1/22/2023

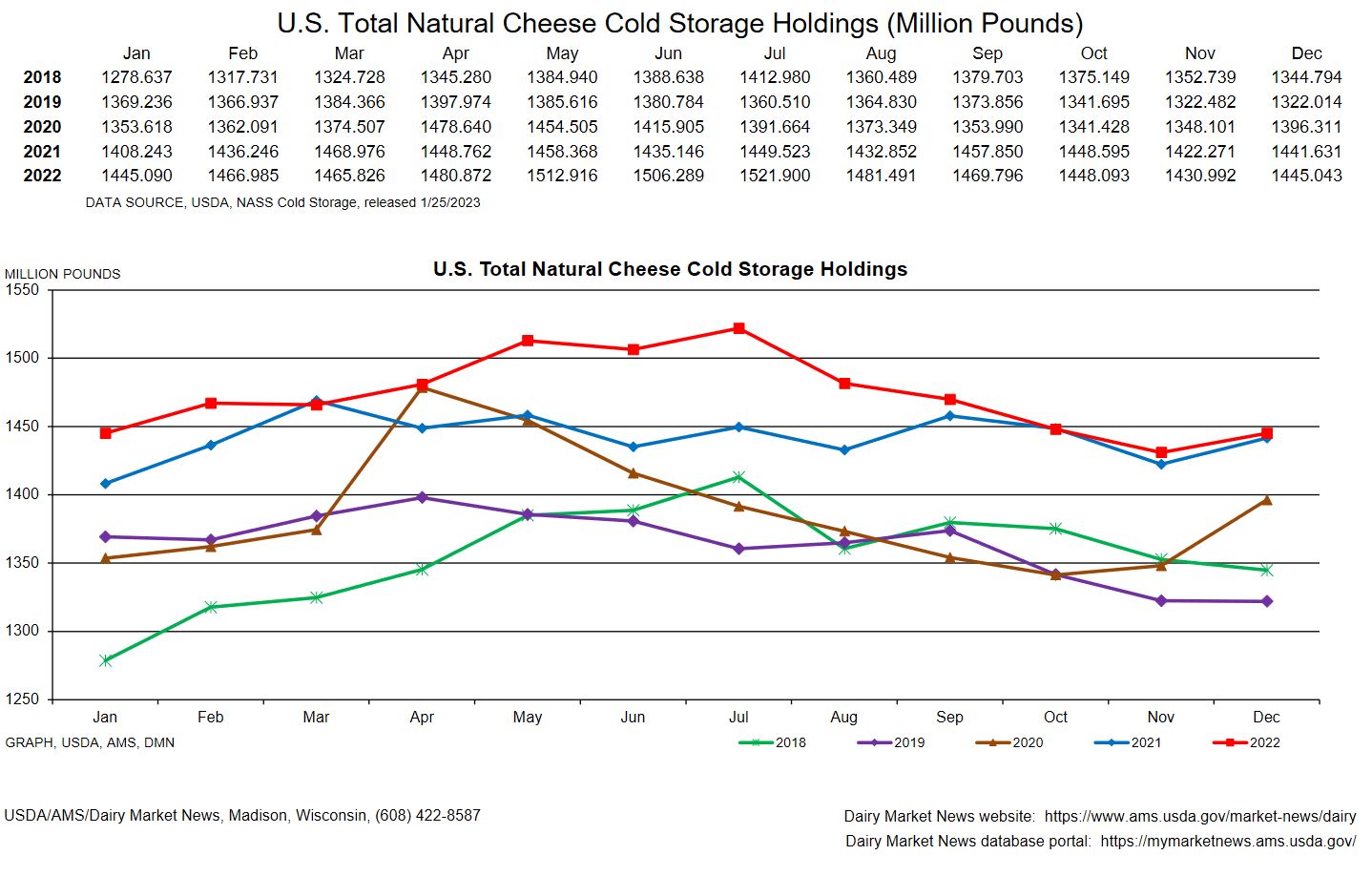

The class 3 market is leveling off from the last couple of weeks drop. Both Milk Production and Cold Storage were out this week, and both reports came out neutral to supportive. Milk Production was up over last year, but milk production drop into the end of last year as cow numbers came off. Cold storage was higher then November 2022 but it was about the same as December of 2021. The market headed higher and posted an all time high for the first six months of 2022, so I do not read the Cold Storage report to be bearish. This does not mean the lows are in. Demand is not what it was in the beginning of 2022, but with cow numbers already starting to drop this year the market lows may come sooner than later.

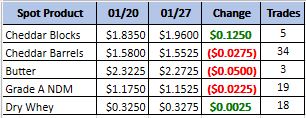

Weekly Spot Prices

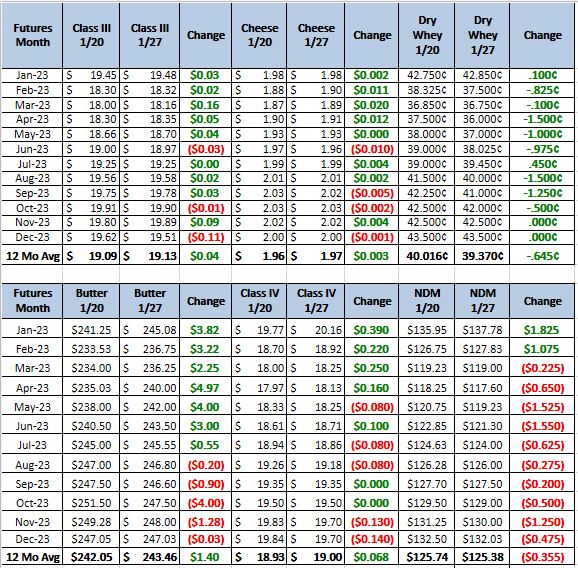

Weekly Future Prices

Cheese: In the Northeast and West, milk is available for strong cheese production. Labor shortages are preventing some plant managers from operating full production schedules in the West. Milk volumes are available in the Central region, but stakeholders say heavy discounts to Class prices are not being as regularly offered as in prior weeks. In the Northeast and West, retail cheese demand is steady while food service sales are strengthening. Some stakeholders in these regions attribute this increased demand to pizza makers who are utilizing mozzarella cheese as sales have increased during the football playoffs. In the Midwest, there is a dichotomy of demand between blocks and barrels, and some barrel producers say bearish market pressures are preventing some purchasers from adding to their stocks. Midwest food service cheese sales have, reportedly, slowed. Export sales of cheese are strong in the West, and some contacts say purchasers in Asian markets are paying above current future prices for loads to ship in Q2 of this year. In the West, cheese barrels and blocks are available for purchasing though stakeholders say barrel inventories are larger than blocks. (USDA Cheese Highlights)

Butter: Cream is readily available in the East and West, while plant managers in the Central region report some variability with availability. In the Midwest, stakeholders say multiples are firming, while those nearer the West region say cream is abundant. Cream handlers say multiples are shifting higher in the East and Central region. Demand for cream is steady to higher in the West, as some processors say they are purchasing more cream to run full production schedules and build salted and unsalted butter inventories. Butter production is strong in the West. In the East and Central region, butter makers say production is focused on meeting upcoming spring demand. Spot demand for butter is steady in the West, though contract sales past Q1 of this year are, reportedly, sluggish. In the East, food service demand is said to be steady, while retail demand is steady to increasing. Contacts in the Central region report softer demand for butter: retail sales are steady, but food service demand is noted as subdued this year. Unsalted butter inventories are tighter than salted in the West. Most of the butter being produced in the East is being frozen or is going to contract purchasers, making butter less available on the spot market in the region when compared to other parts of the country. (USDA Butter Highlights)

Dry whey: Domestic sales of dry whey are steady, though some contacts report lighter sales than previously forecasted for this time of year. International demand for dry whey is steady to lighter, as some contacts report reduced exports to some Asian countries. Dry whey production is trending higher, as cheese makers continue to operate strong production schedules. Some plant schedules are being shifted from higher whey protein concentrates and permeate, due to declining prices, towards dry whey production. Limited demand and strong production are contributing to increased dry whey spot availability and building inventories. Dry whey prices are sliding lower at the bottom of the range and most price series. The top of the price range inched higher, and stakeholders attribute these higher prices to variable contract loads tied to certain indexes. (USDA Dry Whey updates)

Prices have slid below most producers cost of production and are going to bite into equity quickly. Therefore, I do not suggest selling unless you add a call spread. Demand is weaker then last year so lower price still may be coming. Recommendation,buy puts. Ether DRP, put spreads or just disaster relief style puts for 20 cent a month. Looking to the second half of 2023. Buy $19 put, sell the $17.50 put, for a total cost of 40 cents.