8/25/2024

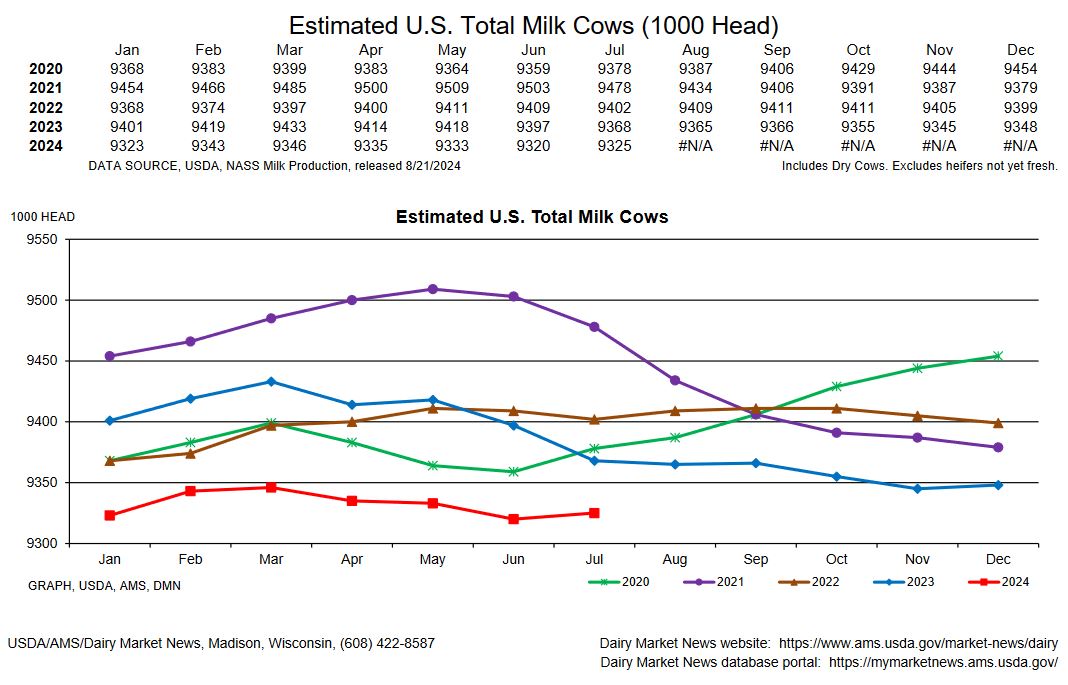

The summer is drawing to a close with cheese prices higher then they have been for a few years. Schools are back in session drawing more milk toward class 1. Cold storage dropped again in July but milk production had a surprisingly strong rebound. This week buyers stepped to the side lines as a few more loads came to the spot market and drop the price at the end of the week.

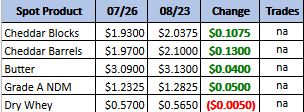

Weekly Spot Prices

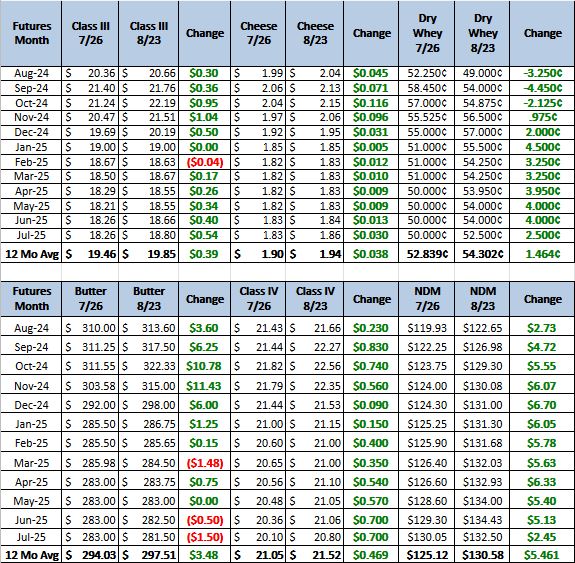

Weekly Future Prices

Cheese: Cheese production is trending seasonally steady to lighter throughout the U.S. Milk availability remains tight in the East. Milk available for Class III processors is constrained by Class I pulls for schools, and cheese production remains light in the region. Contacts anticipate more spot milk availability after Labor Day. Retail demand is steady. Cheesemakers in the Central region relay steady cheese demand. Contacts share demand for barrels remains strong, but spot load availability is rare. Spot milk availability, too, is limited and settled at $2.25 to $3-over Class III. Cheese production is mixed in the West. Some processors relay increased manufacturing while others note tight spot milk availability is slowing manufacturing. Contacts note cheese inventories vary throughout the region. (USDA Cheese Highlights)

Butter: In the West, domestic butter demand varies from steady to stronger. For the Central region, domestic butter demand is strengthening. In the East, domestic butter demand is unchanged. Cream volumes are tight in the East and Central regions. Although cream supplies in the West are looser and more balanced comparatively, stakeholders in the region don’t describe cream volumes as excessive either. Butter production paces vary from steady to weaker. Many manufacturers are relying on contracted cream loads to keep churns moving. Some butter makers convey unsalted butter stocks available for spot buyers are tight. Bulk butter overages range from minus 7 to 10 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Dry whey prices ticked higher on the bottom ends of both the range and mostly price series. The top ends of both the range and mostly price series were unchanged. Dry whey availability remains on the tight end, especially for brand specific spot buyers. For some manufacturers, certain grade specific dry whey stocks are only sufficiently fulfilling contracted obligations currently. Dry whey production schedules are mixed. Some processors are selling the solids as liquid whey. Continued strength with whey protein concentrates and isolate markets continues incentivizing processors away from allocating whey solids to sweet whey production. Demand varies from steady to slightly stronger. (USDA Dry Whey)

With the drop in class 3 futures I would suggest buying puts up front and not limiting the top. The cow numbers have dwindle for the last year to the point that production will most likely not overwhelm demand. This is not to say the market will stay in this $22 range. Demand is going to be the key going forward for the next year. Right now exports are not very strong, so domestic demand is key to holding these prices. Cold storage in July was down 1 percent from June and 6 percent from last year. This is bullish and I will expect the buyers to return this next week.