2/04/2023

First month of 2023 is behind us and the big news this week is the Jobs report. With all the fear and dread of 2023 being a year when we go into a recession the jobs report is pointing in the other direction. We are at a 53 year low for unemployment. For dairy markets that means continued strong demand. Look for buyers to start loading up on barrels as the risk of missing out on lower prices is less then the risk of prices moving higher in the fall.

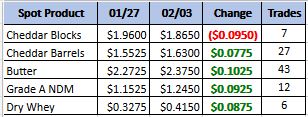

Weekly Spot Prices

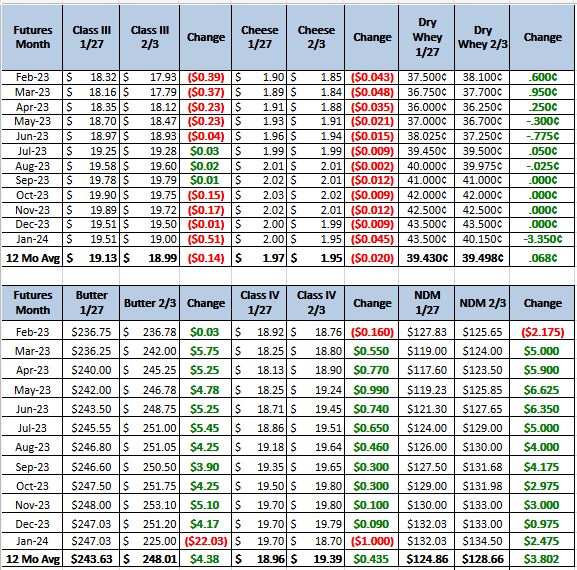

Weekly Future Prices

Cheese: Milk is available for strong cheese production throughout the country, though some plant managers in the Northeast and West relay labor shortages and delayed deliveries of production supplies are limiting some plant managers’ abilities to operate full schedules. Cheese production is busy in the Midwest, and spot loads of milk continue to move at as much as $10 under Class III. Some stakeholders have reported downtime at cheese plants in the upper Midwest this week, for various reasons. Demand for cheese is steady in the Northeast, but sales of mozzarella cheese to pizza makers are softening. In the West, retail demand is steady while food service and export sales are softening. Some stakeholders say lower prices being offered by cheese sellers in Europe are having a negative impact on export demand. Demand for cheese varies in the Midwest. Some cheesemakers relay strong orders, while barrel makers are concerned with growing inventories amid slowing spot sales and lighter contractual buying compared to previous years. Spot loads of cheese are available for purchasing in the Northeast and West. Contacts in the West say barrel inventories are larger than blocks. (USDA Cheese Highlights)

Butter: Cream is widely available throughout the country, and contacts in the West relay strong demand for cream volumes. Some handlers in the Central region report having some difficulty routing cream haulers in recent weeks. In the East and West, butter makers are running strong production schedules. Some stakeholders in the East say they are churning seven days a week, and most of the butter being produced is being frozen or made to fill contracted retail orders. Butter producers are running busy schedules in the Central region, though contacts report production trends are mixed from churning to micro-fixing, depending on specific customer needs. In the East, retail demand is down compared to this time last year, and food service sales are steady. Spot demand for butter is steady in the East. Central region contacts say food service demand is lacking, and some suggest this may be contributing to some bearishness to butter markets. Spot availability of butter varies throughout the East, as some processors are freezing bulk butter. In the West variance has been reported between unsalted butter, with tight inventories, and salted butter, with more available inventories. Butter inventories have been growing since late 2022, in the Central region. Bulk butter overages range from 0 to 12 cents above the market, across all regions. (USDA Butter Highlights)

Dry whey: Sales are steady to domestic purchasers, though contacts continue to report softer demand from export purchasers. Some stakeholders say sales to Asian countries remain below previously forecasted levels. Cheesemakers are running busy production schedules, as strong milk availability persists. Drying operations are utilizing available liquid whey to run strong production schedules. Some plant managers relay lower prices for higher protein whey and permeate are causing them to shift their production schedules towards dry whey. Dry whey production and inventories are running higher. Stakeholders say the aforementioned factors are contributing to lower prices for dry whey. Dry whey prices shifted lower across the range and mostly price series this week. (USDA Dry Whey updates)

Both cheese and dry whey prices having been dropping the last couple of weeks as ample milk suplies flow into cheese plants. This is forcing class 3 prices lower and the market has been leaning negative. However, with cow numbers coming down and the economy still chugging along; I am looking for this market to bottom in the near future. With that in mind the recommendation this week is for buying calls in the 3rd and 4th quarter of this year. Looking at buying $21 calls for an average of 40 cent in the second half of 2023.