06/14/2019

Block cheese hit $1.80/lb for the first time since Feb 2017, before giving back some ground on Friday. Barrels were solidly higher, finishing the week up 7¢. That put the block/barrel average back above the previous double-top line. Currently at $1.69, the next target would be the previous highs made around the $1.75/avg level, back in the summer/fall of 2017 (see graph below).

Spot Market Recap

| Spot Product | 6/7 | 6/14 | Change |

| Cheddar Blocks | $1.7525 | $1.7825 | $0.0300 |

| Cheddar Barrels | $1.5350 | $1.6050 | $0.0700 |

| Butter | $2.3975 | $2.3650 | ($0.0325) |

| Grade A NDM | $1.0550 | $1.0525 | ($0.0025) |

| Dry Whey | $0.3650 | $0.3625 | ($0.0025) |

Spot Market Trade Volume

With both clocks and barrels finding bids, Class III futures finished the week higher, with double-digit gains in many contracts. However, dry whey and some butter futures contracts finished the week lower, responding to losses in their respective spot markets. Spot butter trading was heavy, with 47 loads exchanging hands.

Futures Recap

| Futures Month | Class III 06/07 | Class III 06/14 | Change | Cheese 06/07 | Cheese 06/14 | Change | Dry Whey 06/07 | Dry Whey 06/14 | Change |

| Jun-19 | $16.26 | $16.31 | $0.05 | $1.681 | $1.694 | $0.013 | 38.025¢ | 36.750¢ | (1.275¢) |

| Jul-19 | $16.64 | $16.85 | $0.21 | $1.722 | $1.751 | $0.029 | 37.125¢ | 35.750¢ | (1.375¢) |

| Aug-19 | $16.96 | $17.17 | $0.21 | $1.760 | $1.789 | $0.029 | 36.600¢ | 35.750¢ | (0.850¢) |

| Sep-19 | $17.27 | $17.44 | $0.17 | $1.787 | $1.813 | $0.026 | 36.650¢ | 35.600¢ | (1.050¢) |

| Oct-19 | $17.25 | $17.46 | $0.21 | $1.789 | $1.821 | $0.032 | 36.250¢ | 35.500¢ | (0.750¢) |

| Nov-19 | $17.13 | $17.32 | $0.19 | $1.780 | $1.805 | $0.025 | 36.025¢ | 35.550¢ | (0.475¢) |

| Dec-19 | $16.71 | $16.90 | $0.19 | $1.742 | $1.765 | $0.023 | 35.800¢ | 35.700¢ | (0.100¢) |

| Jan-20 | $16.37 | $16.46 | $0.09 | $1.708 | $1.718 | $0.010 | 36.000¢ | 35.925¢ | (0.075¢) |

| Feb-20 | $16.28 | $16.43 | $0.15 | $1.707 | $1.715 | $0.008 | 36.000¢ | 36.100¢ | 0.100¢ |

| Mar-20 | $16.25 | $16.40 | $0.15 | $1.709 | $1.719 | $0.010 | 36.025¢ | 35.725¢ | (0.300¢) |

| Apr-20 | $16.38 | $16.44 | $0.06 | $1.715 | $1.725 | $0.010 | 35.825¢ | 35.925¢ | 0.100¢ |

| May-20 | $16.46 | $16.56 | $0.10 | $1.725 | $1.735 | $0.010 | 35.625¢ | 36.125¢ | 0.500¢ |

| 12 Mo Avg | $16.66 | $16.81 | $0.15 | $1.735 | $1.754 | $0.019 | 36.329¢ | 38.000¢ | 1.671¢ |

| Futures Month | Butter 06/07 | Butter 06/14 | Change | Class IV 06/07 | Class IV 06/14 | Change | NDM 06/07 | NDM 06/14 | Change |

| Jun-19 | 237.025¢ | 237.025¢ | 0.000¢ | $16.80 | $16.80 | $0.00 | 103.850¢ | 104.225¢ | 0.375¢ |

| Jul-19 | 242.525¢ | 241.875¢ | (0.650¢) | $17.08 | $17.19 | $0.11 | 104.850¢ | 105.500¢ | 0.650¢ |

| Aug-19 | 243.925¢ | 243.750¢ | (0.175¢) | $17.26 | $17.42 | $0.16 | 106.325¢ | 107.350¢ | 1.025¢ |

| Sep-19 | 245.125¢ | 244.750¢ | (0.375¢) | $17.41 | $17.57 | $0.16 | 107.600¢ | 108.400¢ | 0.800¢ |

| Oct-19 | 243.250¢ | 243.925¢ | 0.675¢ | $17.47 | $17.63 | $0.16 | 109.325¢ | 110.000¢ | 0.675¢ |

| Nov-19 | 240.000¢ | 241.225¢ | 1.225¢ | $17.48 | $17.62 | $0.14 | 110.725¢ | 111.250¢ | 0.525¢ |

| Dec-19 | 233.025¢ | 235.475¢ | 2.450¢ | $17.28 | $17.46 | $0.18 | 112.125¢ | 112.425¢ | 0.300¢ |

| Jan-20 | 228.925¢ | 229.050¢ | 0.125¢ | $17.16 | $17.25 | $0.09 | 113.200¢ | 113.500¢ | 0.300¢ |

| Feb-20 | 228.575¢ | 228.475¢ | (0.100¢) | $17.17 | $17.21 | $0.04 | 114.000¢ | 114.700¢ | 0.700¢ |

| Mar-20 | 229.100¢ | 228.975¢ | (0.125¢) | $17.25 | $17.33 | $0.08 | 115.925¢ | 115.500¢ | (0.425¢) |

| Apr-20 | 228.000¢ | 229.000¢ | 1.000¢ | $17.32 | $17.36 | $0.04 | 117.100¢ | 116.075¢ | (1.025¢) |

| May-20 | 228.500¢ | 229.475¢ | 0.975¢ | $17.45 | $17.50 | $0.05 | 117.725¢ | 117.000¢ | (0.725¢) |

| 12 Mo Avg | 235.665¢ | 236.083¢ | 0.419¢ | $17.26 | $17.36 | $0.10 | 111.063¢ | 111.327¢ | 0.265¢ |

The July-Dec 2019 average pushed into new contract highs, before settling back a bit today at $17.19.

Meanwhile, the Jan-Jun 2020 average also pushed in to new contract highs, and added to them on Friday.

Both of these graphs show what a ride we’ve been on the past couple months. In particular, note how steep (fast) the rise has been. It hasn’t been without merit; there are plenty of factors that would argue for higher prices. But we’ve been around long enough to see sharp rises followed by some sharp corrections. We’re not advocating selling here, but you should do something to protect these prices. The July-Dec 16.50 PUT option averages 18.3¢ per month. Consider buying a floor there for your milk price. If the markets keep moving higher, take the higher price, but at least you’ll have some protection at a base price that is profitable for many operations.

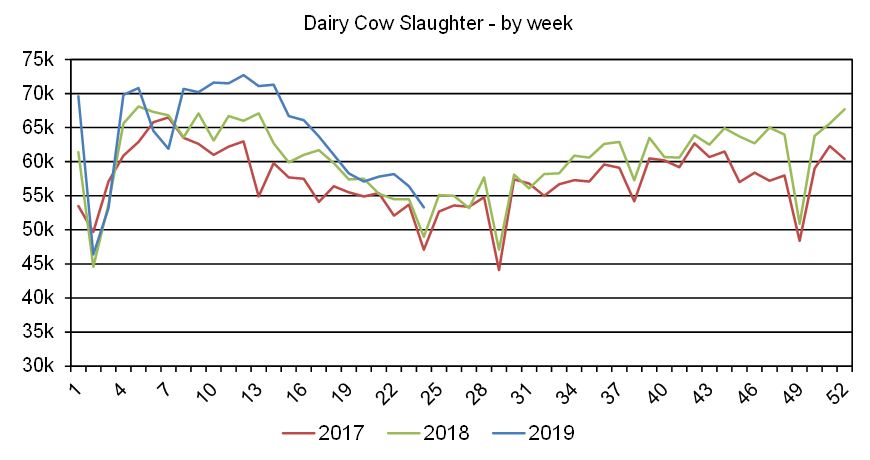

Taking a look at fundamentals, dairy cow slaughter for the week ending 06/01 totaled 53,300 head, up 8.8% vs. the same period a year ago. Slaughter number are definitely slowing down, but still pacing well above last year.

Cheese stocks at USDA-selected storage centers declined 161,000 lbs over the period 06/01 through 06/10, while butter stocks increased 1.3 million lbs. Nationally, cheese stocks remain heavy, but fresh cheese is in a more balanced position. The milk flow across the U.S. continues to be well under previous year flush levels. Processors have enough milk, but there is no deeply discounted loads. Midwest contacts are mostly positive about cheese supply/demand, but the higher block price has some buyers stepping back. Summer warmth is putting pressure on milk output in southern reaches of the U.S., while cooler regions continue to enjoy strong output. Cream is tightening across the country as schools let out and ice cream manufacturers compete for available loads. Dairy Market News reports bulk butter requests from wholesalers are very active, while print shipments into food service are robust. More active cheese output and the continued drag on sales from the swine flu virus had dry whey inventories creeping higher this week, and that put some pressure on prices. NDM trading was light this week, but contacts expect the market to return to a bullish tone. There are plenty of stocks on hand now, but the expectation is those will clear pretty quickly with lighter milk production later this summer. Grains continued to rip higher this week as planting progress remains well behind and crop conditions suggest yields will come down as the percent in the good to excellent categories do not come from the highest yielding states. Feed will be getting more expensive.

Current spot prices work out to about $16.45 Class III. With July futures beginning its calculation period next week, and settling at $16.85 today, it’s actually sitting at about parity with the spot market when weekly survey basis is added in. We wouldn’t be surprised to see a bit of a pullback to start the week, based on Friday’s price action and the somewhat high block price. No doubt there is some pushback at/near that $1.80 level, unless everyone is convinced we’re shortly headed to the $1.90 – $2.00 level; but the market doesn’t seem ready for that yet. That said, we still think downside is somewhat limited for blocks. End users should use dips as buying opportunities.

Have a great weekend!