9/27/2025

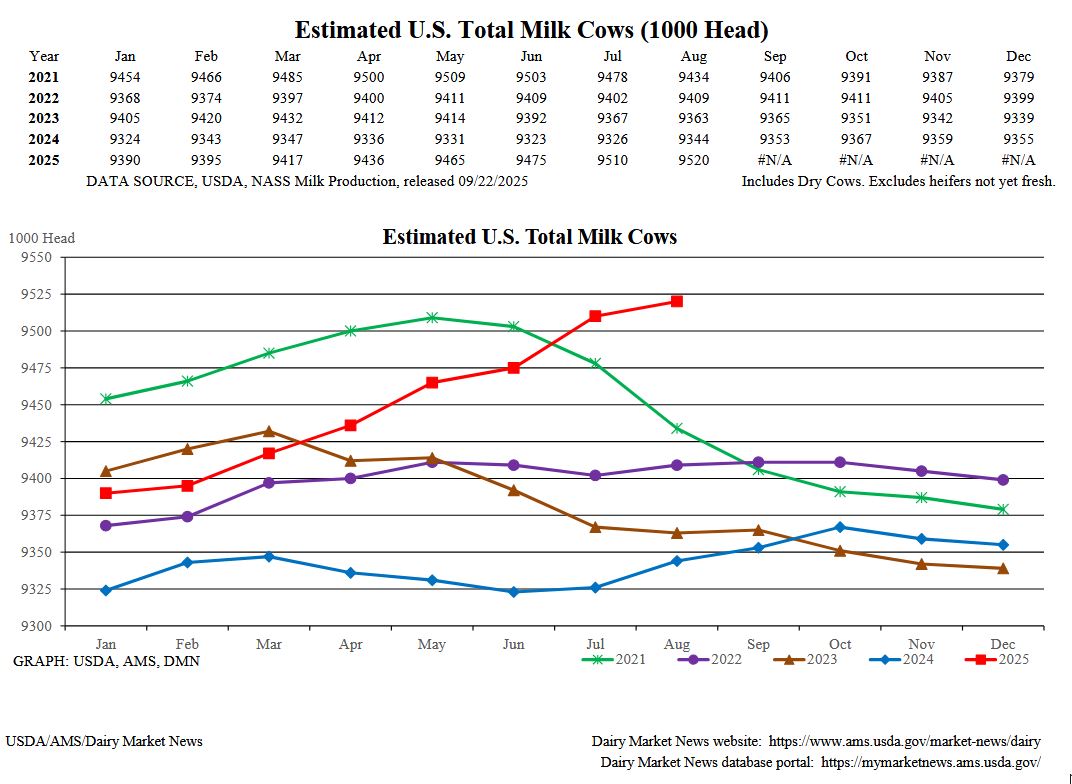

This week we had the production report and the cold storage report for August. Production report was another big number. With good weather and cow numbers up, it is a perfect storm for milk to come pouring in. This is the second month in a row that we have seen milk production over 3 percent. The abundance of milk has weighed the market down as prices on the spot market have been bouncing around in the 1.60’s. Cold storage came out on Friday, and it was down 1 percent. Therefore, even with the elevated production demand is using it up.

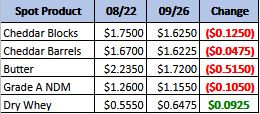

Monthly Spot Prices Comparison

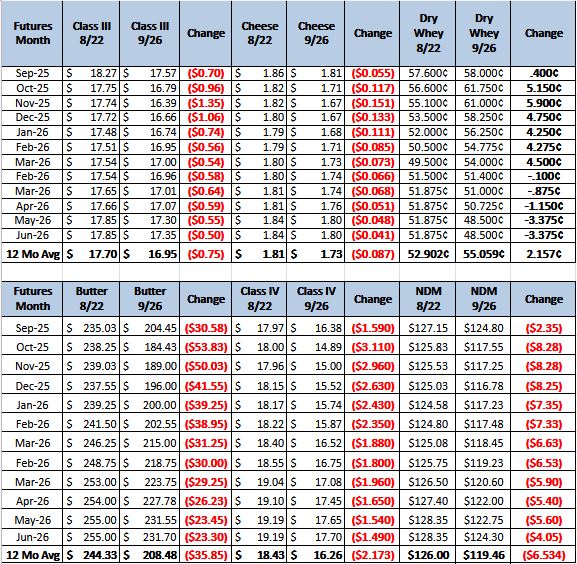

Monthly Future Prices Comparison

Cheese: Cheese makers in the East are beginning to fill holiday orders. As a result, production is increasing in many facilities. Milk and condensed skim are available for spot purchase in the region. Export demand is also increasing, keeping cheese inventories balanced. Cheese production is steady in the Central region. Class III spot milk is available, but some manufacturers are not able to take in much additional milk over their contract loads. Domestic cheese demand is steady, and export demand is growing. In the West, cheese production varies from steady to stronger. Class III spot loads of milk are available. Export demand for cheese is rising for some producers. Domestic demand is steady. The increasing export demand, according to some producers, is keeping a floor on domestic prices. (USDA Cheese Highlights)

Butter: Contacts generally report either steady or lighter domestic demand for butter. Central and West region contacts note stronger export butter demand, while East region contacts note slow activity. Cream is widely available and continues to be more affordable for Class IV manufacturers. Butter manufacturer demand for spot cream loads is mixed. Butter churning activity varies from steady to stronger. Production schedules are more focused on retail butter loads than bulk butter loads. Unsalted butter availability is somewhat tight. CME

closing butter prices for September 22 through September 25 are lower compared to week 38. Bulk butter overages range from 2 cents below to 5 cents above market across all regions. (USDA Butter Highlights)

Dry whey: Prices were unchanged across the price range and the mostly price series this week. Spot inventories are tight, and some manufacturers are sold out of dry whey for near term shipment. Stakeholders say there is more dry whey available in the Southwest than in the Central region. Domestic spot trading is limited by light availability, but some spot purchasers are, reportedly, taking a step back to see where dry whey markets are going before securing additional loads. Export demand remains light. Cheesemakers are running busy production schedules, leaving plenty of liquid whey available for drying. Plant managers say they are primarily using this liquid whey for higher whey protein concentrates, keeping dry whey production limited. Prices for animal feed whey were also unchanged this week. Demand for animal feed whey remains light and spot inventories are tight amid limited production. (USDA Dry Whey)

Going into the fall the above graph is going to be the one that makes or breaks milk. Right now, cow numbers are heading to an area that will weigh on the market. Good exports have kept the dairy market in a range from 1.60 cheese to 1.80 cheese, but the highs are starting to be lower on every rally. With fast food medium pizzas at a lower price point then most fast-food burgers we should see good cheese demand domestically this fall. Exports continue to be strong for cheese, but the World market has started to drift lower. Recommendation at this point is to sell into rallies. This is a good demand time of year, but the current milk production is going to keep a lid on how high the price can go. I am going to be travelling up to Wisconsin in the next two weeks and still have some availability on the 8th and 9th of October. If you are interested in meeting give us a call.