11/15/2019

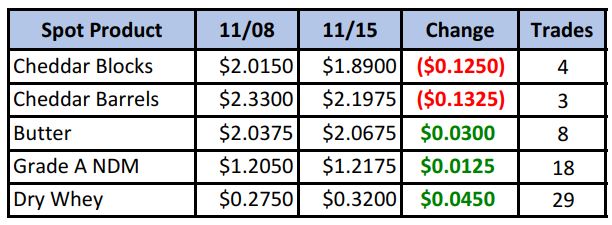

Spot cheese prices continued to retrace from recent highs this week, with blocks reaching a level not seen since late August. NDM on the other hand pushed in to new multi-year highs, butter perked up and dry whey had a strong week, putting in a two-month high. The strength in those components helped close the gap between Class III and Class IV to just over $2/cwt.

Spot Market Recap

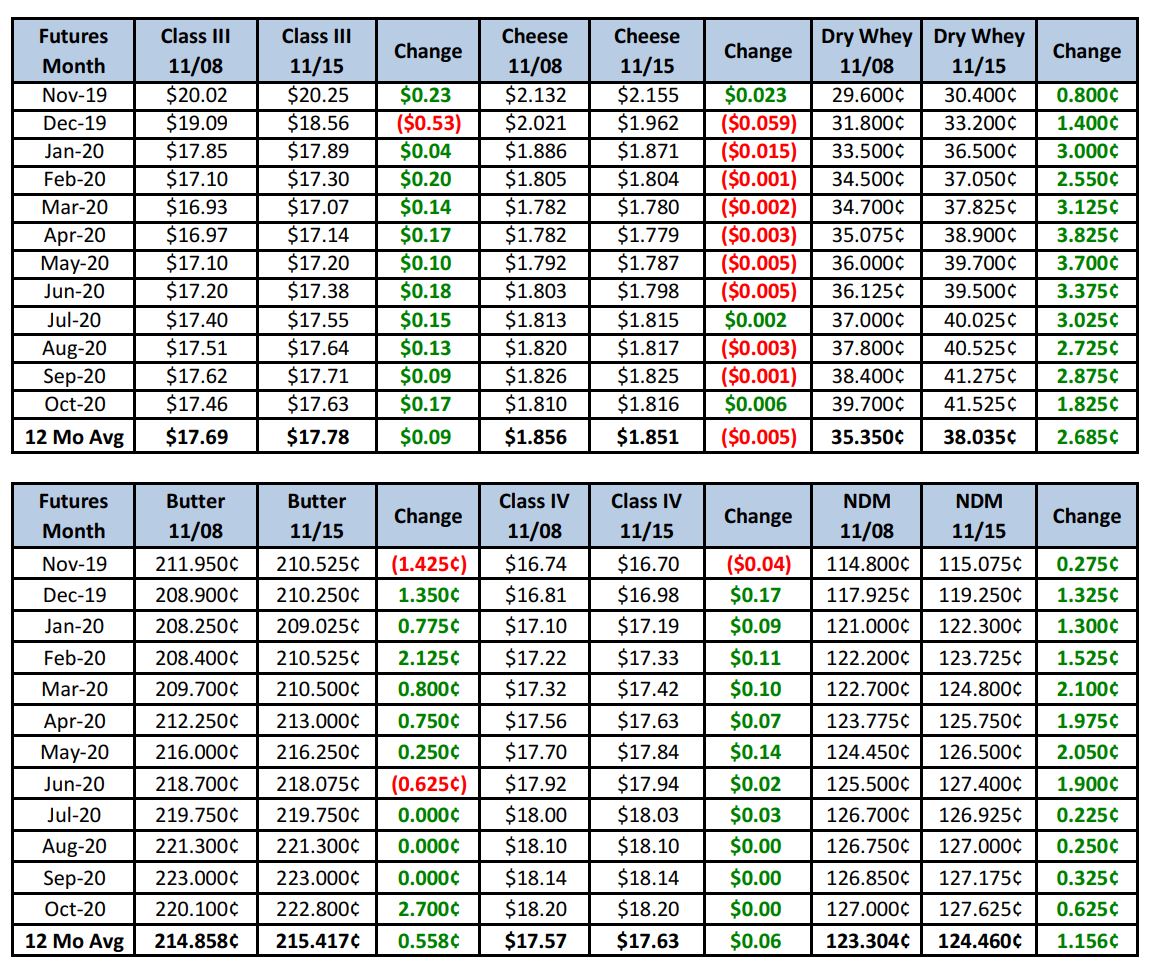

Futures Recap

Dairy Market News reports this week indicate milk production in the U.S. is beginning to pick up. Balancing plants in the NE had been idle during the summer but are now receiving steady to strong milk volumes. Eggnog production has begun, while Class I sales are steady to improved. Output is steady in the Central region, but bottling demand is lower. Some cheesemakers are beginning to report more discounted spot milk loads, as more milk becomes available for manufacturing. The West continues to track higher in milk output as in previous weeks. Plants are running near full capacity in CA. In the Pacific Northwest, some contacts feel there is too much milk. Discounted milk loads of $4.75 below Class IV are common. Cream is available on each coast but tightening in the Central region. Churns are generally full, however, keeping up with increasing holiday demand. NDM continues to move well with Mexican buyers putting positive pressure on the markets. Inventory is available, but demand is strong enough to keep the tone bullish. Some plants in the East are sold out through 2019. Cheese output is steady to active across the U.S., but sales have slowed compared to last week. Some plants are back to running 6-7 day schedules due to higher milk availability. Weekly cold storage numbers appear to confirm the increasing seasonal demand. Over the first 11 days of Nov, cheese stocks declined 4% (3.6 million lbs) and butter stocks fell 6% (3.4 million lbs) at USDA-selected storage centers.

Class III futures have had an interesting reaction to the plunge in cheese prices. While the Dec contract is down more than $1/cwt from two weeks ago, the 2020 contracts have, as an average, pushed into new life-of-contract highs at $17.45 today.

2020 Class III Futures Average

Long-term feed issues in the U.S. and ongoing international demand recovery may be pushing long hedgers and end users of dairy to get some coverage for upside price risk. The scare of how quickly $20 milk can re-appear is probably motivation enough to buy some insurance. Dairy producers should be looking at these prices and have a plan in place to start getting their downside risk covered. A combination of DRP, options, forward contracts and futures can all be used. The trend looks higher in the 2020 contracts for now. Give us a call if you would like help in putting together a risk management plan for your operation.

Have a great weekend!