12/20/2019

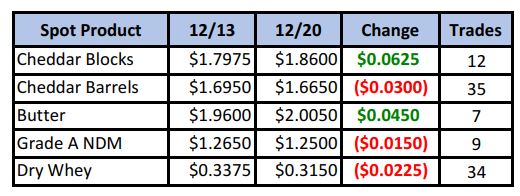

Spot cheese prices regained some footing this week after the prior couple week’s massive sell-off. While barrels ended the week lower, blocks were higher, and trade volume picked up significantly for barrels as value hunters started picking up cheap loads, which briefly traded below $1.60/lb. Reports of strong holiday orders appeared to help lift spot butter prices, which finished back above the $2/lb level.

Spot Market Recap

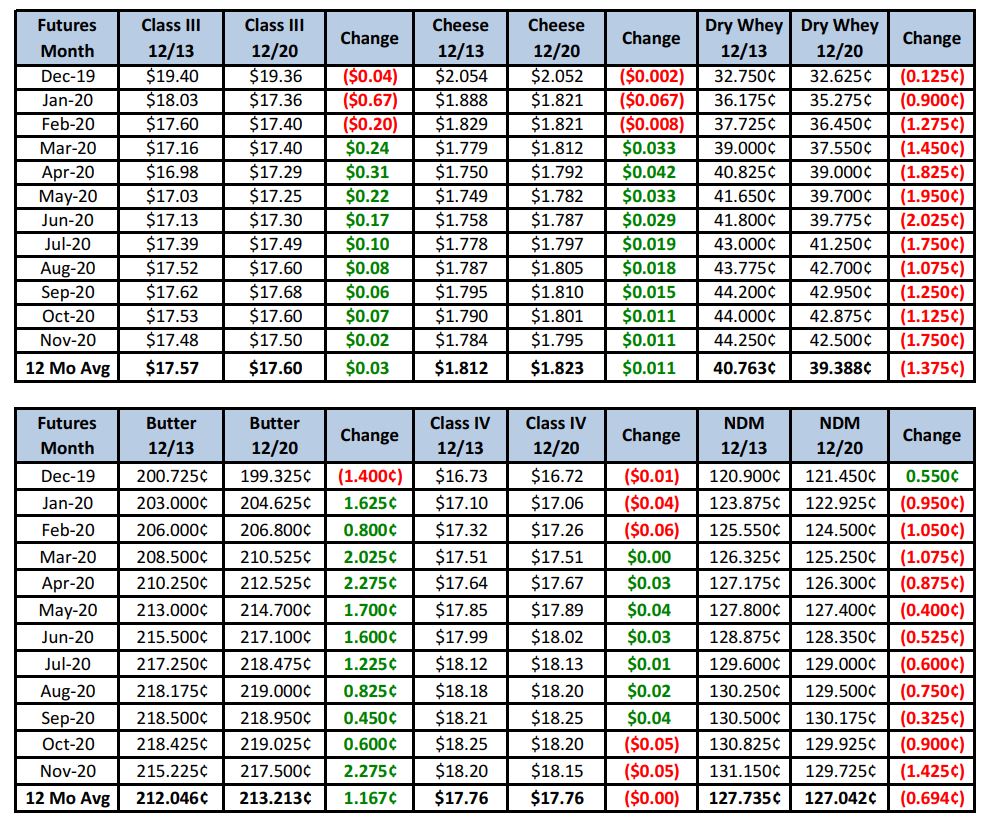

Jan Class III futures still finished the week with a steep loss, due to it being in its early calculation period, and spot prices working out to just $16.90/cwt or so. Add the NDPSR basis and its settlement today is pretty close to even with spot. Further out, futures contracts were all in the green, some significantly.

Futures Recap

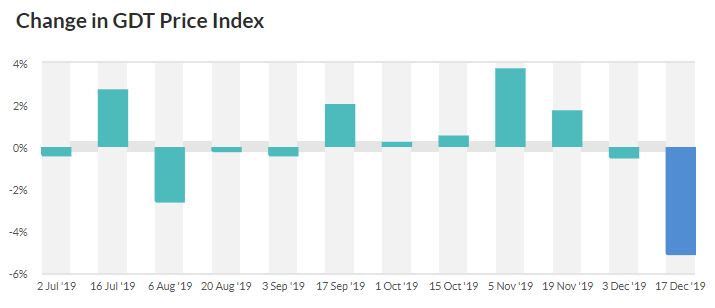

Early on in the week it looked like a strong continuation to the downside was in the works. This was aided by a significant 5.1% drop in the GDT Price Index at Tuesday’s auction.

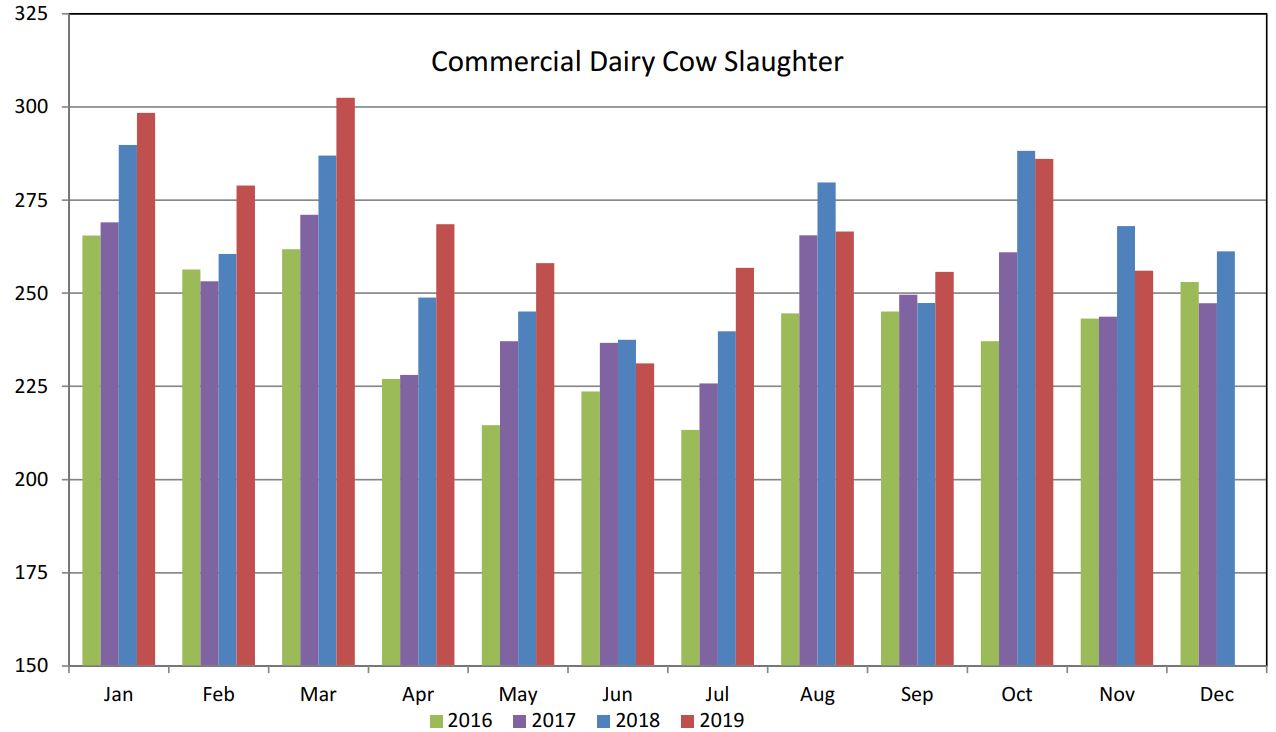

And dairy cow slaughter numbers for the month of November were down 4.4% compared to a year ago, making it 3 out of the last 4 months with totals below 2018 numbers. With recent higher milk prices, clearly the incentive to aggressively cull has diminished.

But global milk production continues to play a supportive role. On the international side, Jan-Oct milk output in the EU increased just 0.5%, with October output up 0.4% Y0Y. Record heat and wildfires continue to torment Australia. November milk production fell 3.4% vs. a year ago, while the current milking season (July-Nov) is down 5.3%.

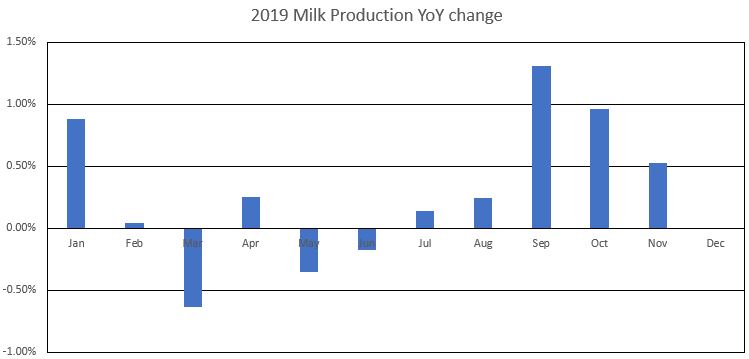

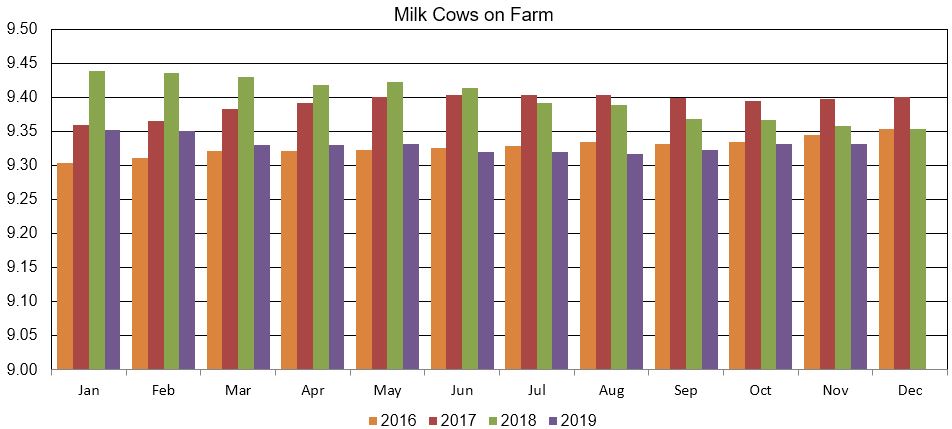

Finally, U.S. milk production numbers were a bit of a surprise to analysts. November milk production in the U.S. increased just 0.5%, the smallest YoY increase since August, and October output was revised lower. Cow numbers, which bottomed out in August and started to increases, were unchanged from October.

Nationally, production gains were again led by the West, with CO up 7% and TX up 6.9%. But tellingly, milk production in WI declined 1.6% and cow numbers fell 7,000 head. Even milk per cow dropped 20 lbs. With most of that state’s output utilized in Class III production, it helps explain some of the recent tightness in the cheese supply. Ongoing feed issues could continue to play a role there, and if cow numbers continue to decline, things could get interesting indeed.

Meanwhile, early December cold storage numbers appear to indicate demand is still good leading up to Christmas and New Year’s. Over the first 16 days of the month, cheese stocks at USDA-selected storage centers declined 2% (1.6 million lbs) while butter stocks fell 2% (864,000 lbs).

Weekly updates from Dairy Market News paint a little more negative picture. Milk output continues to increase seasonally across the country. Schools letting out will mean more milk available for processing. Some cheese plants reported spot loads of milk at $8 under Class. Inventories are not burdensome, but on the same hand, both blocks and barrels are available, so not tight either.

Our take is that we may stay somewhat range-bound in the near term. Demand is good, but supplies are available. After the vicious sell-off, the market bounced. Q2 had a high settlement of $17.41 avg on 12/03, a low settlement of $16.94 avg on 12/17 but came all the way back to close at $17.28 avg today. That’s impressive. If we’re able to climb higher from here and re-challenge the previous high, that would be technically bullish. But a failure from here likely means we’ll re-challenge the prior low and maybe even put in a lower low, which is technically bearish. Watch these months carefully. Hedgers should consider getting some Q2 coverage at current prices or higher if they have little to no protection in place.

We still aren’t too excited about aggressive sales in the 2nd half of the year. Global production issues, domestic feed issues, improving trade relations and a strong economy still suggest limited downside risk. At an avg $17.52, the second half is just 6 cents away from its life-of-contract high, so it didn’t experience near the sell-off the first half did.

As we close 2019, we at KDM Trading want to wish you and your families a very Merry Christmas. We are blessed and thankful to work with each of you.

Finally, there will not be a report next week.