12/13/2019

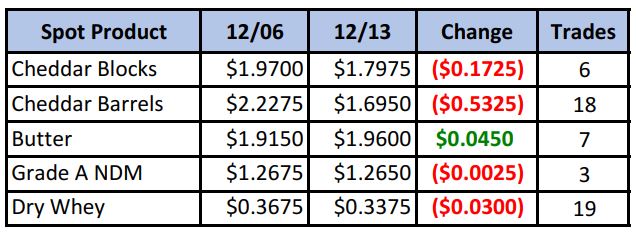

That “thud” you heard this week was the price of barrel cheese as it plunged 53¼¢. Blocks had no choice but to follow as bidders were completely outgunned by offers. The combined move shared $3.33/cwt off the Class III calculation in 5 trading days. NDM and dry whey also lost ground, with butter being the only component to finish the week higher.

Spot Market Recap

There has never been as epic a move in the spread as we’ve witnessed the past few months (at least as far as our charts go back). It as just this past Sep 23rd that blocks peaked at a 47¼¢ premium to barrels. Production issues and a surge in demand rallied the barrels to a 37½¢ premium to blocks on Nov 12th, just 36 trading days later. And that was followed by the spread moving back to a block premium to barrel this week. All said, the spread made an 80¾¢ move in the first leg, followed by a 47¾¢ move (so far) in the second leg, for a 128½¢ total move. That is some amazing volatility (see chart below).

While blocks were not immune, most of that volatility was in the barrel price, which peaked at $2.39/lb on Nov 6th, before careening down 69½¢ lower (so far) in 27 trading days to today’s settlement. Front month Class III futures suffered the most damage, despite the fact that they had been pricing in a substantial fall for weeks. It was just much more than anyone anticipated, and it might not be over yet.

Futures Recap

Dairy Market News updates this week were not too friendly to cheese. Output across the country is strong with plenty of milk available for manufacturing, while sales have yet to recover much since Thanksgiving. Inventories are not burdensome, but both blocks and barrels are available.

Milk output across the country is slowly rising, with some discounted milk available. Class I orders are declining as schools and universities prepare for winter breaks. That’s leaving more milk for manufacturing. Cream is generally abundant from coast to coast.

But, it’s not all doom and gloom. Butter sales are improving as the first sub $2/lb prices seen since 2016 are enticing buyers. The block/barrel average has crumbled from over $2.25/lb to just $1.75/lb today. But that makes our cheese much more competitive on the international market. This $1.75/avg could also be an area of support, based on previous highs set in 2017 (see chart).

However, if we break to the downside, we could be in for quite another leg lower.

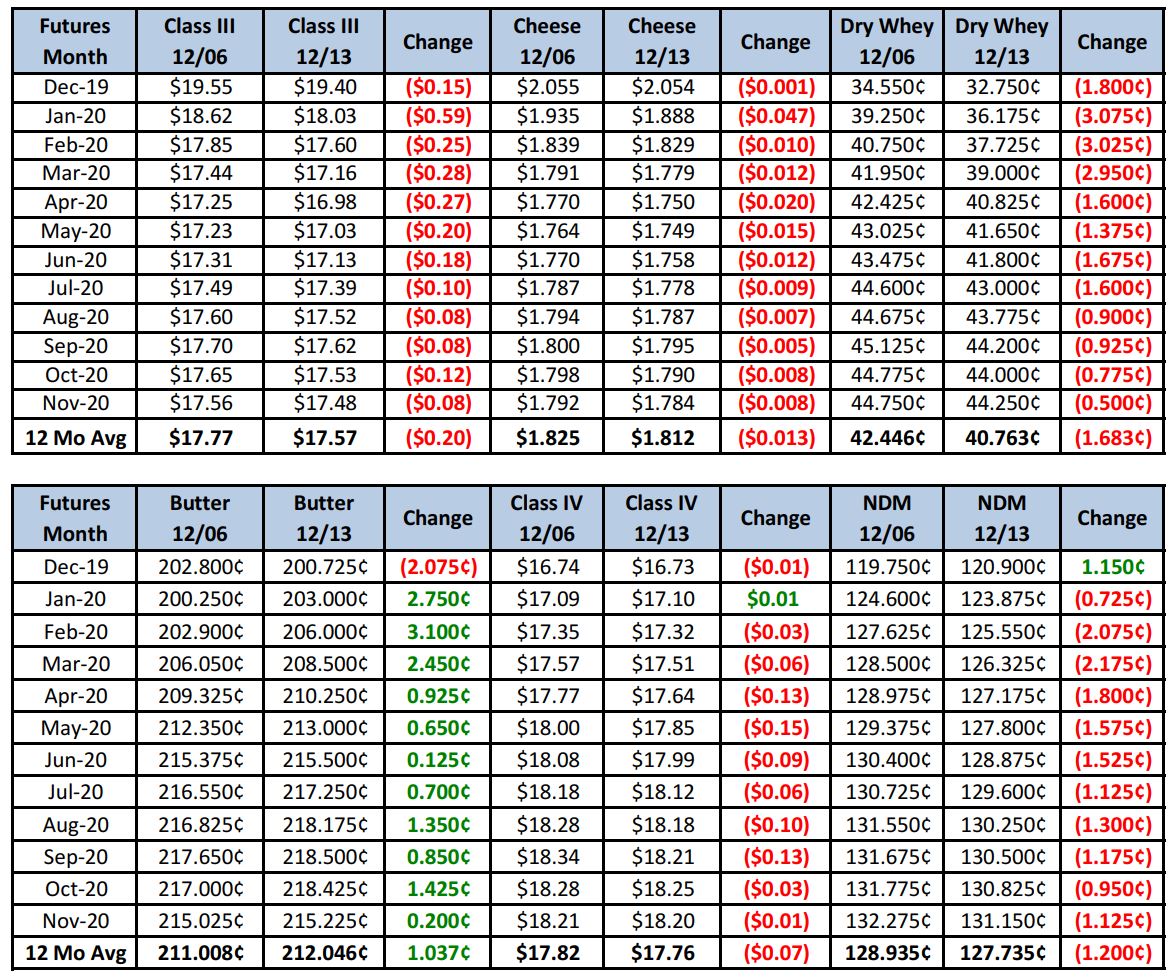

Class III averages settled at $17.60 for Q1, $17.32 for Jan-Jun and $17.40 Jan-Dec. Hopefully previous recommendations were heeded to contract, sell, buy DRP or put options, especially in the first half of 2020. Again, it’s hard to predict where we go from here, other than the momentum still remains to the downside.

With the news that the U.S. and China may be on track for a Phase 1 deal and the new U.S. – Canada – Mexico trade agreement passed, doors may be opening for improved dairy exports next year. Let’s hope the recent move lower is somewhat short-lived. Low prices cure low prices.

Hang in there!