9/22/2024

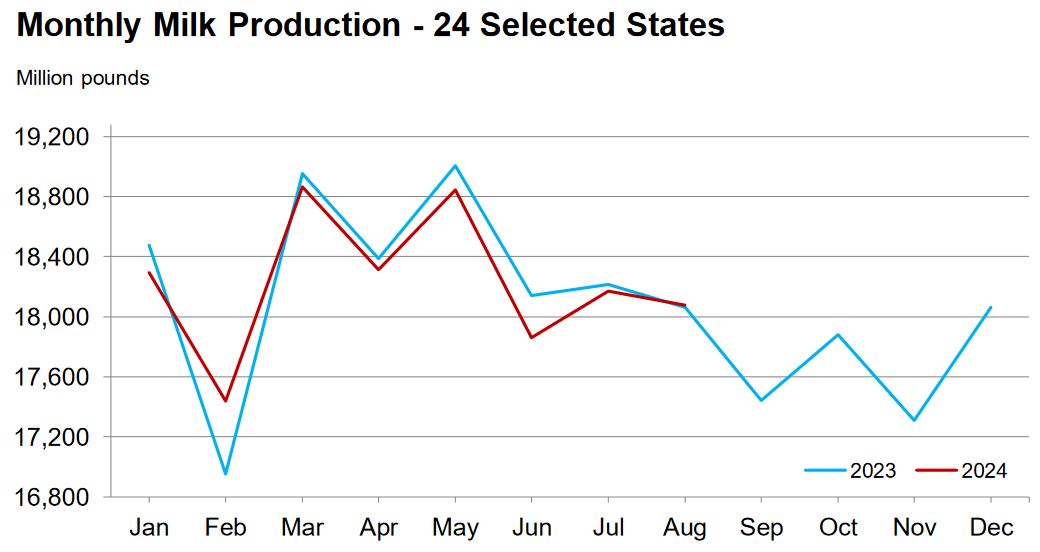

After a few weeks of buy pressure sellers showed up this week. With spot prices well above October futures, the market is looking for more selling as we go into the next couple of weeks. Milk production was out this week and even with lower cow numbers production came in a little above last year. With cheap feed and higher milk prices the name of the game is to maximize the production of every cow.

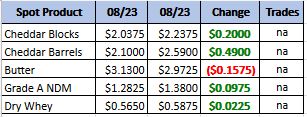

Weekly Spot Prices

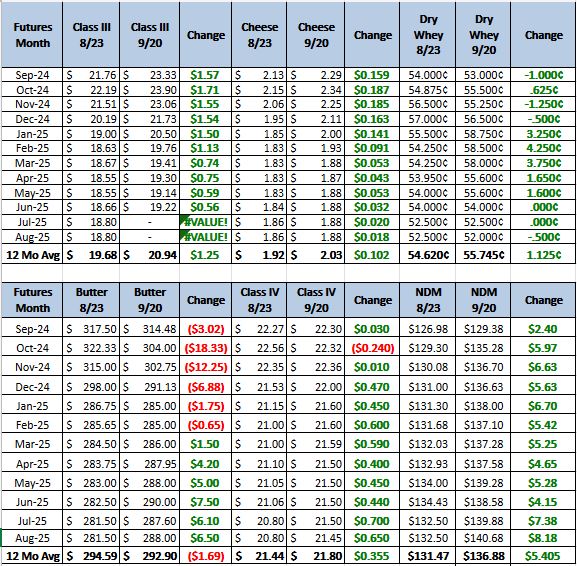

Weekly Future Prices

Cheese: Contacts share mixed cheese production throughout the U.S. Cheesemakers in the East note limited spot milk availability as Class I demand draws upon milk volumes available for cheese processing. Contacts note demand for several cheese varieties is steady to stronger. In the Central region, contacts note plant maintenance and downtime have freed up some milk supplies for processors. For the first time in several weeks, spot milk prices were reported below Class III, ranging from $0.75 below to $3.50 above Class III. Cheesemakers in the region say production efforts are geared toward upcoming holiday demands. Barrel inventories have grown enough to accommodate spot purchases. In the West, cheese manufacturers relay steady to stronger production, despite variable spot milk availability. Cheese inventories in the region are mixed, with barrel inventories noted to be especially tight. (USDA Cheese Highlights)

Butter: Butter demand in the East is steady. Butter demand is picking up in the Central region. For the West region, salted butter demand is steady, but unsalted butter demand varies from steady to lighter. Cream volumes are generally available throughout the country. However, cream volumes are comparatively tighter in the Northeast part of the nation. Butter production varies from strong to steady in the West. In the Central and East regions, butter producers convey production schedules are busier than expected. Butter manufacturers suggest production paces are comfortable for anticipated Q4 demands. Bulk butter overages range from minus 5 cents to 10 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Dry whey prices are unchanged for the range. The bottom end is unchanged, while the top end moved slightly higher. Domestic demand is steady. However, some buyers are pushing back on offered spot loads as prices near the 60-cent mark. Demand from international buyers is stronger. Dry whey stocks are tight, especially for some grade or brand specific loads of dry whey. A few delayed deliveries are noted. Dry whey production is mixed. Whey protein concentrates, and especially whey protein isolates, continue to have strong demand drawing whey solids away from sweet whey production. (USDA Dry Whey)

Milk is starting to loosen up as we move into the fall. With some extra loads moving below class. This market is starting to look a little top heavy. Milk production for August was better than expected and even with the heat the cows are out producing last year. Milk production is still limited with a smaller herd size for this next year and therefore, I do not see a big crash coming. With that said a $3 plus drop would not take most dairy farmers out of profitable ranges. Recommendation, sell, I would look to get the rest of 2024 done and make a good start on 2025. Demand is going to be the big mover in the next year so look to the overall economy for bigger price moves on class 3.