09/27/2019

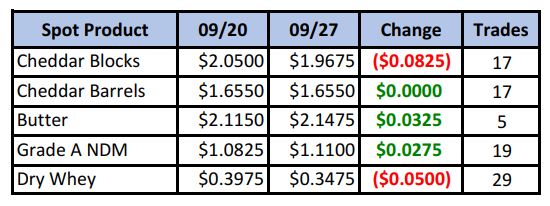

Barrel cheese managed to finish the week unchanged, but blocks gave up another 8¼¢. Buyers were really no where to be seen until Friday, when both blocks and barrels managed to claw back some ground.

Spot Market Recap

While cheese continued to feel mostly weak, spot NDM was the star of the show, putting in a high not seen since Feb, 2015.

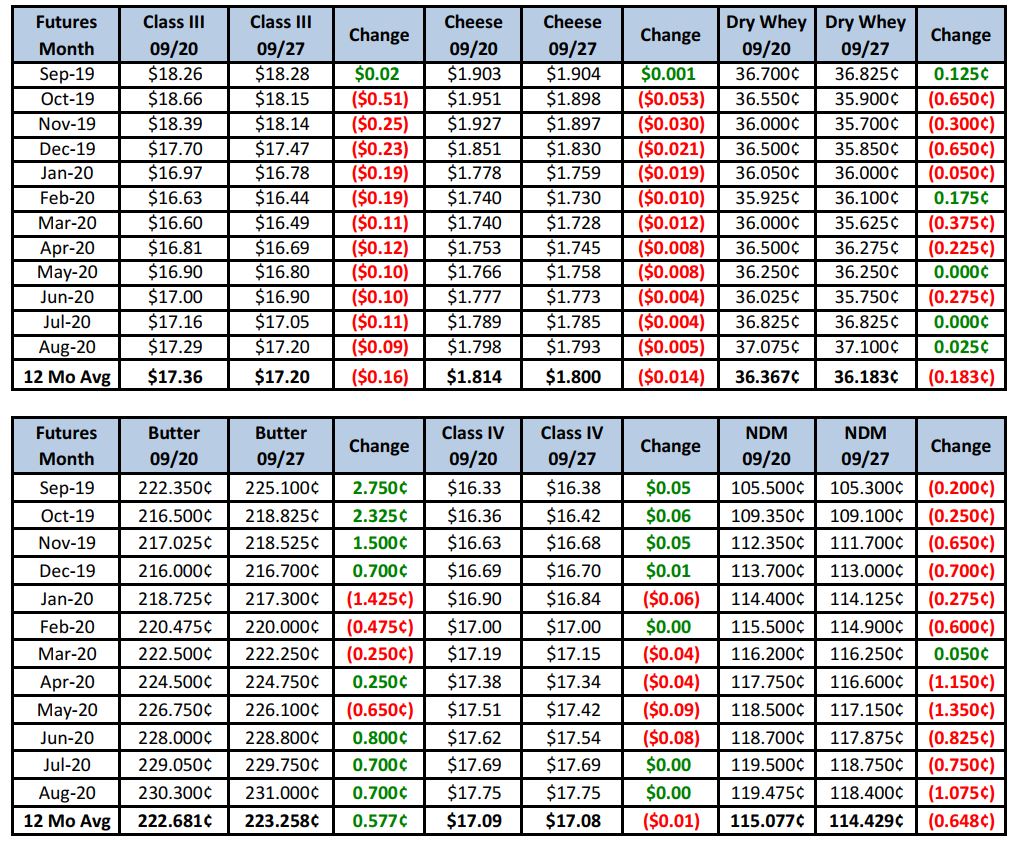

That didn’t seem to help NDM futures, however, which finished the week mostly lower, along with just about everything else except butter.

Futures Recap

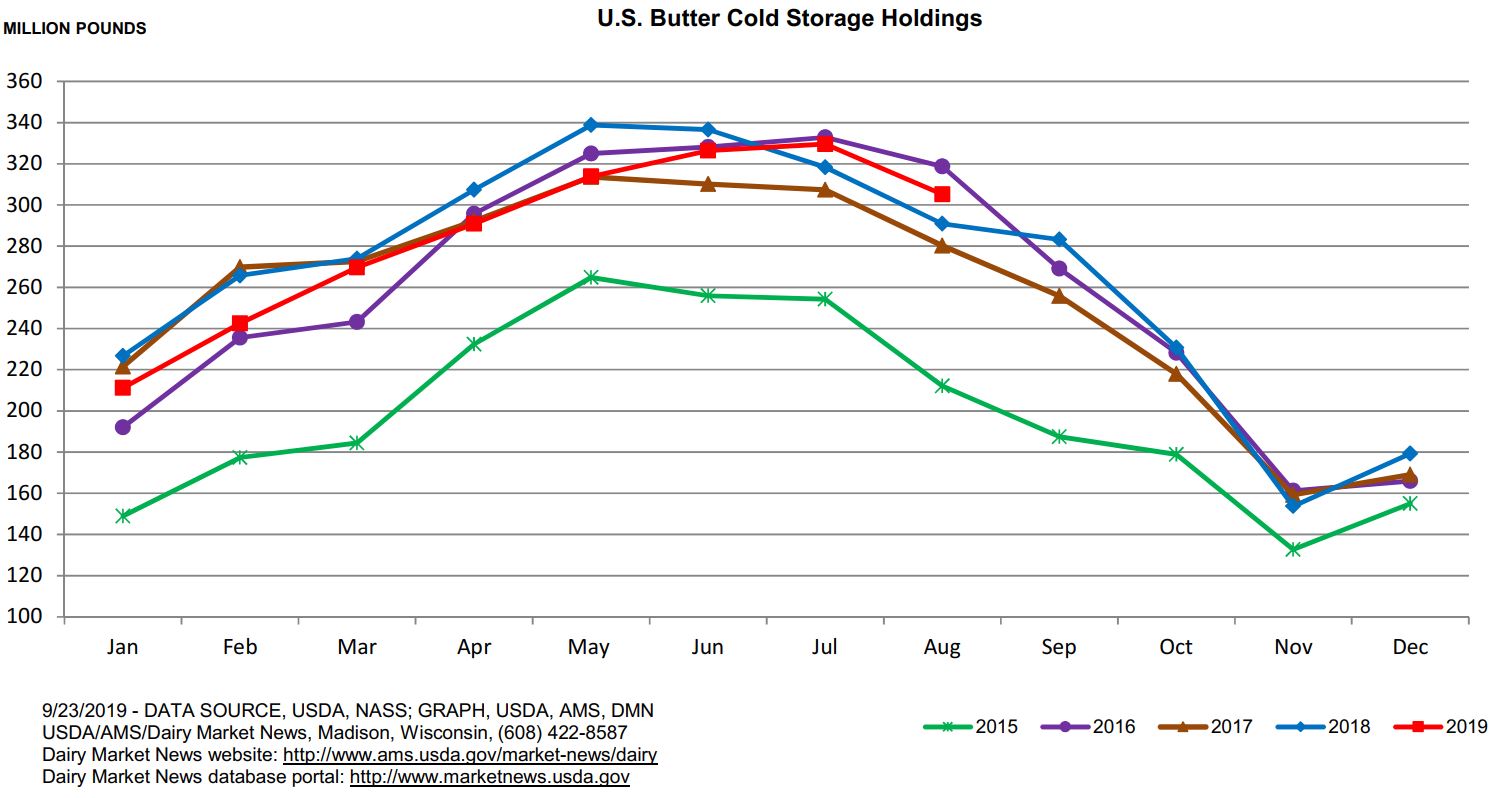

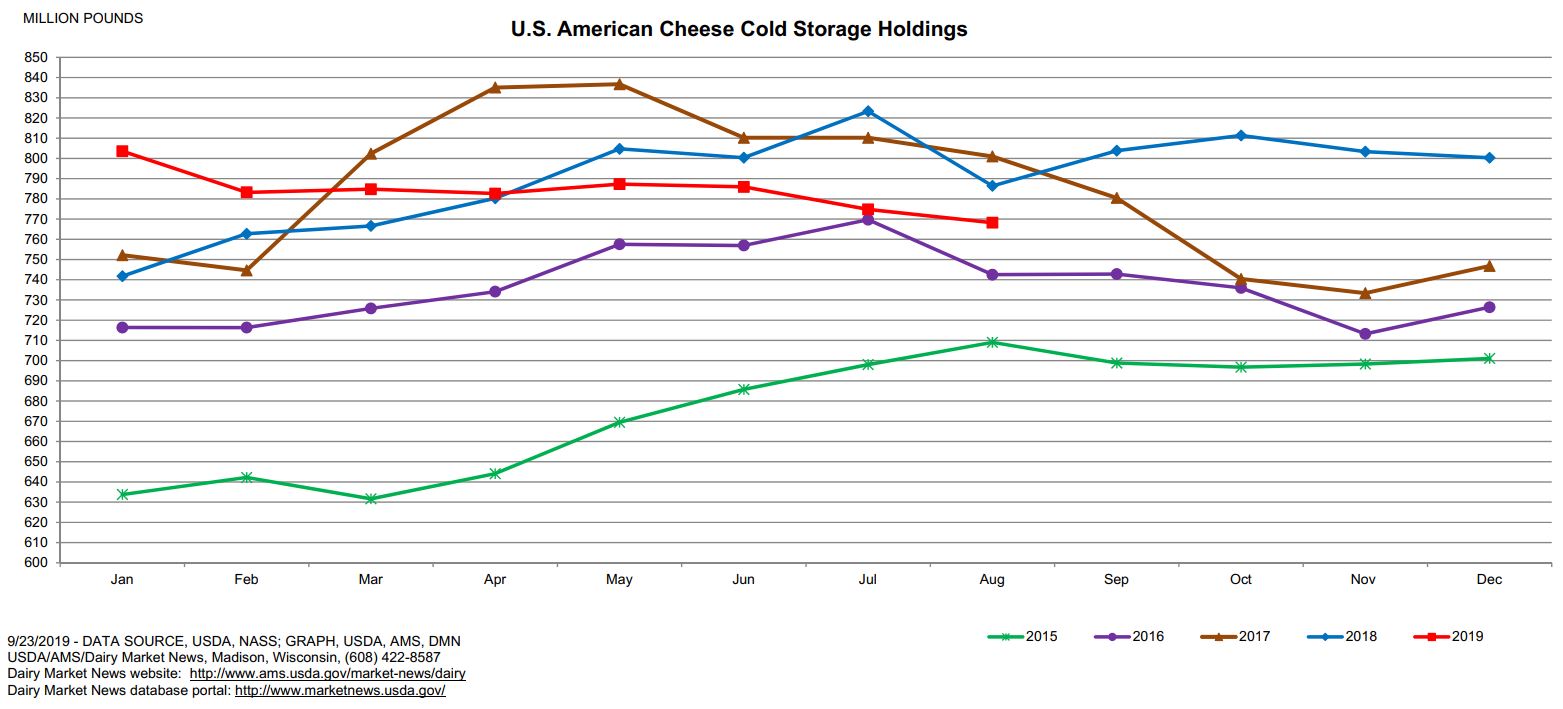

The only major report out this week was Cold Storage. Butter stocks at the end of August came in 5% higher a year ago, while American cheese stocks were down 2% from last year.

If you were to read Dairy Market News’ cheese updates over the past three weeks or so, they would largely look the same. Manufacturing milk is tight in the Midwest and East, in balance in the Southwest, and loose in the Pacific Northwest. That remains true this week, with cheesemakers in the Midwest reporting spot milk is tight and plants are now on 5-6 day workweeks. Domestic demand, as well, remains very good. So, we’re back to being a little perplexed over the market’s price action over the past couple weeks. Sure, we’ll concede prices went too high, too fast, but it was the nearly 31¢ drop in barrels from a high of $1.92 to a low of $1.6125 in a matter of just a little over a week that’s harder to explain. If there were so many barrels floating around, why did they spike so high in the first place. I think we’d all agree we’d much rather deal with a more stable, trending market, than the extreme volatility we just went through. That said, it did provide for some great hedging opportunities. So now the question is, where do we go from here? With both blocks and barrels both nudging higher on Friday, perhaps most of the bloodletting is over. With both block cheese and milk still on the tighter side in much of the country, and the peak demand season ahead of us, it would suggest at a minimum that the market shouldn’t collapse from here, and could find some bullish legs even. Current spot prices work out to about $17.45 Class III, not including NDPSR basis. With Nov Class III settling at $18.15 today, it’s trading just a slight premium to cash. Spot action next week will be key in determining where the front months go from here. The kind of whip-saw action we just went through may keep some buyers on the sidelines. Hedgers should consider selling some milk Nov-Jan on a rally. On the international front, New Zealand milk output in August was up just 0.8% YoY, while milk solids were up 2.2%. Australia is nearing its milk production peak, but much will depend on weather, as continued dry conditions hamper milk output in some areas. Milk output is declining seasonally in the EU, and July output was reported as up just 0.3% vs. last year. Globally, then, milk production is making very small, incremental gains. Market analysts Rabobank put out their quarterly report this week, suggesting the global dairy markets will remain firm thought the next six months. They expect demand growth to more than offset the modest increases in global milk production. For that reason, while rallies up front may be sold, we would not get too aggressive selling the 2020 contracts just yet.

Have a great weekend!