10/04/2019

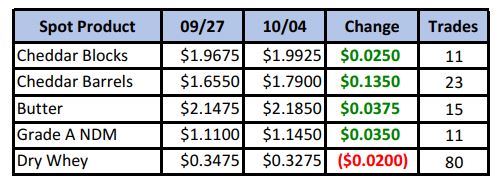

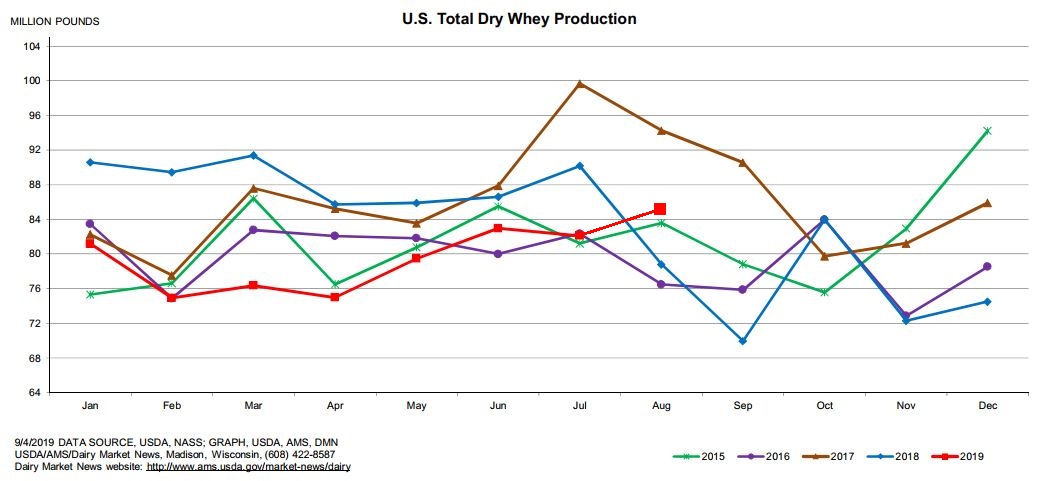

A record-breaking 80 loads of dry whey traded in this week’s spot market as the demand picture has weakened. Inventories are starting to build and the continuing spread of African Swine fever to other countries has the export outlook feeling grim. Sellers, then, were motivated to move product, leaving dry why 2 cents lower by week’s end. On the other hand, cheese and butter managed to regain some footing, while NDM pushed in to new multi-year highs.

Spot Market Recap

Futures Recap

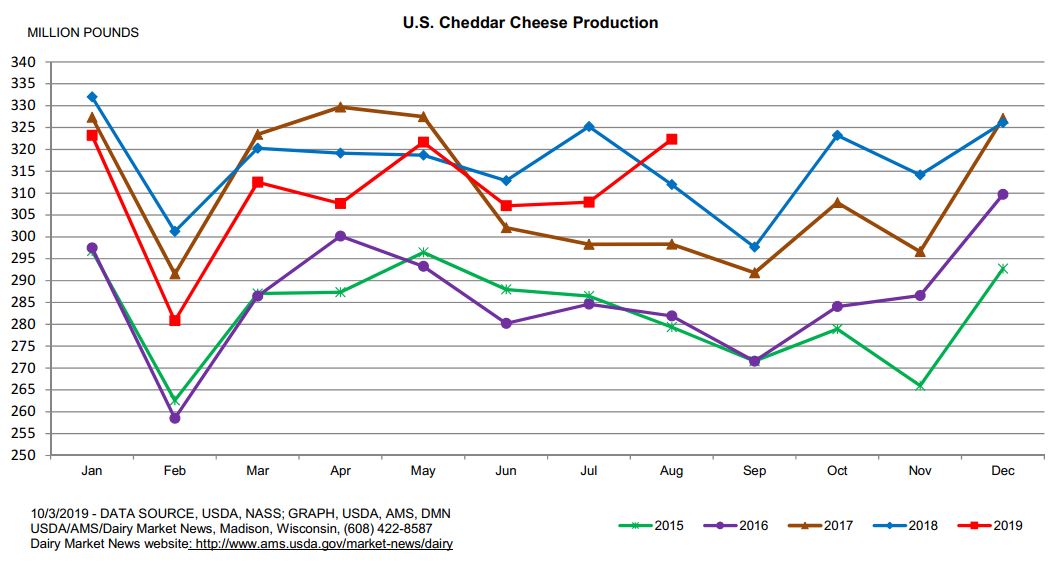

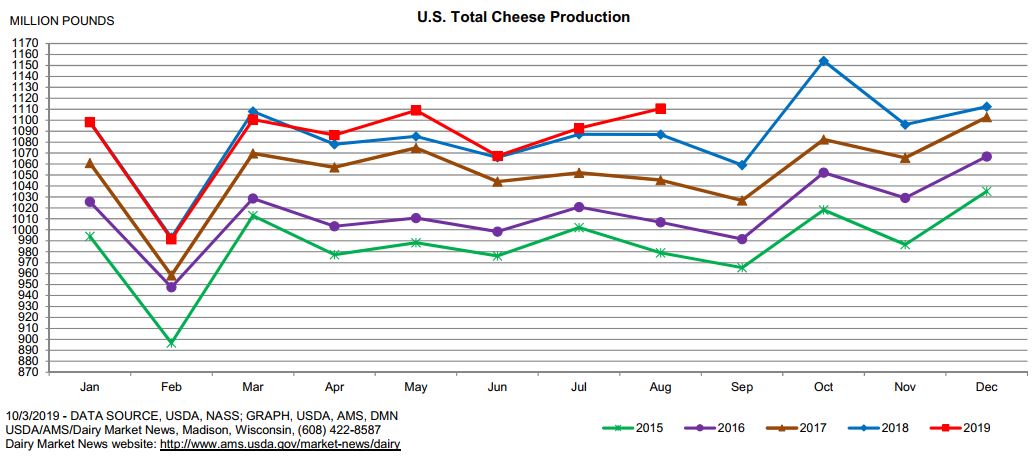

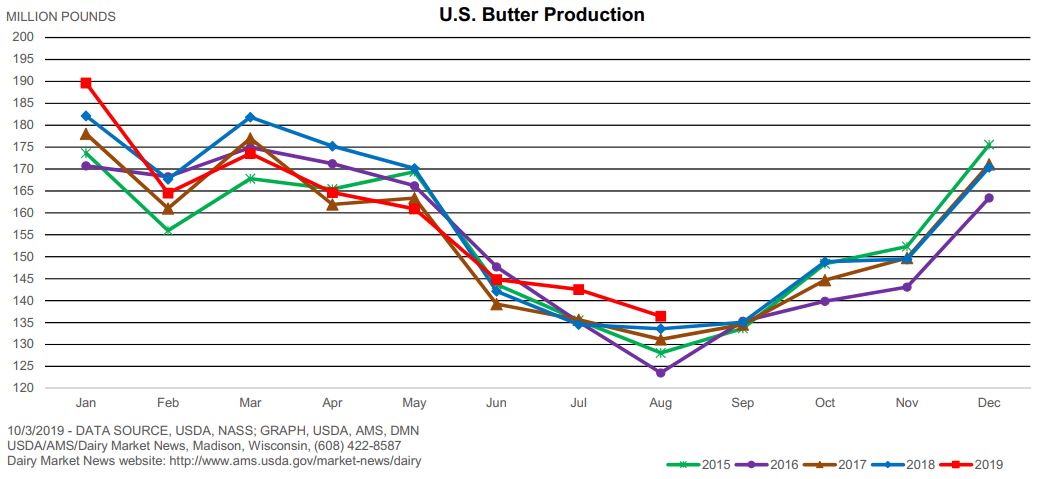

The Dairy Products Report was released Thursday and threw a bit of cold water on bullish cheese sentiment. Despite milk being on the tighter side in much of the cheese-making Midwest, according to USDA, American cheese output in August surged 5.1% higher than a year ago, and made an anti-seasonal move higher vs. July. The 458 million lbs produced set a new record for the month. The strong American cheese output carried total cheese output 2.2% higher YoY. Butter output in August was 2.1% higher than last year, but down 4.3% from July.

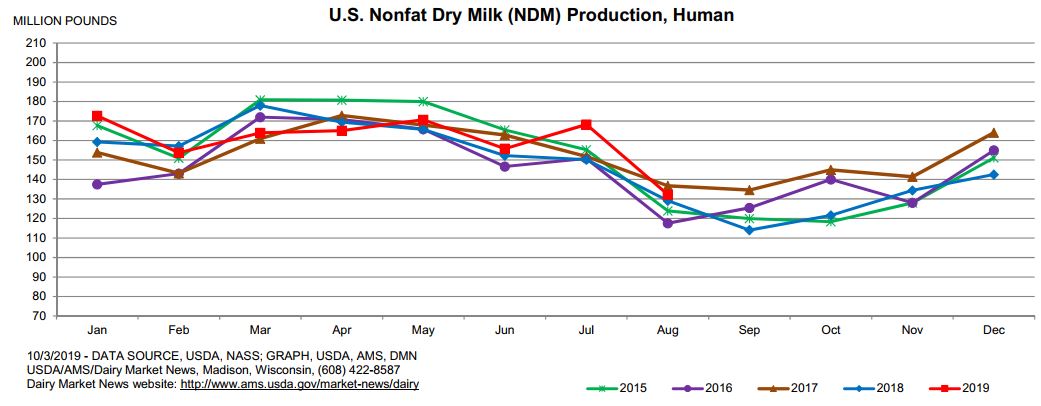

Moving to powders, total dry whey output in August was up a strong 7.2% while NDM output increased 2.5% YoY.

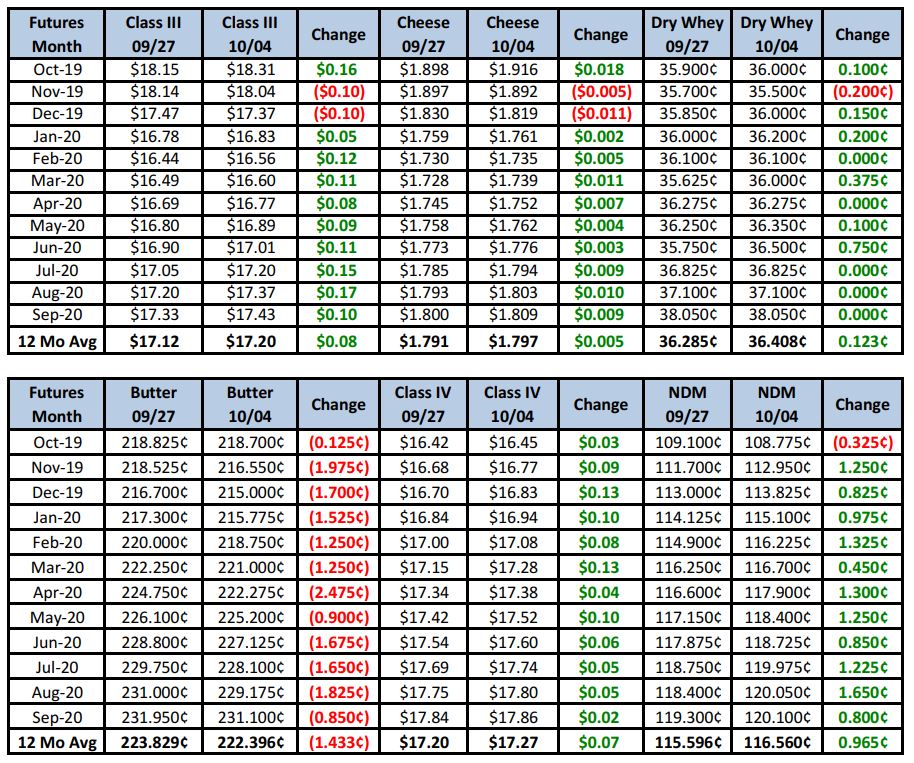

At first glance, these numbers are price-negative, especially cheese. But we also have to remember that this is data for August and it is now October. Block cheese is currently tight, so what happened to all the August cheese output? It could be an indication that domestic demand is very strong, or it was socked away in storage. Friday markets reacted poorly to the report, with futures up front predicting further spot cheese price declines. Current spot prices work out to about $18.25/cwt, not including basis, which would put it closer to the $18.60-18.70 level. Blocks gave up a bit of ground in today’s session, but barrels were higher. We’re not saying the market is wrong, but if current cheese tightness holds the next couple weeks, Q4 futures will eventually start climbing again.

Dairy cow slaughter for the week ending 09/21 totaled a solid 64,700 head, up 6.3% vs. the same period a year ago. Farms are still letting go of animals. This week’s Dairy Market News updates report there is little to no manufacturing milk available in the Southeast, and milk is being imported into the region to satisfy Class I needs. Milk output in the NE and Mid-Atlantic is flat. In the Central region, milk is tighter due to the pulls from the Southeast and spot loads were almost nonexistent. Those that did trade went as high as $1.50 over Class. Some farms are reporting feed is tight in the region. Heading west, the milk supply in CA is in balance with processors running close to capacity. In AZ and NM there is a good balance between supply and demand, while the Pacific Northwest remains in more of a milk glut situation. Discounted milk loads were reported at $4.75 below Class IV.

Cream is widely available across the country and butter output is steady. Demand is currently slow, giving a bearish tone to the market, but is expected to firm as we head in to the holiday season. We covered the negative sentiment on dry whey earlier, but the bullish tone remains around NDM. Supplies across the country are highly committed, while demand is up due to fortification of cheese vats and strong demand for protein components. Requests from the baking/cooking sector are also growing ahead of the holidays. Finally, Mexican buyers have been more active lately, improving the export picture of NDM.

Cheese output is steady across the country, but in the Midwest, plants are reporting lower output due to the scarcity in the milk supply. Some industry contacts in the region expect demand to remain strong for the rest of the year and into 2020. Midwest plants would like to add days to their current schedules, but are limited by the milk supply.

Not much to report on the international front. This week’s GDT saw the Dairy Price Index increase a modest 0.2%, but cheddar cheese fell 3.4% to a U.S. equivalent $1.69/lb. However, milk output in Australia is off to a slow start. August production was down 5.9% from a year ago, putting the current season (July-Aug) down 6.9% YTD. Global milk output remains on a very slow growth trajectory; smaller than demand growth.

So, that leaves us with a confusing market. We’re back again to skepticism in the face of mostly positive fundamentals. We’re encouraged by the strength in NDM. Recall it was the powder complex that led us to record milk prices several years ago. Class IV is still about $1.50 behind Class III, but if butter can find a bid, things could get interesting.

Our recommendation remains basically the same as last week. Take action in Q4 on substantial rallies and limit sales in 2020.

Have a great weekend!