10/26/2024

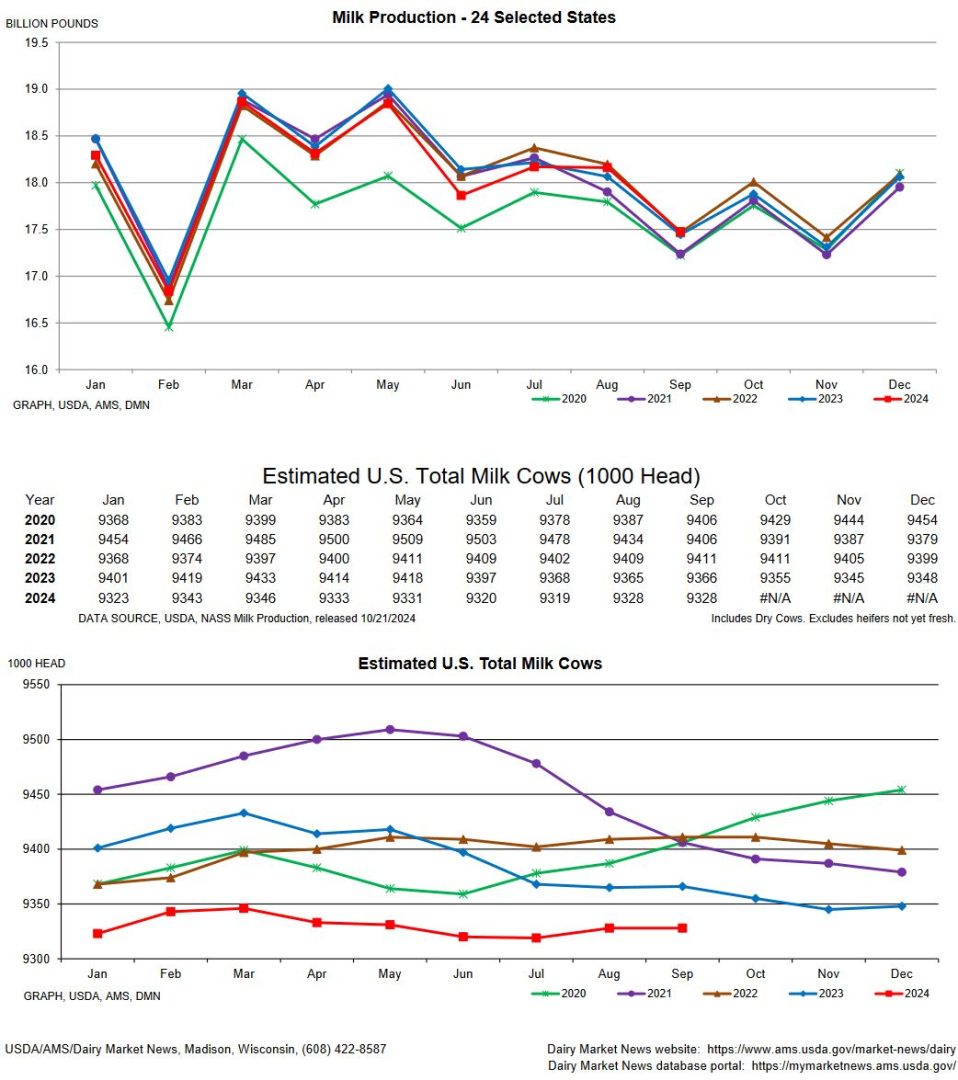

Milk production continues to hold steady despite the drop in cow numbers from last year. With 38 thousand less cows; milk production was up slightly from a year ago. This weighed heavily on the market with blocks and barrels finishing the week in the red. Cold storage came out at the end of the day on Friday and should give next week a boost. It was down 1 percent from last month and down 7 percent from last year.

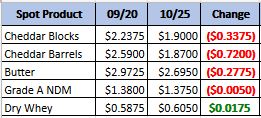

Monthly Spot Prices Comparison

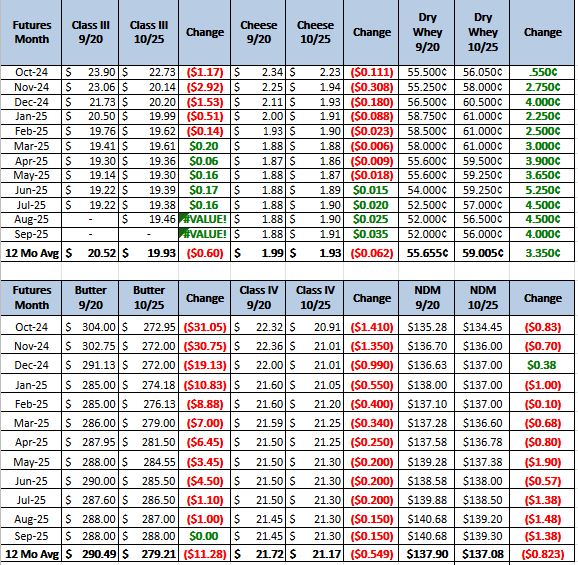

Monthly Future Prices Comparison

Cheese: Cheese production is mixed throughout the U.S. In the East, cheesemakers note steady production schedules. Regional milk availability is not adequate to meet local processing needs, and some contacts shared they are bringing in loads of milk from milk handlers in the West. Cheesemakers in the Central region note milk availability is steady. Spot milk volumes were reported at $1.50 below Class III to $2.50 above Class III. That said, plant managers continue to relay some downtime for maintenance, and cheese production schedules are mixed. Retail demand is strong, and while customer inquiries are growing, there is minimal spot cheese availability. In the West, cheese production ranges from steady to stronger. Class III milk availability is adequate to meet regional processing needs. Contacts note domestic cheese demand is steady. (USDA Cheese Highlights)

Butter: In the East region, retail butter demand is steady to weaker as a large portion of retail orders have been fulfilled. In the Central region, demand is steady to increasing. Butter inventories are sufficient to meet seasonal needs. Domestic and export demand is steady in the West. Cream volumes are widely available across the country. Plenty of cream is moving throughout the regions with some processors preferring to sell the excess cream, if possible. Scheduled maintenance and unexpected plant downtime are being seen in plant operations in all regions. Despite interruptions, butter churning paces are noted as strong across the nation and busier than is normal for this time of year. Bulk butter overages range from 1 to 8 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Dry whey prices ticked higher on the bottom of the range and held steady elsewhere. Suppliers continue to report significantly tight availability. They have suggested if they had spot loads available, those would be offered out in the low/mid $.60s/lb range. However, production is currently focused on contract fulfillment. Negotiations for 2025 contracts are underway. Milk availability in the region is not markedly available. There are growing concerns in California regarding recent output decreases in recent weeks, as triple digit

temperatures remained in the Central Valley until early October. Class III processors are actively seeking out extra milk loads. That said, drying whey has slid on the priority ladder due to consistently bullish market sentiment for whey protein concentrate 80% and whey protein isolates. Dry whey market tones are firm and expected to remain so for the near-term. (USDA Dry Whey)

Demand is starting to outpace supply and with the recent drops in prices I would expect that to continue. We do need a strong holiday and football season to push into the 22 – 23, dollar range. I do expect to see the buyers to be back in the market after the cold storage report. Although, I would not get your hopes up that it will be good forever. Look to take advantage of the next rally and get some coverage well into 2025. Recommendation, buy call and call spreads to cover sold contracts or in anticipation of selling contracts on the next rally.