4/29/2022

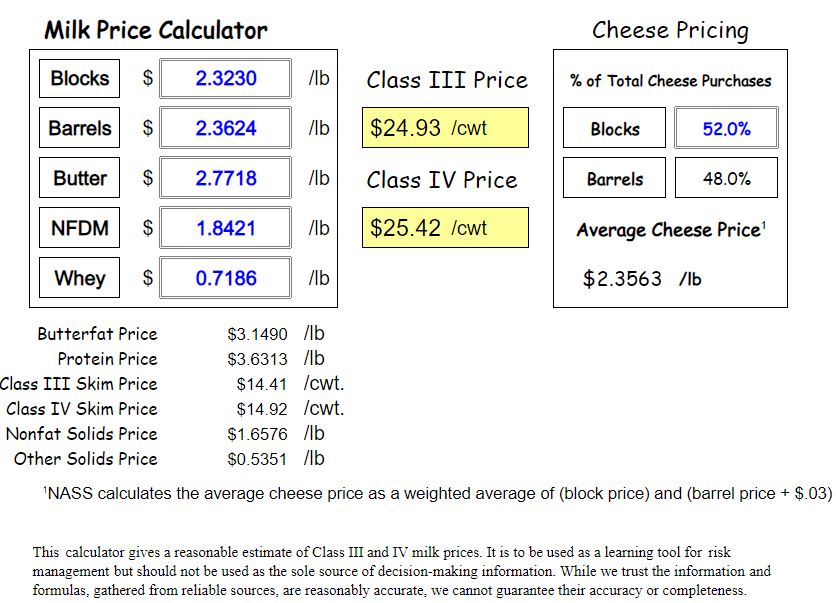

The roller coaster continues. Last week the class 3 market was pushing $25 only to sell back off to the low $24, and then buy mid week class 3 is heading back up. With plenty of milk flowing into cheese plants and good demand in the domestic and export markets look for prices to hold in this range.

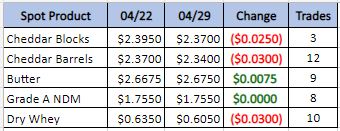

Weekly Spot Prices

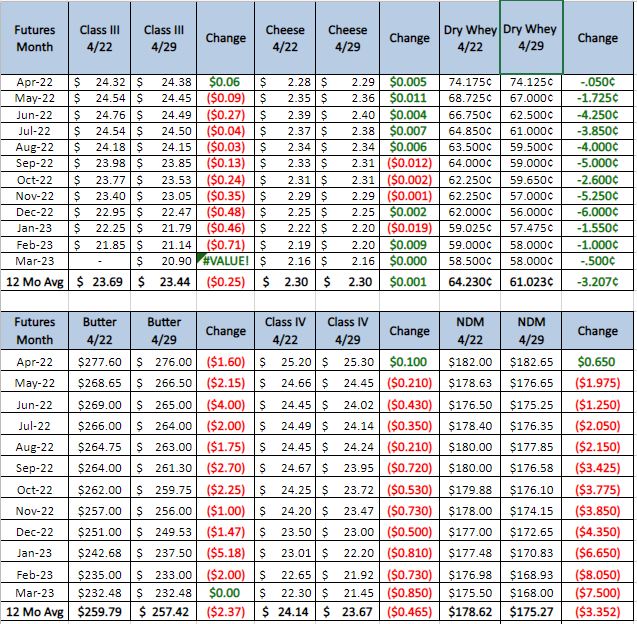

Weekly Future Prices

Cheese: united States milk supplies are growing, thus becoming more available and moving into cheese production. Spot milk prices in the upper Midwest ranged from $2.50 to $1.50 under Class III this week. Comparing this year’s prices to last year’s, spot milk topped out at level last year during week 17, while the low end was $5.00 under Class. Lighter COVID restrictions and spring weather have increased food service demand, according to contacts in the West. Midwestern cheesemakers continue to relay steady to strong demand notes, as well. Eastern cheese stocks are aplenty, but steady demand has allayed much consternation regarding oversupply. Despite some ups and downs on the CME, general market tones are healthy. (USDA Cheese Highlights)

Butter: Cream availability ranges from steady to available for butter processors nationwide. That said, Eastern butter plant contacts relay a snugness on the cream market following the past few weeks. Western cream continues to move eastbound, as some Midwestern butter plant managers report clearing cream from both local and Western sources. There are growing and vocal concerns regarding the domestic butter inventory come late summer/fall, as domestic demand is expected to seasonally intensify, while export interests continue to keep churners churning. Butter market tones remain on solid ground, despite moving into the low $2.60s on the CME from the previous range in the $2.70s over the past few weeks. (USDA Butter Highlights)

Dry whey prices continue to hold somewhat firm in the low-$.60s for a majority of spot trading, while the range is holding onto some higher prices based on brand preference. Still, there were some downticks on the top of the range and mostly series. Production has steadied in recent months, but it remains well behind levels seen in early 2020. Seasonally, milk is increasing at the farm level, but Class III production is facing the workforce challenges that much of the industry is. Plant managers have become seasoned in maneuvering through these choppy waters, as this will be the third consecutive flush season in which they have dealt with circumstances outside of their control limiting employment rosters. Whey offers have increased with the incremental increases in production recently. Animal feed whey trading was steady week to week, as prices dropped on the bottom of the range. Whey market tones lack certainty moving into May. Market looks steady to softer. (USDA Dry Whey updates)

NDPSR Calculated Prices

NDPSR prices have held up in recent weeks as cash prices have started to falter. Cash is usually a good indication on where the NDPSR will go next. For those of you who do not know NDPSR is the National Dairy Products Sales Report, which is what Class 3 and Class 4 ending prices are based on. Cash is the daily trade of physical dairy products on the CME. If the prices on the NDPSR do not start to drop on the next report (which it comes out every Wednesday) futures could put in some new highs next week. This would be a good time to layer in some hedges. I would still suggest doing some DRP, or look buy a put at the money and sell a call $2 higher for 30 to 40 cents.