11/23/2024

In the last two months the milk market has gone from not enough milk and prices may go to all-time highs. To now looking at going back into the red for most dairy farmers on cost of productions. Production has pushed above year ago levels for the last two months, led by big gains in Texas and South Dakota. On the demand side exports have been good but domestic demand has been lackluster. This has kept the buyers on the sidelines and the spot cheese market has dropped more than 90 cents from the highs.

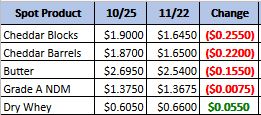

Monthly Spot Prices Comparison

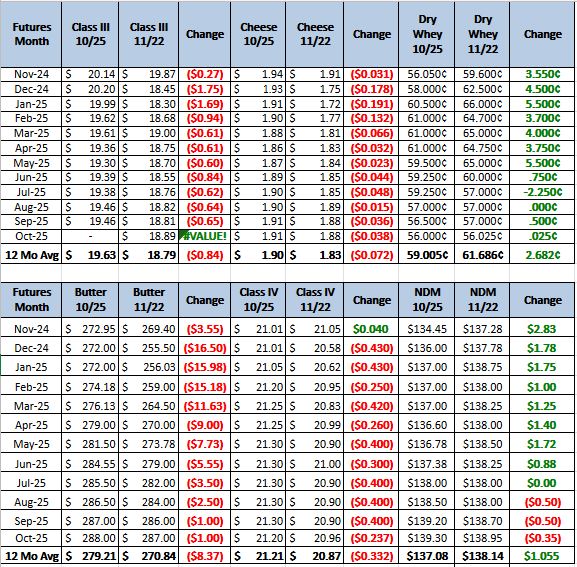

Monthly Future Prices Comparison

Cheese: Cheese production varies throughout the U.S. In the East region, milk volumes range from steady to tighter. Cheese plant managers relay steady production schedules ahead of Thanksgiving and note inventories are more balanced now than earlier in the year. In the Central region, milk availability remains mixed. Spot milk loads were reported at Class to $4 above Class III. Some cheese plant managers relay slower production schedules as holiday cheese orders have been fulfilled. Contacts in the West region share steady cheese roduction schedules. Spot milk loads are tighter in the southwest. Contracted cheese demand is steady. Export activity is trending steady to stronger. Price points for domestic cheeses are competitive on an international scale. (USDA Cheese Highlights)

Butter: n the East and Central regions, domestic butter demand is mixed for both the retail and food service sectors. In the West region, near- term domestic butter demand is lighter. Cream volumes are generally readily available across the country. Many butter manufacturers are not purchasing additional loads of cream, as in-network and/or contracted volumes of cream are sufficiently accommodating butter churning schedules in many cases. For the East and Central region, stakeholders indicate butter production is steady. For the West region, stakeholders indicate steady retail butter production and lighter bulk butter production. Bulk butter overages range from 1 to 8 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Prices moved higher on the bottom ends of the range. The top ends of the range were unchanged. Demand from domestic and international buyers is steady. Stakeholders convey stocks of both preferred and nonpreferred brands continue to be tight. Some dry whey manufacturers indicate availability of Grade A dry whey loads remains extremely limited for spot load buyers. Strong market strength for whey protein concentrates and isolates continues to be a contributing factor in the tight dry whey spot load scenario. Dry whey production schedules are mixed. (USDA Dry Whey)

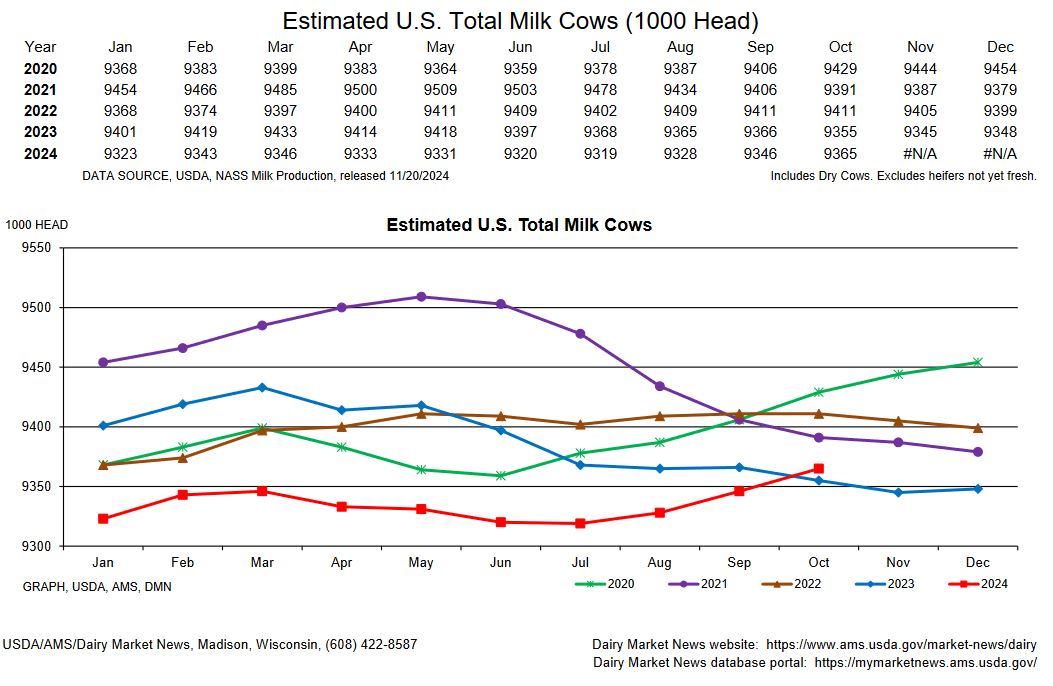

Cow numbers are the story this week as the October production report showed total number of milk cows going above last year. This has been the first increase in milk cow numbers since May of last year. Heifer numbers are tight and expensive with some reports of milk cows fetching north of 3k. With cheaper feed this year and a high milk price farmers are holding on to their cows longer and doing what they can to expand their herds. With that in mind I do not see a bottom in the market yet. Our recommendation is to get covered through the first half of the year. Give us a call this next week and we can get more specific with recommendation to suit your needs.