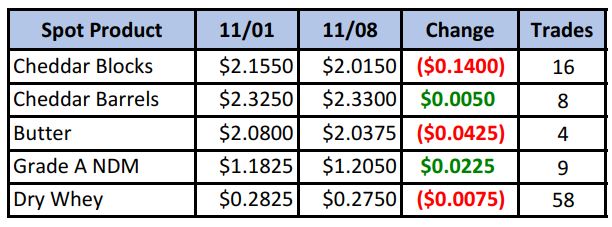

11/08/2019

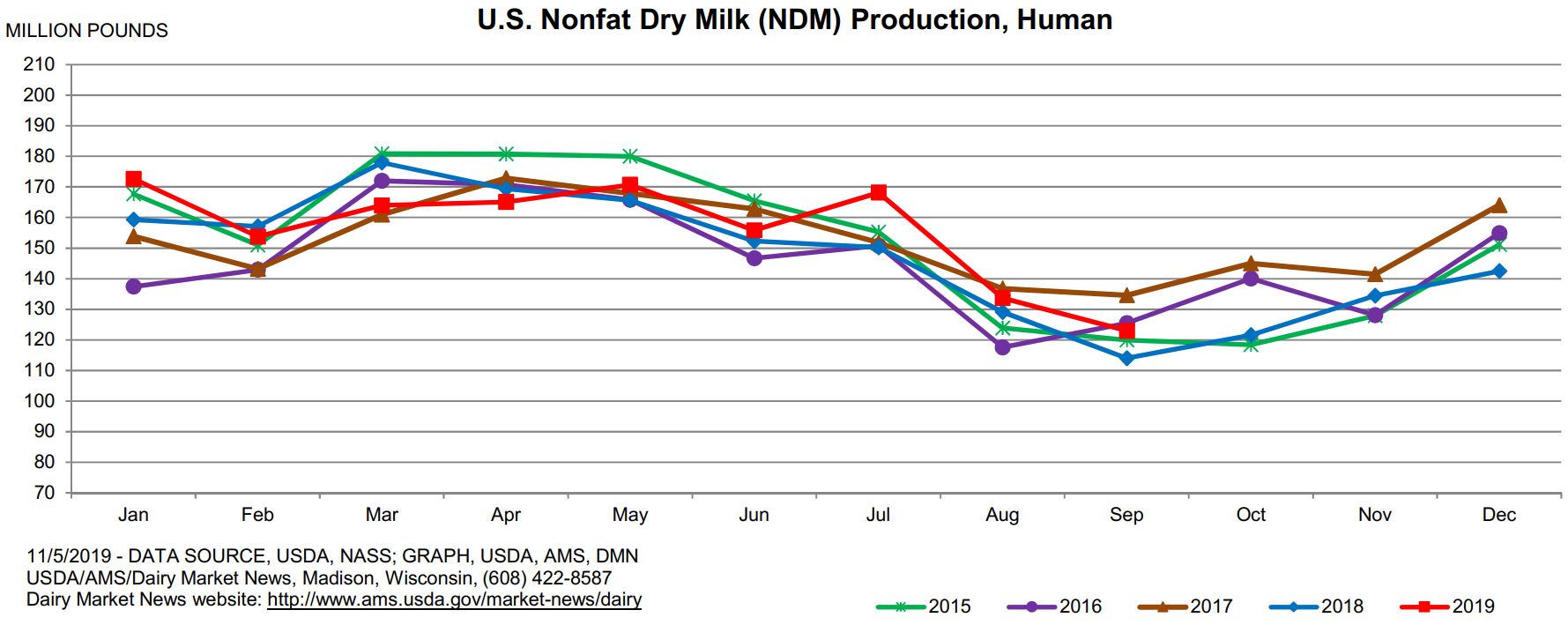

Cheese sellers finally made their presence known, particularly in the block market, which in turn put pressure on barrels. After peaking at $2.39/lb on Wed, barrels gave up ground the rest of the week. The lone bright spot was NDM, which put in new multi-year highs after a positive move in this week’s GDT auction.

Spot Market Recap

Futures Recap

Barrels may still be tight across the country, but just the fact there were offers caused Dec Class III futures to trade limit down for a time on Thursday, before bouncing off its lows. And today saw another day that started in the red but settled slightly higher across the board. The bull market isn’t over, but is taking a break. The extreme inverse premium of barrels to blocks had buyers picking up blocks on the spot market and re-purposing/shredding them for the process market. But milk output is starting to pickup in the NE and Midwest allowing cheese output to increase, while the sky-high prices put a dent in demand.

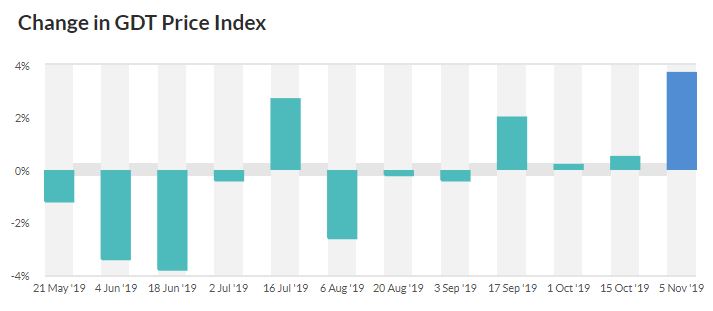

Earlier in the week Tuesday’s GDT auction put a bid in the market as the dairy price index jumped 3.7%, led by a 6.7% gain in SMP.

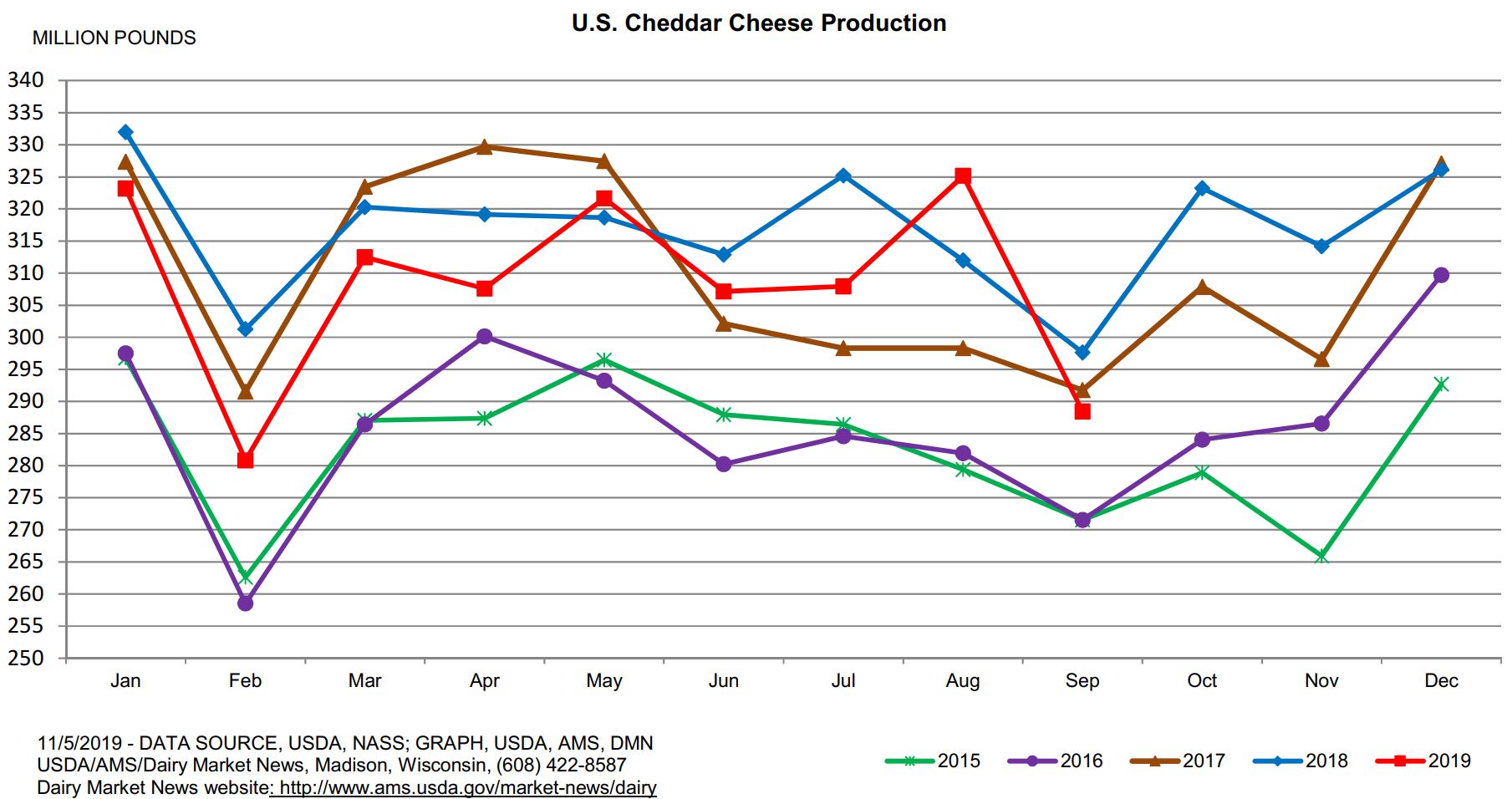

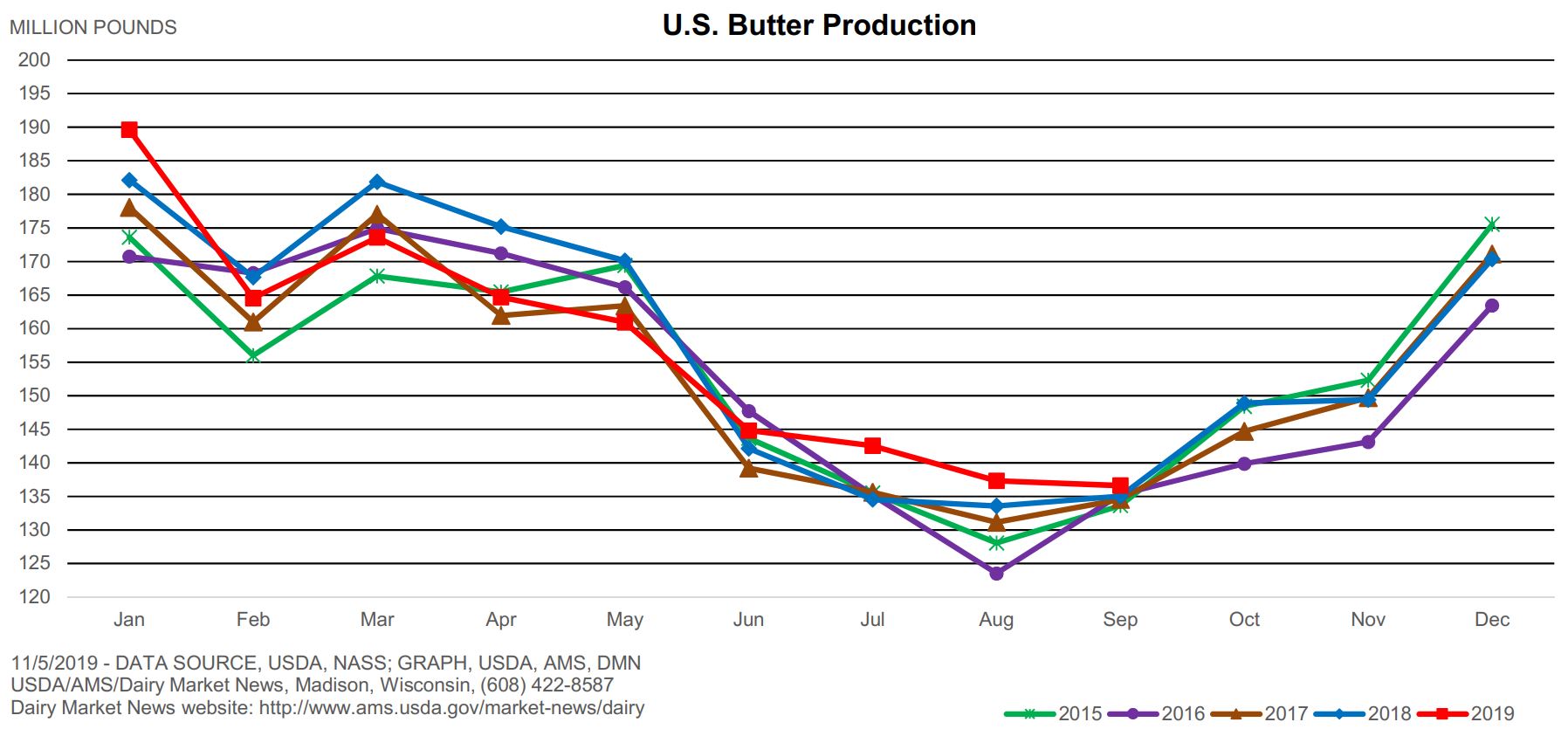

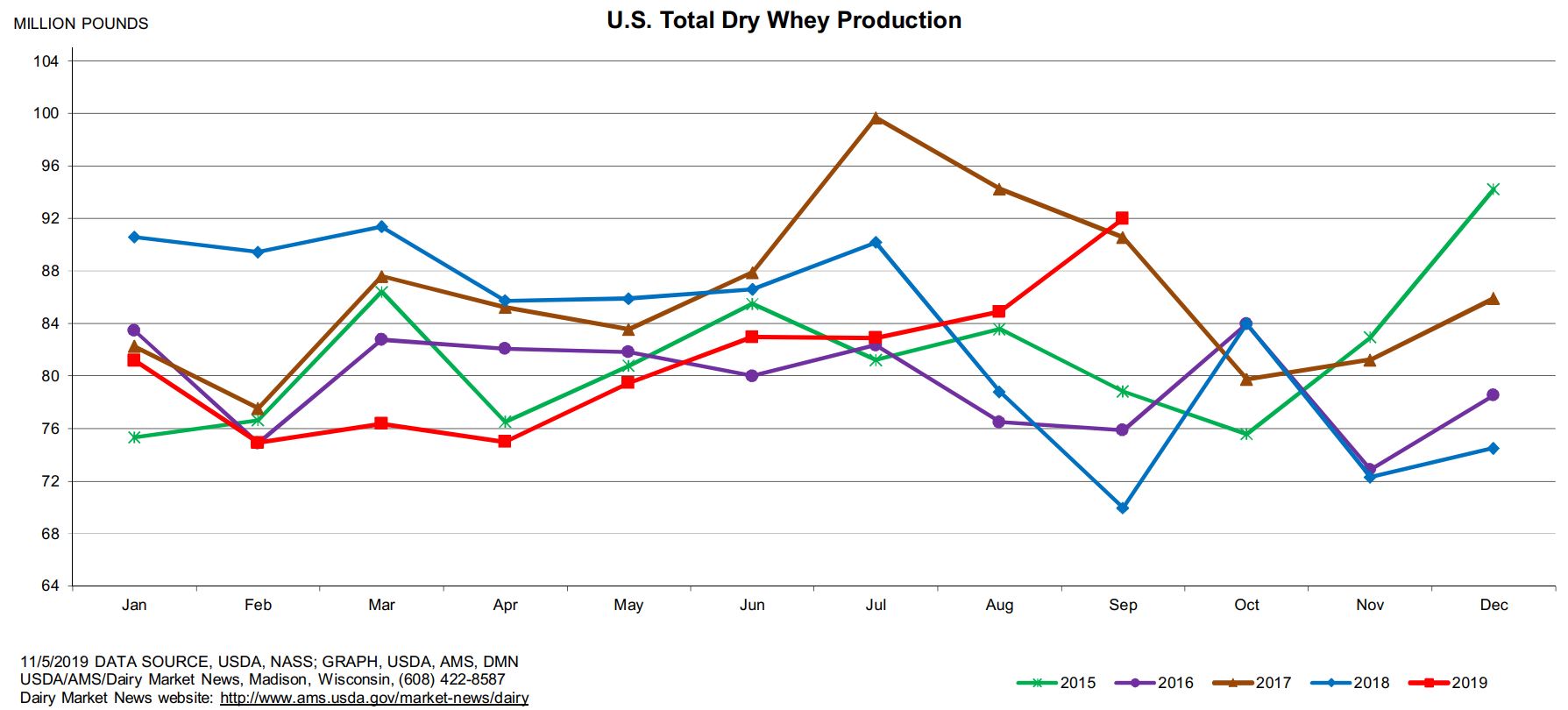

Later in the day, the Dairy Products Report put some numbers behind the jump in spot cheddar prices. Sep cheddar cheese output declined 3.1% vs. a year ago and plunged 11.3% from Aug. Both CA and ID had production issues during the month to cause the steep decline. However, total cheese output climbed 2.1% YoY, butter production increased 1.2% and dry whey output jumped 31.5%. Finally, NDM saw a 2.9% decrease in output compared to last Sep.

While prices in the U.S. have raced ahead of the rest of the world in cheese and NDM, there are signs that the dairy markets are finally firming internationally. The GDT auction is one sign, but Dairy Market News reports this week report that cheese output in the EU, particularly Germany, is not keeping up with demand. This is putting upward pressure on cheese prices, even as manufacturers strain to fill existing orders. EU SMP stocks are very tight, with most output committed into 2020. And in Oceania, milk output continues to struggle in Australia, while New Zealand reported Sep production was down 0.7% vs. Sep ’18. With declining milk production in Australia, a strong showing in New Zealand will be needed to keep the region close to production volumes last year. Finally, some good news in regards to exports. Continued progress is being made in talks with China, and the USDEC reported a rebound in dairy exports in September. Increased trade with Mexico and the UAE pushed Sep dairy exports up 2% YoY, the first YoY increase since Oct 2018. Total dairy exports during the month accounted for the equivalent of 15.3% of U.S. milk production in September, above the average for the first nine months of 14.2%.

While we don’t think a collapse in milk or cheese prices is imminent, further correction is possible. The market ran up a whole lot in a hurry, and for the past few weeks we had been recommending getting some coverage on as Thanksgiving approached. With more milk available in the Midwest, cheese output will slowly increase. Orders may pick up again as we head in to Christmas/New Year’s/Superbowl, so the market will most likely rise and fall with demand/supply. Mother nature may yet play a role too. Next week? Who knows? The 2020 average is still well over $17/cwt. With component pay, it should be a profitable mailbox price. If you don’t have anything done yet, you might want to think about getting 10-25% of your production covered. It’s hard to say what will happen up front as it’s entirely dependent on what happens in the spot market, and at this point, it’s anyone’s guess.

Have a great weekend!