06/07/2019

Block cheese continued to lead the way this week, reaching a price not seen since November 2017. With warmer weather now into much of the country and domestic demand seen as very good, it looks set to make new highs again next week.

Spot Market Recap

| Spot Product | 5/31 | 6/7 | Change |

| Cheddar Blocks | $1.7150 | $1.7525 | $0.0375 |

| Cheddar Barrels | $1.5400 | $1.5350 | ($0.0050) |

| Butter | $2.3600 | $2.3975 | $0.0375 |

| Grade A NDM | $1.0550 | $1.0550 | $0.0000 |

| Dry Whey | $0.3525 | $0.3650 | $0.0125 |

Spot Market Trade Volume

As block bids kept coming, increasing the spread, barrels, which had hit a low of $1.48½ on Tuesday, made an about face and gained the rest of the week. Barrels still settled the week down ½¢, but a massive 63 loads exchanged hands. Class III futures finished the week close to unchanged vs. last Friday, but also came well off their lows. Dry whey and butter futures continued to gain traction as well.

Futures Recap

| Futures Month | Class III 05/31 | Class III 06/07 | Change | Cheese 05/31 | Cheese 06/07 | Change | Dry Whey 05/31 | Dry Whey 06/07 | Change |

| Jun-19 | $16.20 | $16.26 | $0.06 | $1.677 | $1.681 | $0.004 | 37.350¢ | 38.025¢ | 0.675¢ |

| Jul-19 | $16.63 | $16.64 | $0.01 | $1.728 | $1.722 | ($0.006) | 36.500¢ | 37.125¢ | 0.625¢ |

| Aug-19 | $16.95 | $16.96 | $0.01 | $1.760 | $1.760 | $0.000 | 35.875¢ | 36.600¢ | 0.725¢ |

| Sep-19 | $17.22 | $17.27 | $0.05 | $1.794 | $1.787 | ($0.007) | 36.000¢ | 36.650¢ | 0.650¢ |

| Oct-19 | $17.18 | $17.25 | $0.07 | $1.790 | $1.789 | ($0.001) | 35.500¢ | 36.250¢ | 0.750¢ |

| Nov-19 | $17.05 | $17.13 | $0.08 | $1.774 | $1.780 | $0.006 | 35.525¢ | 36.025¢ | 0.500¢ |

| Dec-19 | $16.74 | $16.71 | ($0.03) | $1.742 | $1.742 | $0.000 | 35.525¢ | 35.800¢ | 0.275¢ |

| Jan-20 | $16.39 | $16.37 | ($0.02) | $1.710 | $1.708 | ($0.002) | 35.275¢ | 36.000¢ | 0.725¢ |

| Feb-20 | $16.32 | $16.28 | ($0.04) | $1.709 | $1.707 | ($0.002) | 35.025¢ | 36.000¢ | 0.975¢ |

| Mar-20 | $16.30 | $16.25 | ($0.05) | $1.710 | $1.709 | ($0.001) | 35.250¢ | 36.025¢ | 0.775¢ |

| Apr-20 | $16.35 | $16.38 | $0.03 | $1.720 | $1.715 | ($0.005) | 35.150¢ | 35.825¢ | 0.675¢ |

| May-20 | $16.54 | $16.46 | ($0.08) | $1.729 | $1.725 | ($0.004) | 35.200¢ | 35.625¢ | 0.425¢ |

| 12 Mo Avg | $16.66 | $16.66 | $0.01 | $1.737 | $1.735 | ($0.001) | 35.681¢ | 38.000¢ | 2.319¢ |

| Futures Month | Butter 05/31 | Butter 06/07 | Change | Class IV 05/31 | Class IV 06/07 | Change | NDM 05/31 | NDM 06/07 | Change |

| Jun-19 | 237.500¢ | 237.025¢ | (0.475¢) | $16.88 | $16.80 | ($0.08) | 104.000¢ | 103.850¢ | (0.150¢) |

| Jul-19 | 240.250¢ | 242.525¢ | 2.275¢ | $17.02 | $17.08 | $0.06 | 105.000¢ | 104.850¢ | (0.150¢) |

| Aug-19 | 242.500¢ | 243.925¢ | 1.425¢ | $17.24 | $17.26 | $0.02 | 106.525¢ | 106.325¢ | (0.200¢) |

| Sep-19 | 243.000¢ | 245.125¢ | 2.125¢ | $17.48 | $17.41 | ($0.07) | 108.350¢ | 107.600¢ | (0.750¢) |

| Oct-19 | 241.500¢ | 243.250¢ | 1.750¢ | $17.51 | $17.47 | ($0.04) | 109.850¢ | 109.325¢ | (0.525¢) |

| Nov-19 | 238.075¢ | 240.000¢ | 1.925¢ | $17.48 | $17.48 | $0.00 | 111.400¢ | 110.725¢ | (0.675¢) |

| Dec-19 | 232.000¢ | 233.025¢ | 1.025¢ | $17.28 | $17.28 | $0.00 | 112.500¢ | 112.125¢ | (0.375¢) |

| Jan-20 | 227.800¢ | 228.925¢ | 1.125¢ | $17.16 | $17.16 | $0.00 | 114.000¢ | 113.200¢ | (0.800¢) |

| Feb-20 | 224.625¢ | 228.575¢ | 3.950¢ | $17.15 | $17.17 | $0.02 | 115.450¢ | 114.000¢ | (1.450¢) |

| Mar-20 | 225.575¢ | 229.100¢ | 3.525¢ | $17.32 | $17.25 | ($0.07) | 116.950¢ | 115.925¢ | (1.025¢) |

| Apr-20 | 226.500¢ | 228.000¢ | 1.500¢ | $17.32 | $17.32 | $0.00 | 117.825¢ | 117.100¢ | (0.725¢) |

| May-20 | 226.850¢ | 228.500¢ | 1.650¢ | $17.45 | $17.45 | $0.00 | 118.750¢ | 117.725¢ | (1.025¢) |

| 12 Mo Avg | 233.848¢ | 235.665¢ | 1.817¢ | $17.27 | $17.26 | ($0.01) | 111.717¢ | 111.063¢ | (0.654¢) |

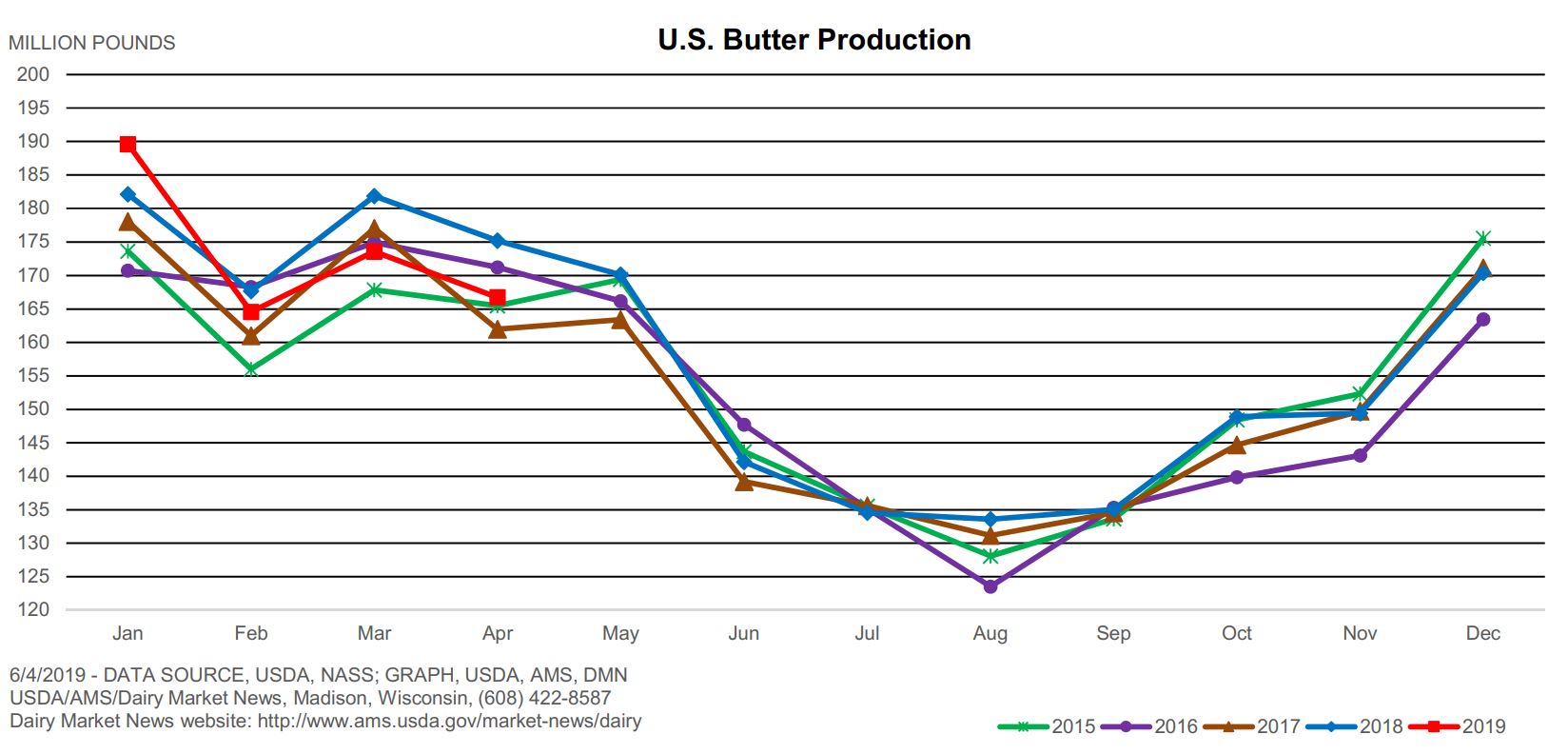

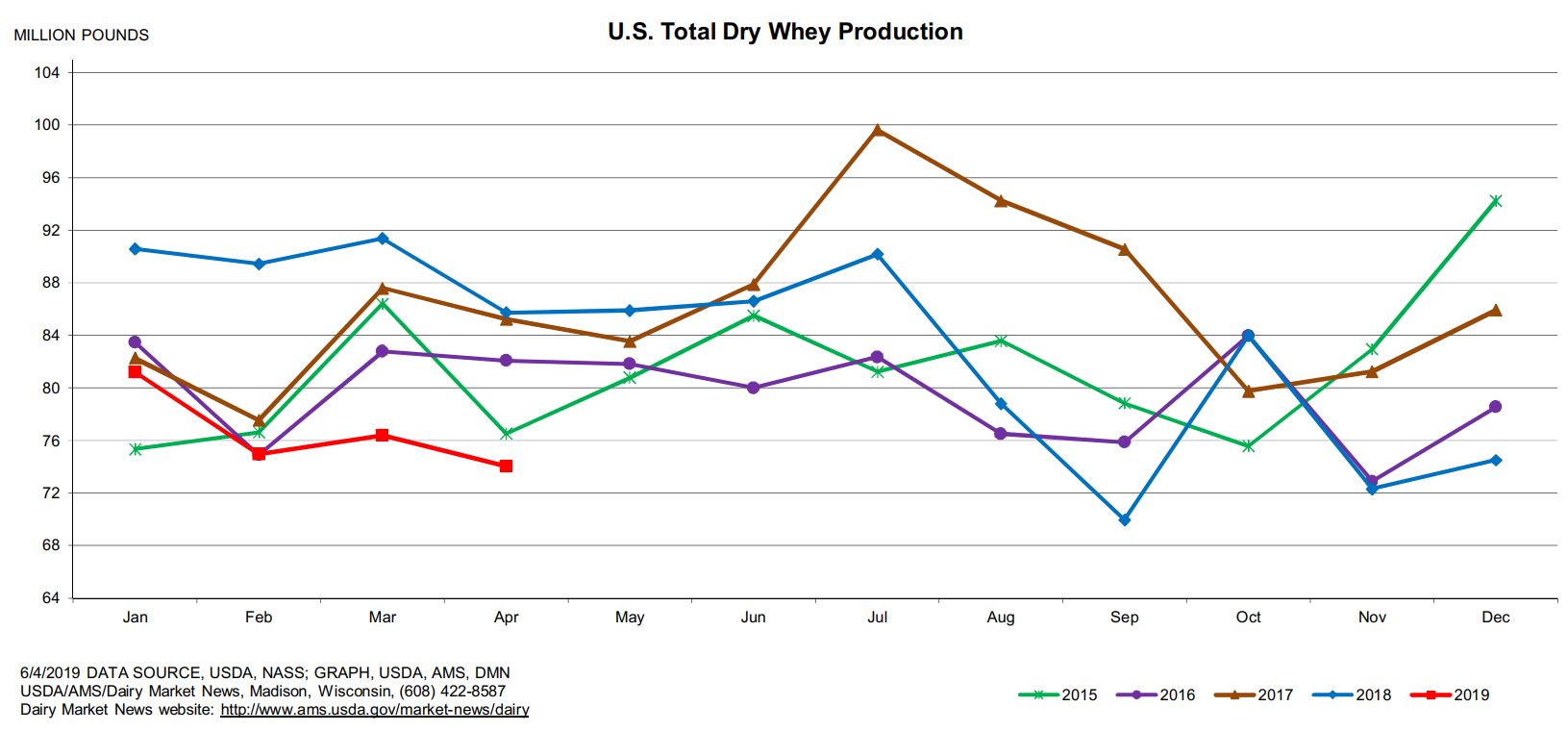

The Dairy Products report was released this week and was mostly supportive of the market. The rise in both butter and dry whey futures was most likely a response to the report, which had April butter output down 4.8% vs. a year ago.

Total dry whey output declined 13.7% vs. a year ago, which was also a 5-year low.

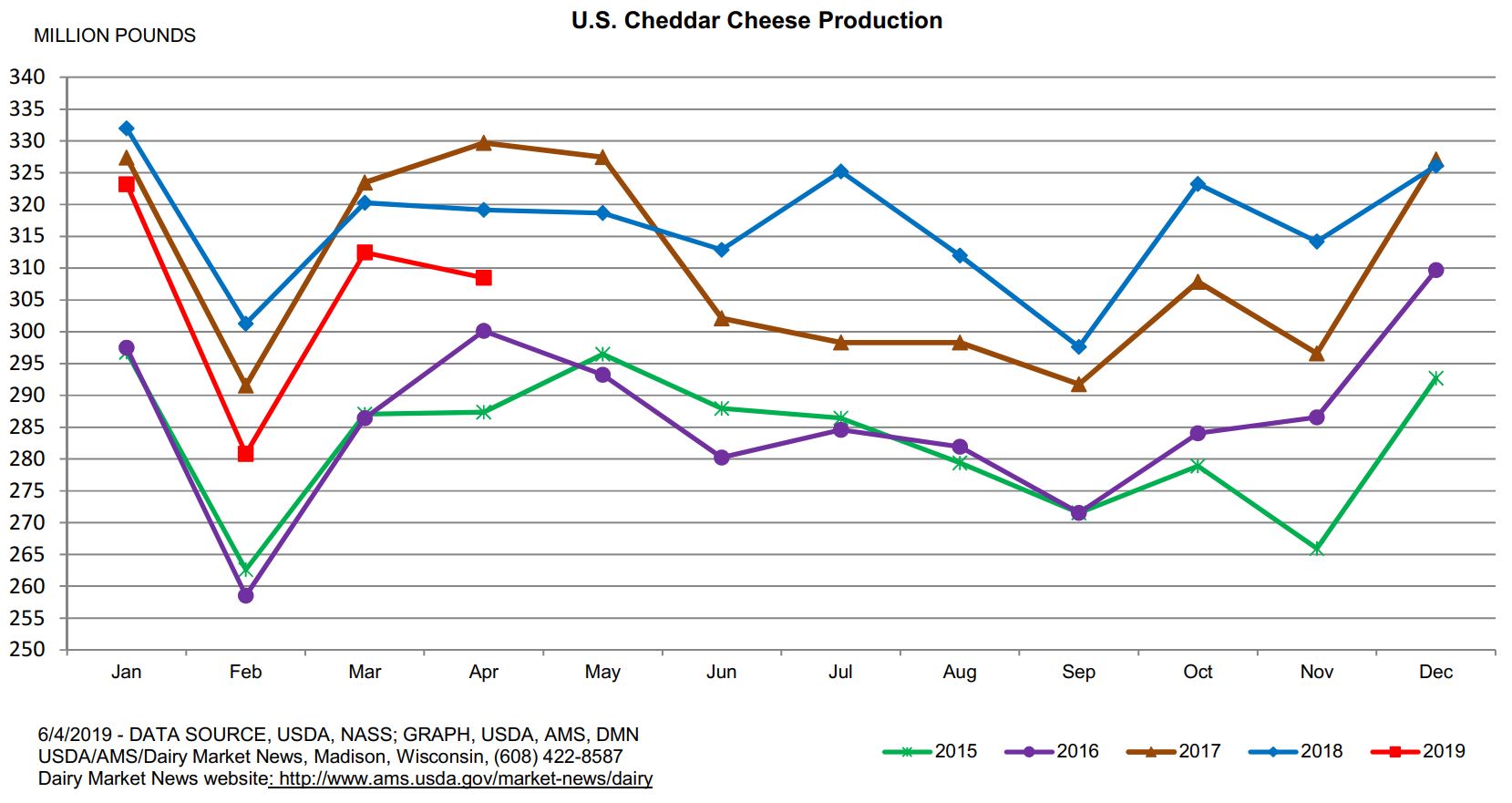

April cheddar cheese output was 3.3% lower than last year, and also below 2017 levels.

Total cheese output increased just 0.2% while NDM output saw a small 2.6% decline. Overall, the decline in the U.S. milking herd is having an impact on finished dairy product output.

Dairy Market News reports this week indicate milk output in Western Europe is below the desire of many dairy processors. EU Cheese output Jan-Mar was down 0.3% vs. 2018. Current stocks are at lower than desirable levels. Powder markets are beginning to firm as most current production is already committed.

In South America, milk output in Argentina, Uruguay and Brazil is significantly lower than levels of the preceding year. Several plants are running below full capacity.

In the U.S., milk output in the NE is edging seasonally higher and surplus milk is available. In the SE, milk output is level to lower as Florida is experiencing a heat index of over 100. Central region output is unchanged from last week, but concern is growing over wet, sloppy fields and what impact that will have on the feed supply. Spot loads remain priced close to Class. In the West, most states are past the peak, with improved Class III sales being reported, with the exception of the Pacific NW, where output is still quite heavy. Cream supplies in the region continue to tighten. Cheese supplies are still heavy on a national level, but cheese makers in the Midwest are starting to look for more milk. Supplies are even described as somewhat “snug”.

The on-again, off-again tariff talk ended on a positive note this week, with the U.S. administration reporting they are hopeful additional tariffs against Mexico can be avoided. Talks with China continue at a slower pace, but there was some optimism reflected by both sides this week.

June is finally here and the market seems to have found some stability. The recent decline in barrels may have been due to a drop-off in exports, according to our sources, resulting in bringing the product to the spot market. It was encouraging to see buyers take on 63 loads this week and we’re hopeful that trend will continue. We continue to hear about farms closing, with some chat about a multi-thousand operation in WI shutting down. Sad to hear, but it does reduce the milk supply.

Who knows what, if any impact the undercover videos shot at Fair Oaks Dairy will have, either on the industry, or their operation. They milk well over 30,000 cows.

It’s always hard to predict the market in the short-term. Strength in the block market looks set to continue next week. With WI still making the most cheese in the nation and many farms in the Midwest being hardest hit, we continue to have a more bullish bias longer term. We would continue to hold off selling 2020 milk, and would target the mid-$17’s or higher in Q3 and Q4. Have a great weekend!