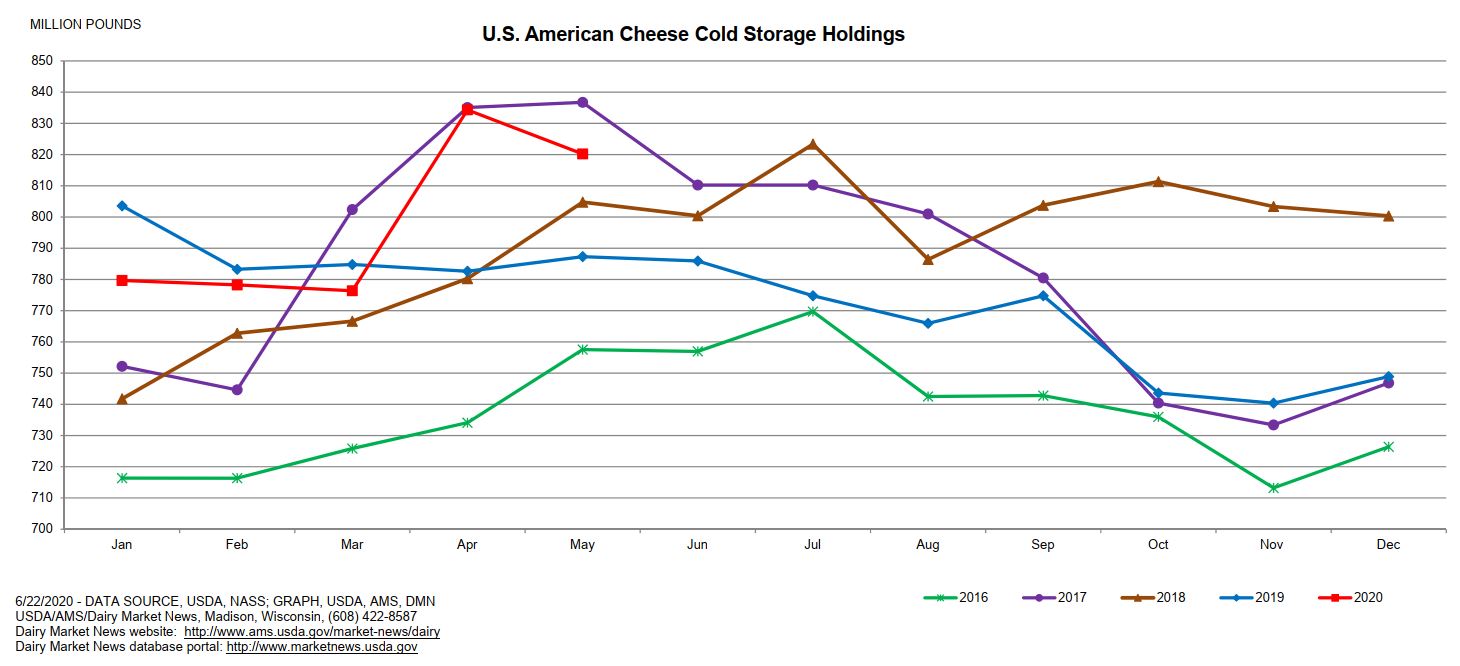

The only major report released this week was the Cold Storage Report. American cheese stocks at the end of May came in below expectations with an anti-seasonal 2% decline from April (see chart below).

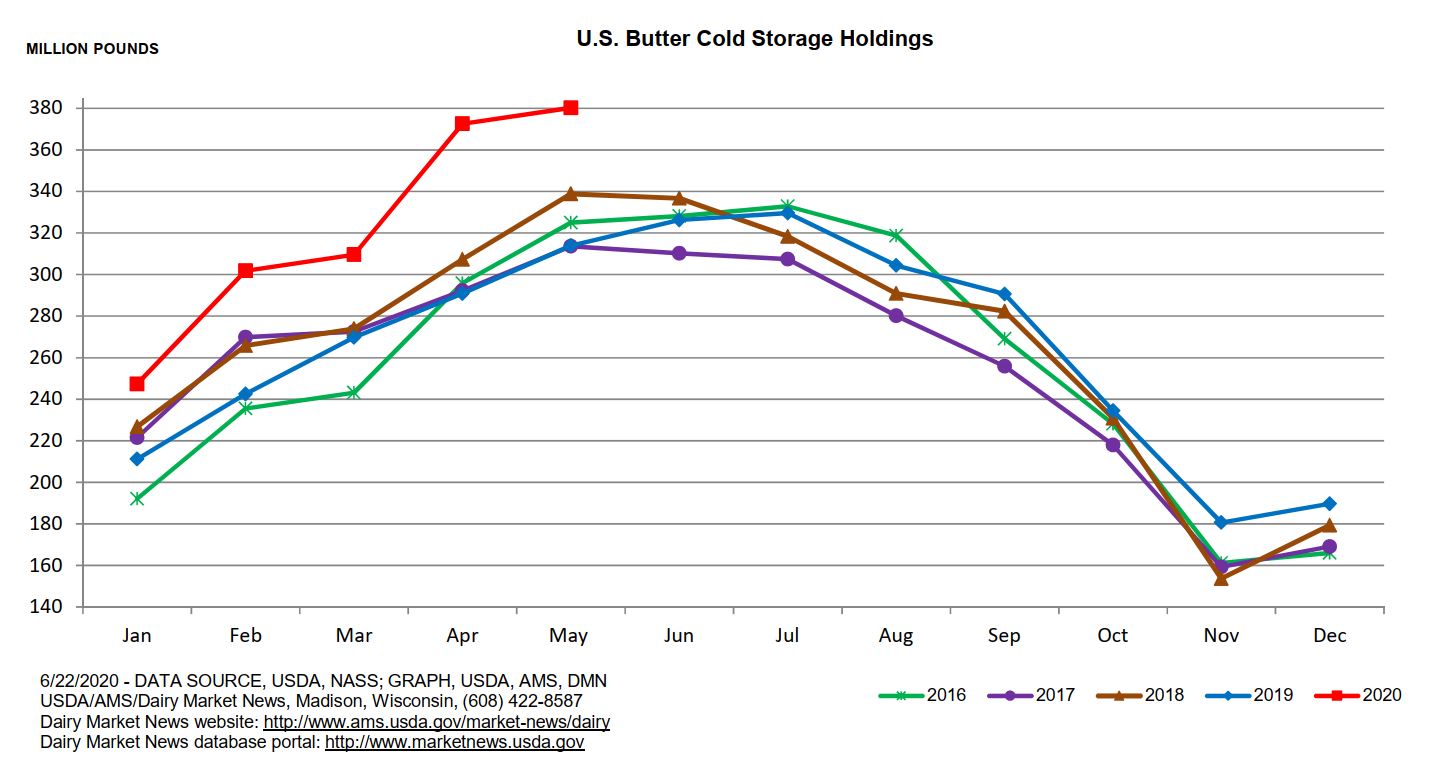

Butter stocks on the other hand were up 21% compared to last year, and up 2% from April.

Dairy Market News reports are still largely bullish cheese. Milk is still tight in the East and cheese demand is healthy. Midwest plants are working overtime and there are even some slightly discounted spot loads of milk, but buyers from the East aren’t letting high cheese prices slow down purchases yet. Barrels are more available, but tighter than they were a year ago. Sales are strong in the West as well as some plants are working above capacity levels. Some buyers remain nervous, but the extension of the Food Box program is helping fuel Western demand.

With spot prices working out to about $23.70 and the July Class III contract well in to its pricing period, it is still trading at a large discount. The brief correction in blocks mid-week seems to have stabilized, and with the government sending out new Section 32 bids and extending food programs, it seems hard to believe a further crash is imminent, but as we all know, the market is always right. Should the spot market continue to see support, July Class III will continue to push higher.

Looking at weekly settlements however, the market obviously believes these prices are not sustainable. August on out, and especially Q4 contracts were hit hard. Increasing cases of COVID-19 and associated concerns with returning to a more restrictive lock-down situation in the U.S. had the stock market selling off today. That could also be affecting the dairy markets as, just when restaurants have started to reopen, they could again be shuttered or left with a “carryout only” option. The loss in demand would hurt prices.

We are living in very uncertain times. Producers should continue to look at DRP strategies and perhaps an option fence strategy for Q4 and Q1 2021. Option premiums are extremely high due to volatility, so taking advantage of that with a spread may be the best way to go. Call us for specific recommendations for your dairy. We’re here to help!

Have a great weekend!