09/20/2019

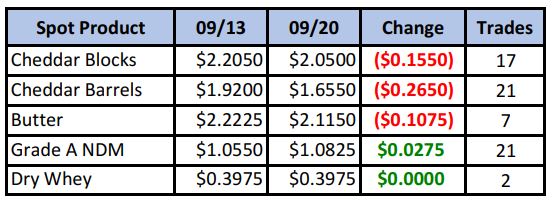

After pushing in to new highs on Monday, the spot market began to give up some ground on Tuesday, before completely falling apart on Wednesday and Thursday. Friday’s spot session saw the return of stability, but still left both blocks and barrels much lower than a week ago.

Spot Market Recap

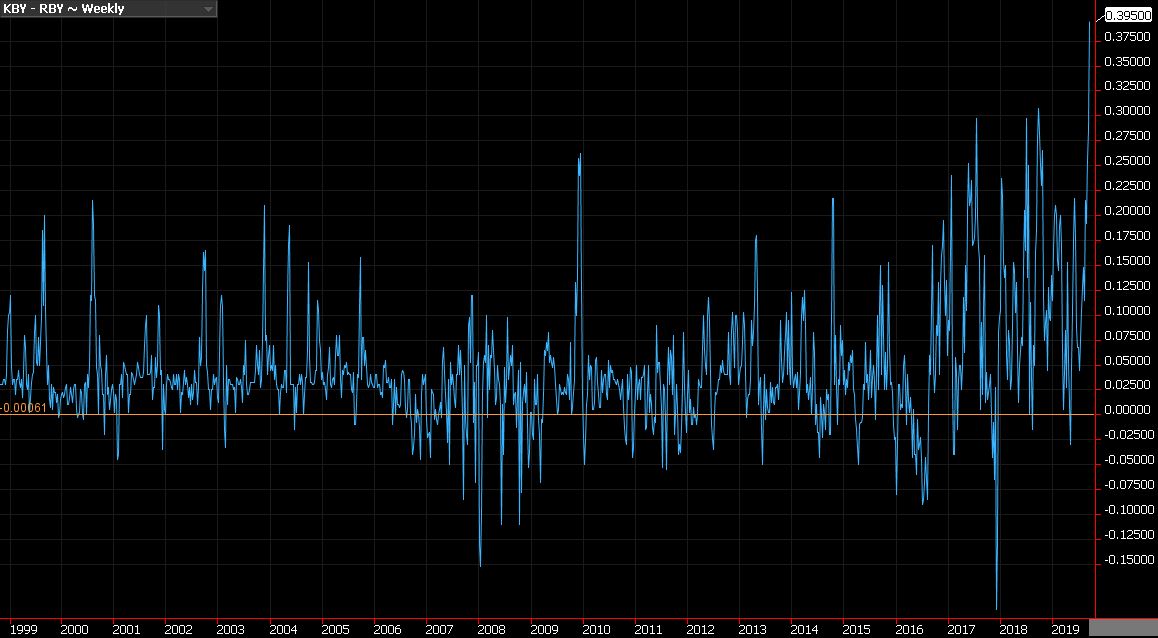

As a result, the block – barrel spread has never been wider. And we mean widest ever, like a 20-year wide of 39½¢, as shown in the weekly chart below, going back to 1999.

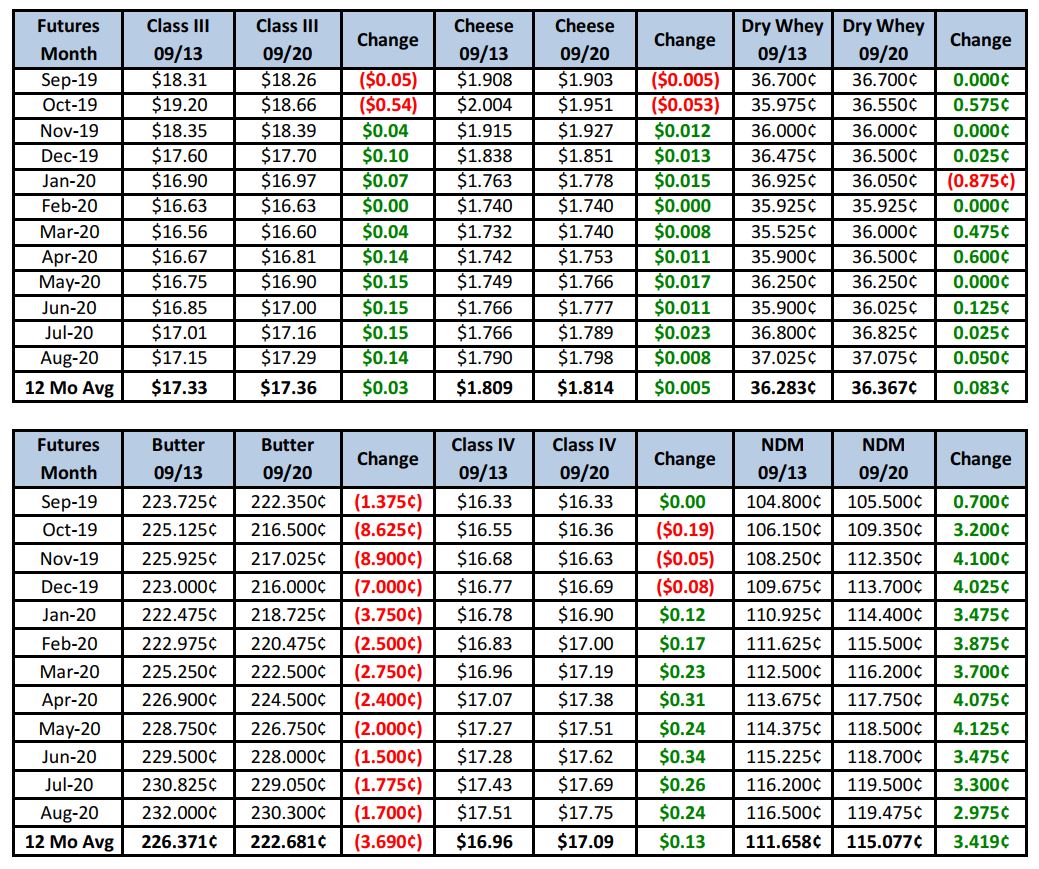

With the collapse in the spot market, October Class III saw a sharp loss, but remarkably, most other contracts finished the week higher. NDM was particularly strong.

Futures Recap

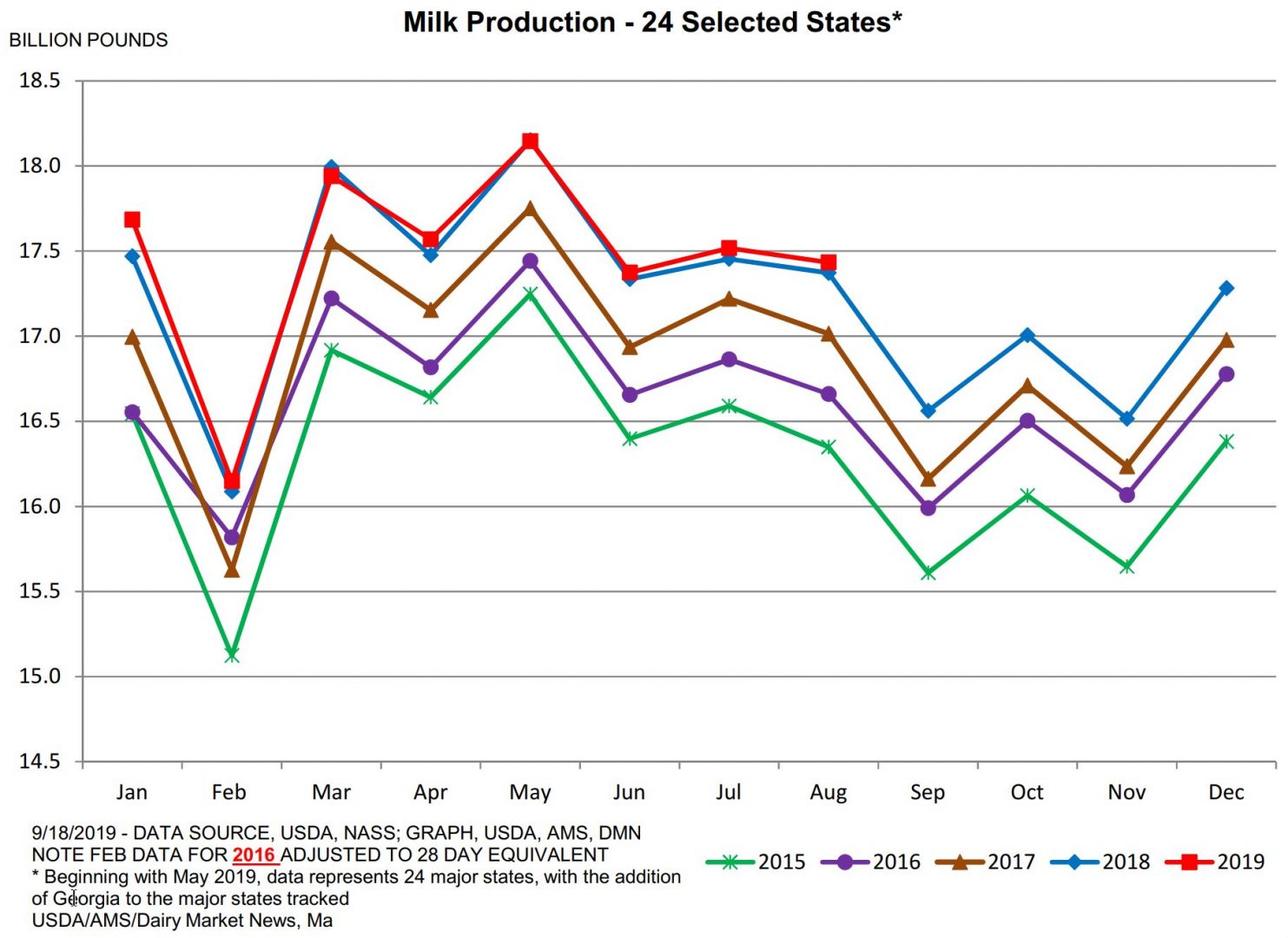

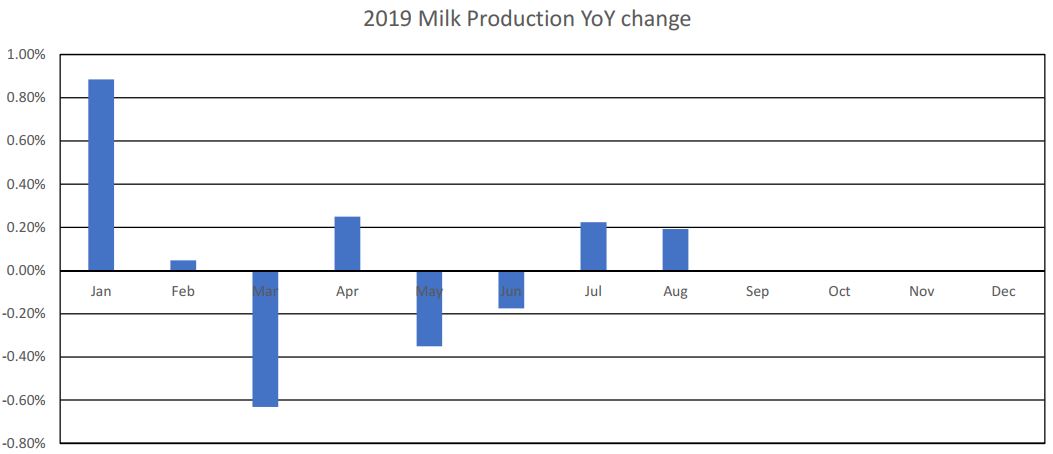

Heading into the hard data, this week’s Milk Production Report was mainly neutral to the market. Milk output in August was up 0.2% compared to a year ago. That limited growth should work longer term to support prices, as long as domestic demand remains strong.

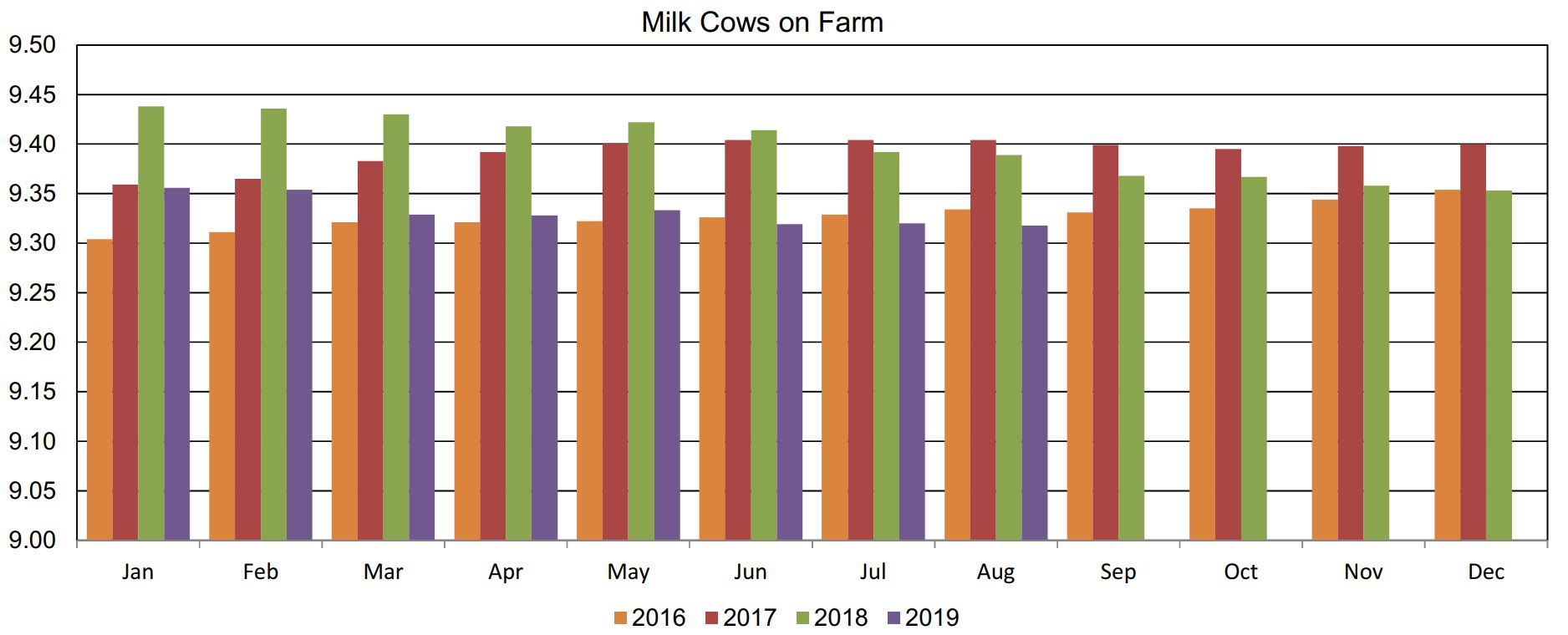

Cow numbers declined 2,000 head from July. At 9.318 million head, the herd is 71,000 cows smaller than a year ago.

Milk production was primarily up in the West, and down in the Midwest and Eastern regions of the country. In particular, output in the cheese-making state of Wisconsin was down 0.5% YoY while cow numbers fell 7,000 head.

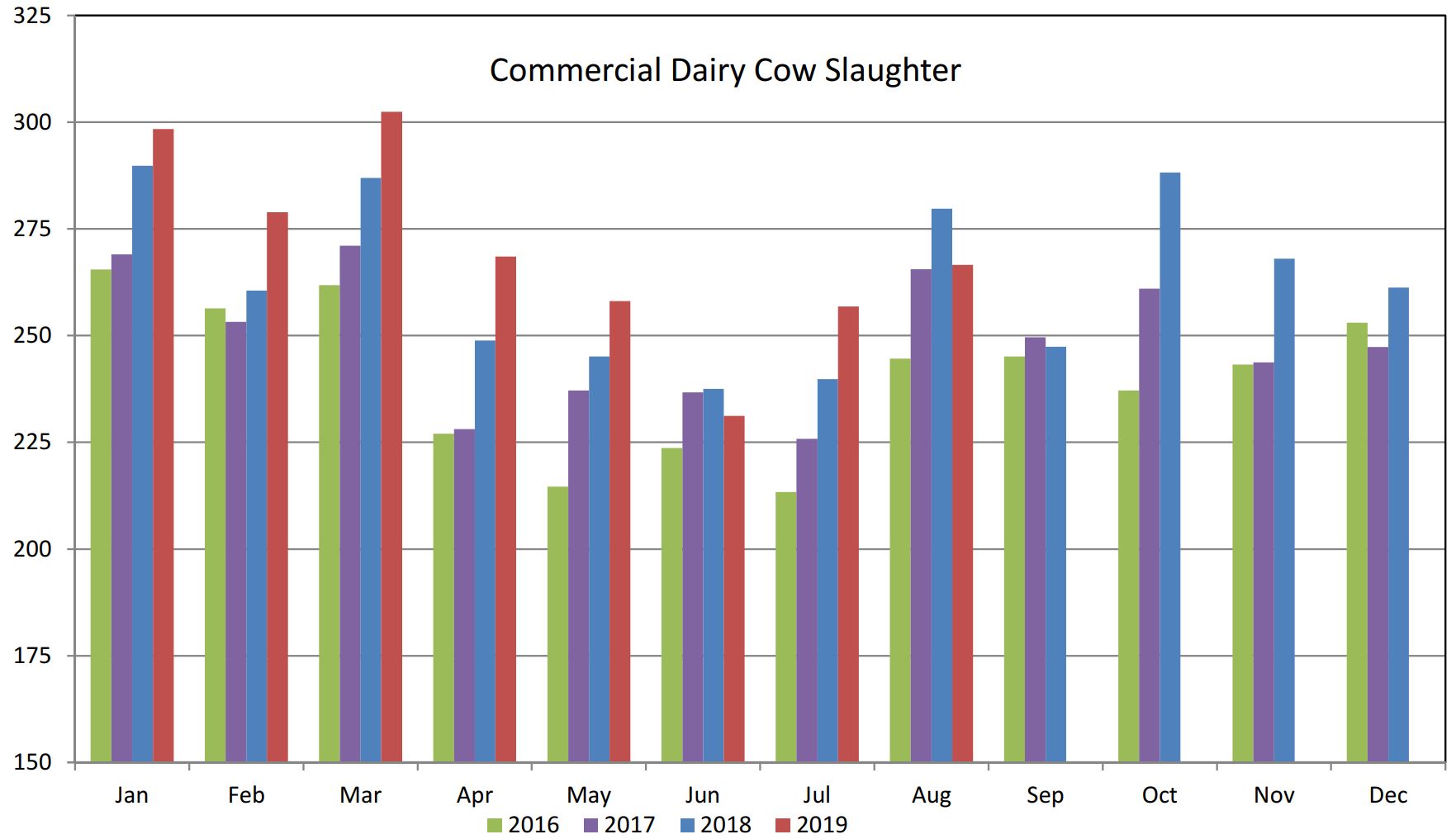

The Livestock Slaughter Report was also released this week. 266,600 dairy cows were removed from the herd in August, down 4.7% (13,100) from last August, but still the 2nd highest total since 2012.

Weekly number continue to forecast a slowing trend in culling. Dairy cow slaughter for the week ending 09/07 totaled 57,300 head, unchanged from the same period a year ago.

Dairy Market News reports milk availability in the Northeast is somewhat tight as strong pulls from Class I sales pull on the supply. Output in the Mid-Atlantic and Southeast regions is down and hot weather is still lingering in Florida. Production is steady in the Central region, the availability is tighter in the Midwest due to pulls from other regions. Spot loads of milk were reported at $0.25 to $1.50 over Class. Milk appears to be relatively in balance in CA and AZ, but in NM, milk flowing to Class III accounts has declined sharply due to a some downtime to one of the major cheese plants in the state. In the Pacific Northwest, milk production remains strong. Ideal weather is keeping output high and components near peak levels. As a result, processors are running near full capacity, while spot milk is being discounted at $4.75 below Class in ID.

Lots of cream and sluggish demand is keeping butter prices in check for now. However, the industry is looking forward to improved demand as baking season arrives.

The dry whey market is firming as cheese output is relatively flat due to limited milk availability in most regions. Likewise, the NDM market is seeing upward price pressure. Current demand is strong, especially for cheese fortification, while supplies are highly committed. Export demand from Mexico is very good, with new requests coming in. Spot availability is generally tight across the country.

Moving to cheese, Northeast participants report both domestic and international orders are strong and growing, while interest for Mozzarella from pizzerias is stable. Midwest manufacturers report stable sales, though barrel demand is off a bit. On the other hand, curd sales are still active. In the West, blocks are actually very tight, which is the first time we’ve heard that word used to describe cheese in the region for a long time. Cheese output is active and Mozzarella demand is improving.

After a limit up day last week, we had a limit down day this week, but overall, despite the rips up and down, the market tone remains positive. Cow numbers are not gaining any traction, milk output is muted, demand is very good, schools/football is open and holiday season must be in the back of long-term buyers’ minds. That said, the extreme moves are a reminder of how important it is to have a marketing plan and orders in place. We sold a lot of upper-$19 October milk this week, primarily as resting orders were picked off. We don’t yet know where October will settle, but those were good opportunities. What are your targets for Nov and Dec or the first half of 2020, or do you have any? Jan-Mar 2020 had a high settlement of $16.94. The market looks like it may re-challenge that level. What will you do if it does? Hedgers should be looking at pulling the trigger on DRP insurance and/or PUT options Nov-Mar. Call us and we’ll help you put a plan in place that will execute if and when the market moves in the desired direction.

Have a great weekend!