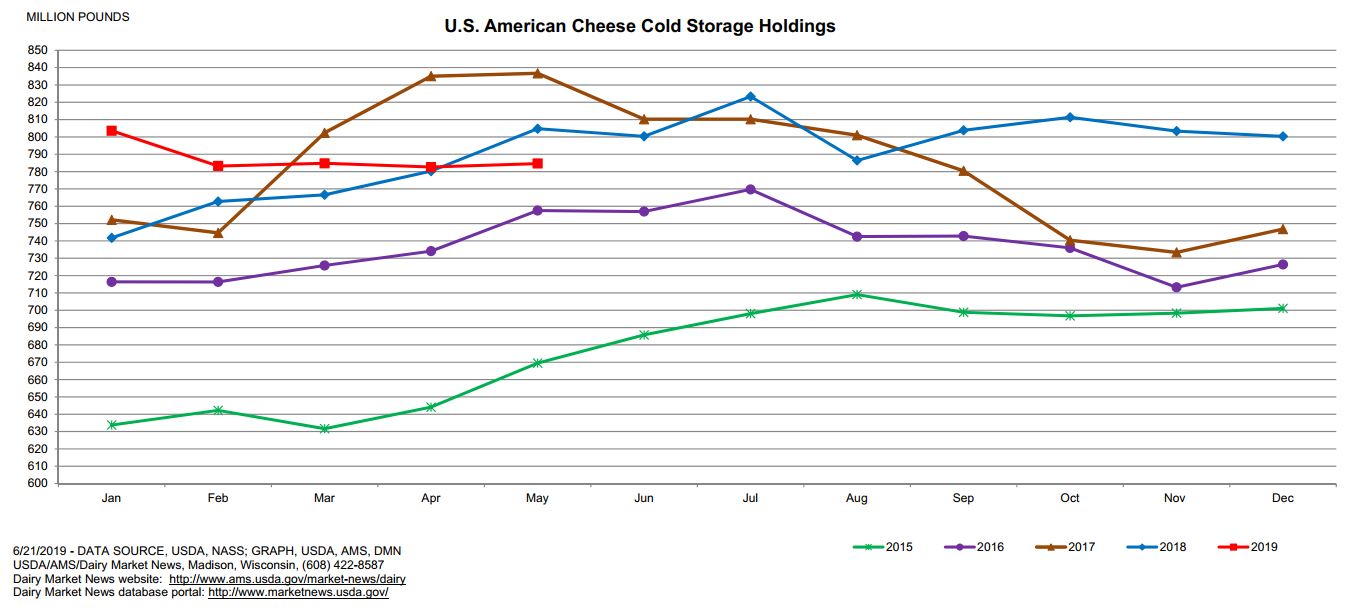

06/21/2019

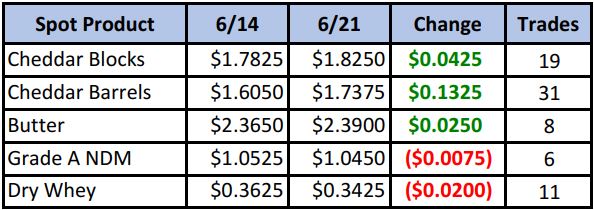

Spot cheese was the star again this week as blocks pushed in to new highs for the year and barrels came within a half cent of matching its 2019 high. The block/barrel average at $1.78/lb settled at a level not seen since Nov 2016. Spot butter picked up some ground this week as well, but both NDM and dry whey finished the week lower.

Spot Market Recap

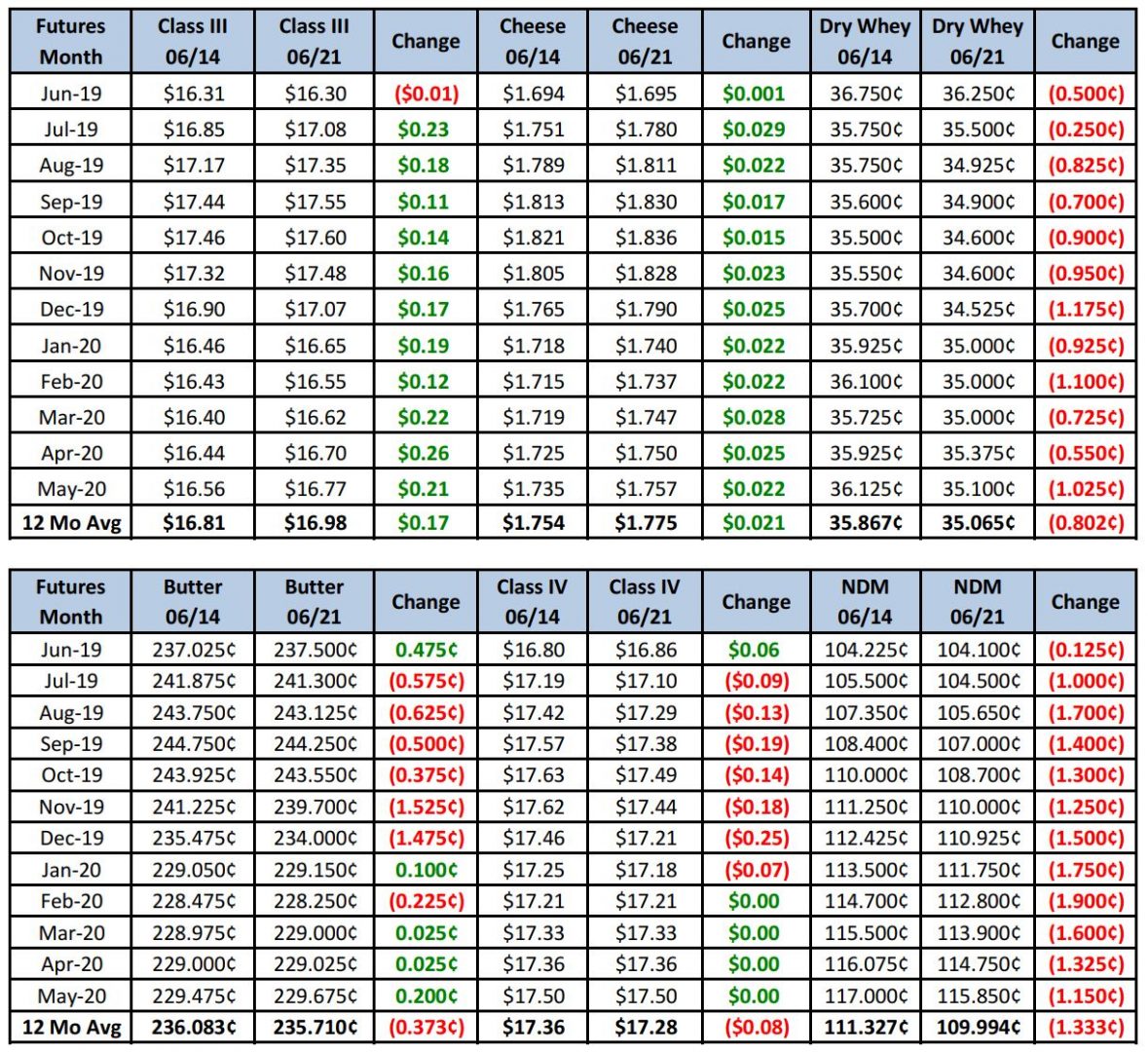

Class III and cheese futures finished solidly higher across the board, while the other Class III components saw mostly red. Notably, the Class III 2020 contracts began to see more interest and had a solid week as well.

Futures Recap

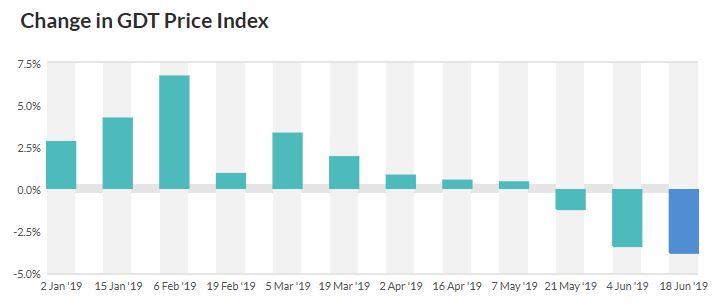

It was a data-filled week, so lets get right to it. Tuesday started with the morning results of the GDT auction, which were less than inspiring. The dairy price index fell for a third straight time and by the biggest percentage (-3.8%). Losses were led by butter, down 5.7% and cheddar cheese, down 4.3%.