8/24/2025

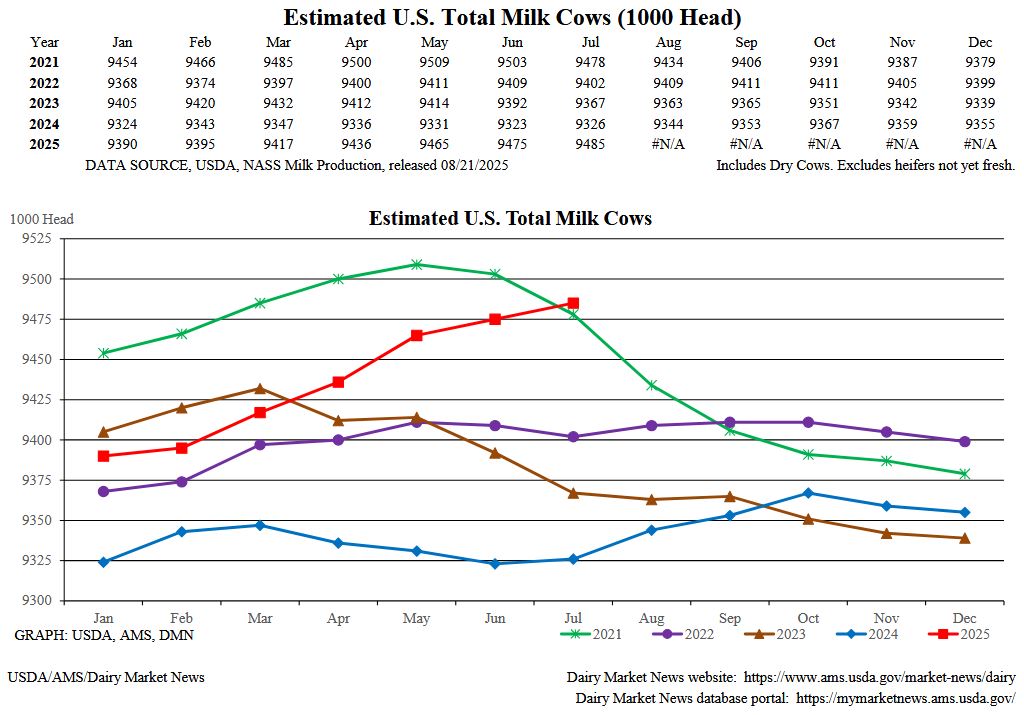

This week we had the production report and the cold storage report for July. Production was up more than expected, at 3.4 percent with and cow numbers 154,000 more than last year. This was a bigger jump then most were expecting and dipped going into Friday. The biggest gains were in Kansas, South Dakota, and Texas all in line with new cheese plants that have gone online in those states this year. Cold storage followed a day later with the numbers up 1 percent from last year but down slightly from last month. That means even with a pick-up in production cheese is in balance. All in all this week I do not see these reports pushing the market to far in ether direction.

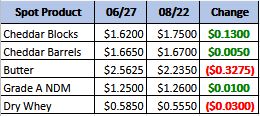

Monthly Spot Prices Comparison

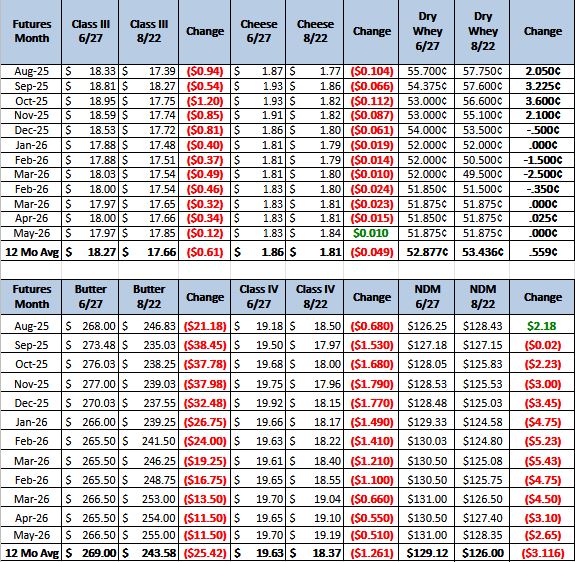

Monthly Future Prices Comparison

Cheese: Milk availability remains tight in the Northeast. Bottling production and demand from cheese makers is keeping spot availability of milk low. Cheese production is good and keeping pace with demand. Inventory levels of cheese are holding steady this week. Milk output in the Central region is mostly steady but still trending lower, as variable heat and stormy weather continue to influence conditions. Contacts note incoming milk inventories are up slightly. Spot milk remains in strong demand, with Class III ranging from $3- under to $2-over, as of reporting. Cheese productions are steady to lighter as plant managers cite limited spot milk availability.

In the West, contractual milk volumes are being met for cheese manufacturers despite some lighter milk output being noted. Demand for Class III spot milk loads from cheese manufacturers is mixed. Stakeholders indicate prices for US produced loads are generally attractive to international buyers. Demand from international buyers varies from steady to stronger. (USDA Cheese Highlights)

Butter: West region contacts report mixed domestic demand. Central and East region contacts report strengthening domestic demand, boosted by the upcoming holiday. Demand from international buyers is strong. Some butter manufacturers note international buyer interest is outpacing production of international butter loads. Availability of spot cream loads is ample, but not abundant. Demand for spot cream loads from butter manufacturers is mixed. Production schedules vary from steady to stronger. Many butter manufacturers are more

focused on retail butter production than bulk butter production. Bulk butter overages range from 5 cents below to 5 cents above market across all regions. (USDA Butter Highlights)

Dry Whey: Prices slipped at the top of the range this week, while the bottom of the range and the mostly price series held firm. Production strengthened, with manufacturers running heavier schedules and making some product available to the market. Spot loads are moving with fewer constraints, and inventories are no longer viewed as tight. The animal feed whey price range is unchanged, with demand described as steady to light. (USDA Dry Whey)

Going into the fall the above graph is going to be the one that makes or breaks milk. Right now, cow numbers are heading to an area that will weigh on the market. Good exports have kept the dairy market in a range from 1.60 cheese to 1.90 cheese. With fast food medium pizzas at a lower price point then most fast-food burgers we should see good cheese demand domestically this fall. As long as exports continue cheese is likely to stay range bound. On the other hand, 2026 needs to be a spot dairy producers need to get some coverage. At this point the recommendation would be for put spreads but also consider selling rallies. Give us a call for a specific hedge plan to meet your needs.