4/6/2025

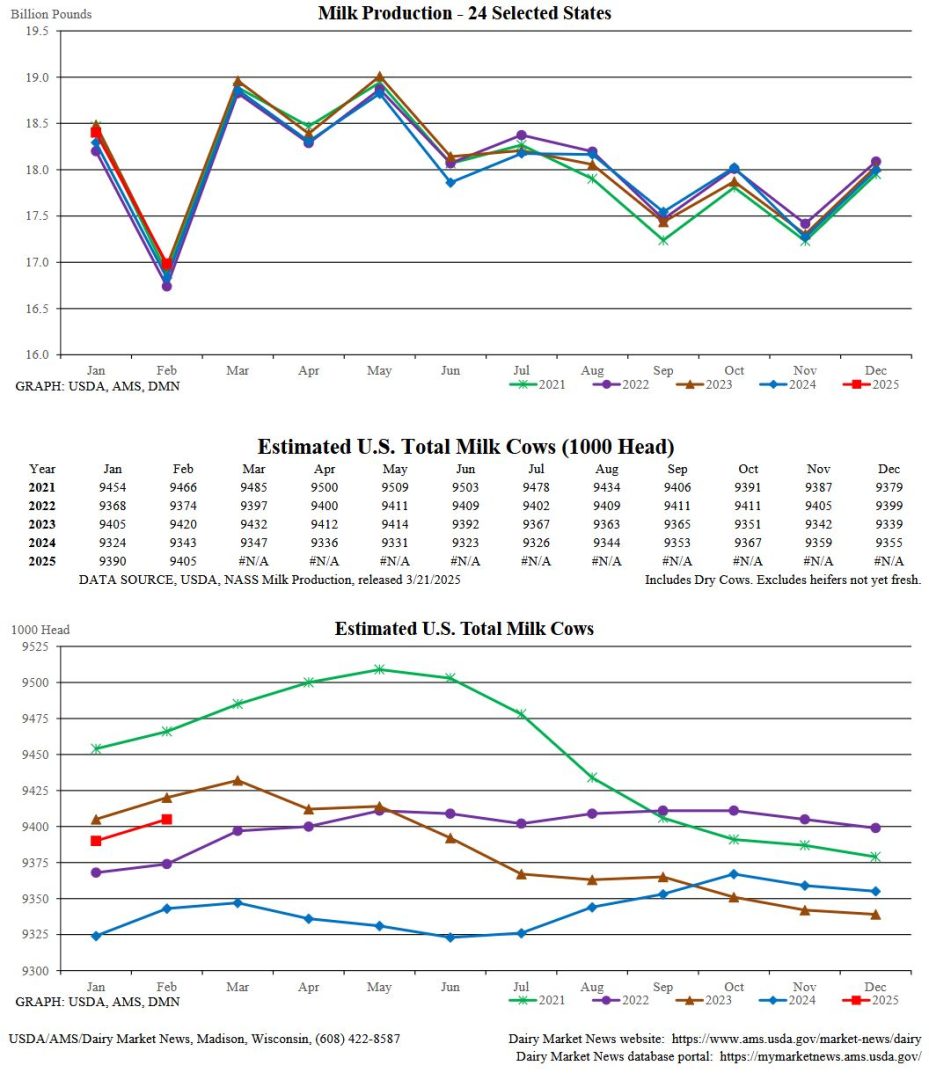

It has been a hard week for everything as the Trump administration unveils the plan for tariffs. With higher than expected tariffs the markets dove lower. Dairy is no exception as America is a net exporter of dairy and trade barriers will slow exports. Production report was a slight increase over last year and cow numbers adding 15k head. Cold Storage also was higher. This is pretty normal this time of year as spring flush starts and inventories build in the spring. The bigger question is where demand is going to be this year.

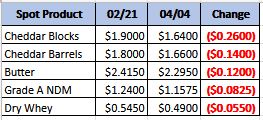

Monthly Spot Prices Comparison

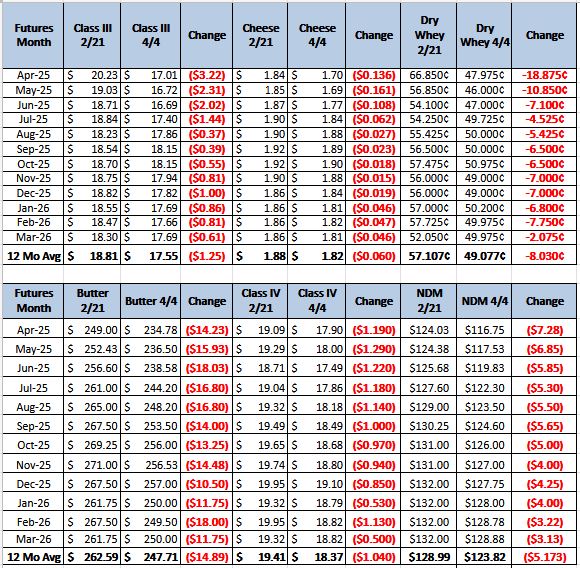

Monthly Future Prices Comparison

Cheese: Cheese plant managers in the East region share active cheese manufacturing schedules. Seasonally strong milk availability has enabled cheese inventories to grow. Some contacts note retail cheese demand remains steady while foodservice demand remains light. Cheesemakers in the Central region relay strong milk availability with spot milk prices falling between $4.50 to $2 under Class III. Ample milk availability has allowed cheese stocks to grow. Contacts in the region relay mixed demand. In the West region, both seasonal milk production and cheese production schedules remain strong. Contacts note block cheese inventories are growing faster than barrel cheese inventories. Retail demand continues to trend steady to stronger while foodservice demand is weak. (USDA Cheese Highlights)

Butter: Domestic retail butter demand continues to vary from steady to stronger. Domestic food service demand is weaker than domestic retail demand. Competitive domestic prices compared to international prices are helping to keep export demand in-line with last week. Cream loads generally continue to be readily available. However, a few butter producers convey cream loads too inexpensive to pass up are no longer around. Many butter manufacturers have their churns running at or near full capacities. Bulk butter overages range from 5 cents

below to 6 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Dry whey prices moved 1 cent lower for all facets of the range. Both ends of the mostly price series have had consecutive downward price ticks going back to week 8. Demand from domestic and international buyers is lighter. Some stakeholders convey unsettled trade factors continue to create some hesitancy from international buyers looking to secure dry whey for animal feed purposes. Spot load availability varies by manufacturer, type of dry whey, and grade of dry whey. A few manufacturers note stocks of anything but Extra Grade white dry whey to be extremely tight. Dry whey production schedules are steady. (USDA Dry Whey)

Milk Production and cow numbers are following standard trends for this time of the year. Demand is going to be the big question. With more federal money being cut for food programs and schools and international trade taking a big hit. Demand, both domestically and exports, is starting to look weaker this year. International prices are much higher than domestic prices which in the past would lead to greater exports. At this time, I do not see exports picking up. Recommendation would be to sell or buy puts. With that said keep an eye on trade agreements and policies because they can change quickly with this administration.