11/22/2019

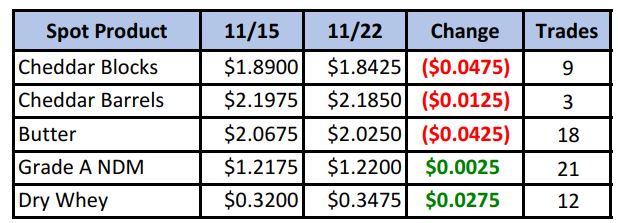

Trade volume in this week’s spot market was much quieter than in weeks past, perhaps as Thanksgiving approaches. Nonetheless, cheese prices continued to give up some ground, while NDM and dry whey traded higher.

Spot Market Recap

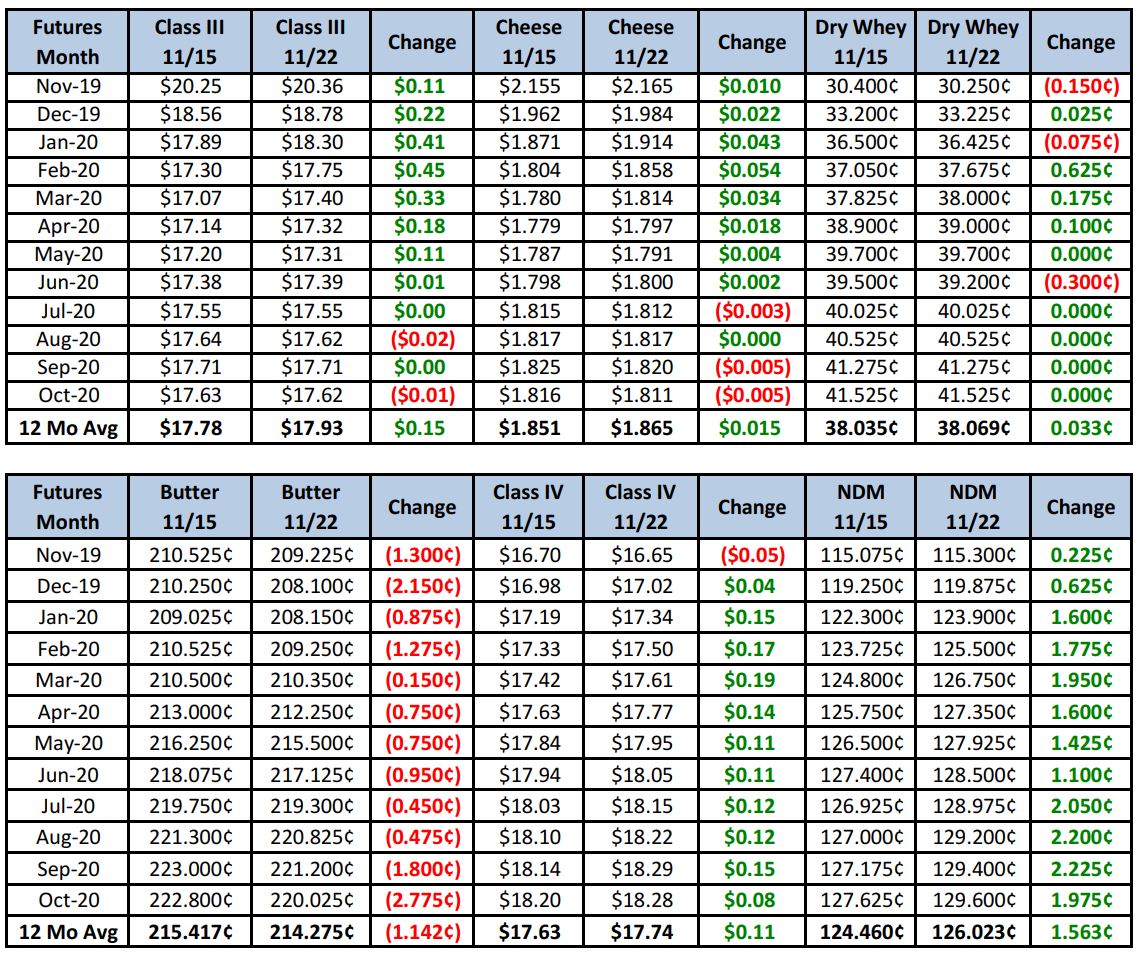

Futures Recap

While the spot market was quiet, Class III futures were on the move, with Q1 contracts seeing the largest gains, pushing in to new life-of-contract highs. The Q1 average settled today at $17.83, the first half of the year at $17.59 and the 2020 annual average gained 8 cents from last week to post a $17.53 average. The question is why? This week’s Milk Production Report was not price supportive. Milk production in October increased 1.3% over a year ago, matching Sep (which was revised higher) for the largest YoY increase in 2019.

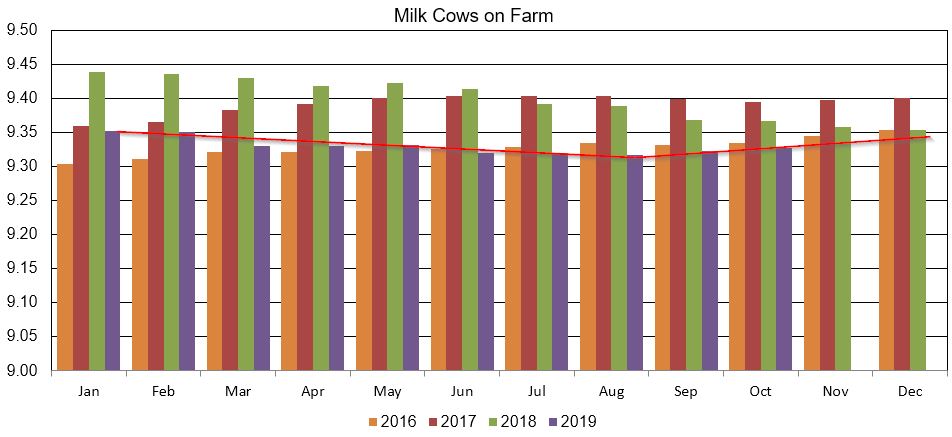

Likewise, cow numbers were up 5,000 head from Sep, and that was after Sep cow numbers were revised higher. The increase from Aug to Oct was 10,000 head. The trend in the herd size has changed. It appears we bottomed out in Aug at 9.317 million head and are now slowly rising (see chart below with red trend line).

Skim milk powder was up 3.3%, while cheddar cheese gained 2.5% to a U.S. equivalent $1.68/lb. Certainly it’s good to see these price increases, but the U.S. is still much higher priced and at an export disadvantage.

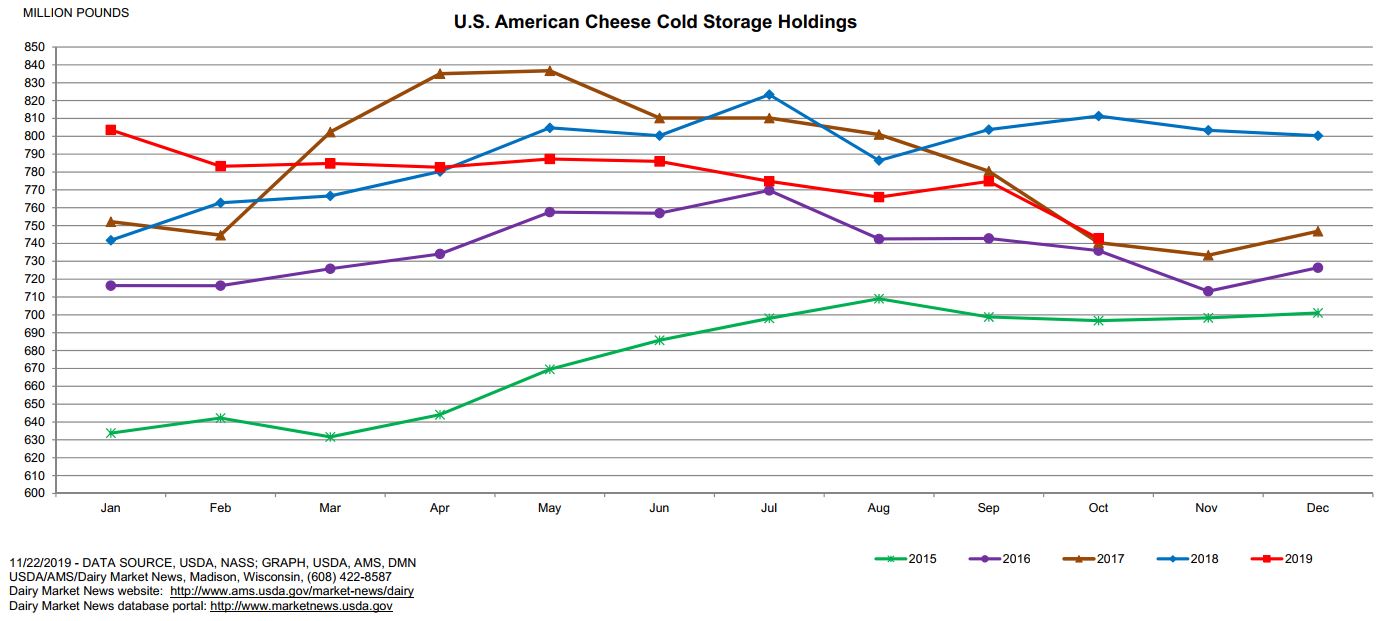

With domestic milk output recovering in the U.S., the herd size back on the rise and reports that cheese supplies are becoming more available (especially in the West), we circle back to our question above, why the strength this week in the 2020 contracts? Today’s Cold Storage Report may provide some insight. A combination of very strong demand and weaker output saw American cheese stocks at the end of October down 8% vs. a year ago. Total cheese stocks, however, were down just 2% YoY.

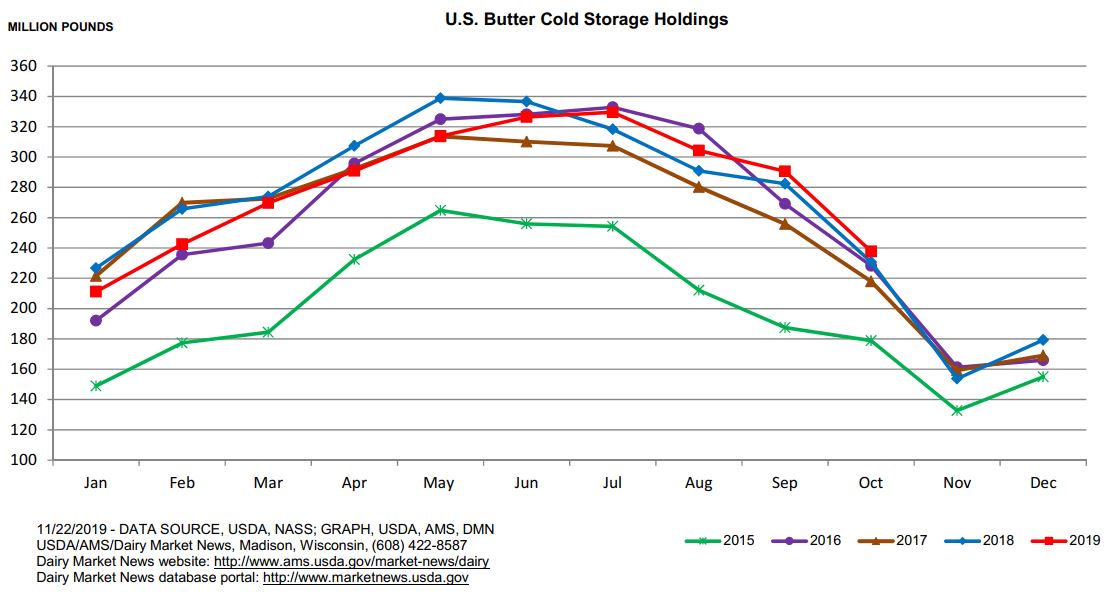

Butter stocks were 3% higher than last October, but made a sharp 18% decline from September.

Finally, our most current weekly cold storage data show that over the first 18 days of Nov, butter stocks at USDA-selected storage centers fell 9% (5.2 million lbs) while cheese stocks declined 3% (2.5 million lbs).

So, we need to remember that the Cold Storage Report is data as of Oct 31st. It helps explain the surge in spot cheddar prices this fall, and current demand appears to be good. But there are cracks appearing in this bull market. Clearly higher profit margins are encouraging the herd to grow and culling to decline. Our cheese prices are still much higher than the rest of the world. U.S. milk output is increasing and both blocks and barrels are becoming more available in the West. How long can we continue to grow our herd before we are once again in an oversupply situation? Powders are still a bright spot and may carry Class III with it for a while, but ultimately higher milk production will fix that supply issue as well.

In summery, we think today’s price averages for 2020 as quoted above, combined with increasing risk factors, mean this is a great opportunity to get coverage for your operation. The Cold Storage Report was released after the market close on Friday, and may be interpreted as price-supportive for the months up front. If you’ve been sitting on the fence, we suggest you get started. Use DRP (call us), put options, futures and/or plant contracts to cover some downside risk. We’re not suggesting lock all of your output in, but up to 30% or so may not be a bad idea. Once you make a hedge decision, you can leave it alone, but we can often work with you to enhance, or open up that hedge to higher prices, should market conditions change. Bottom line, you have a window now; take advantage of it.

Note: There will be no report next week due to the Thanksgiving Holiday. Dairy markets will be closed both Thursday and Friday.

Have a great weekend!