4/8/2022

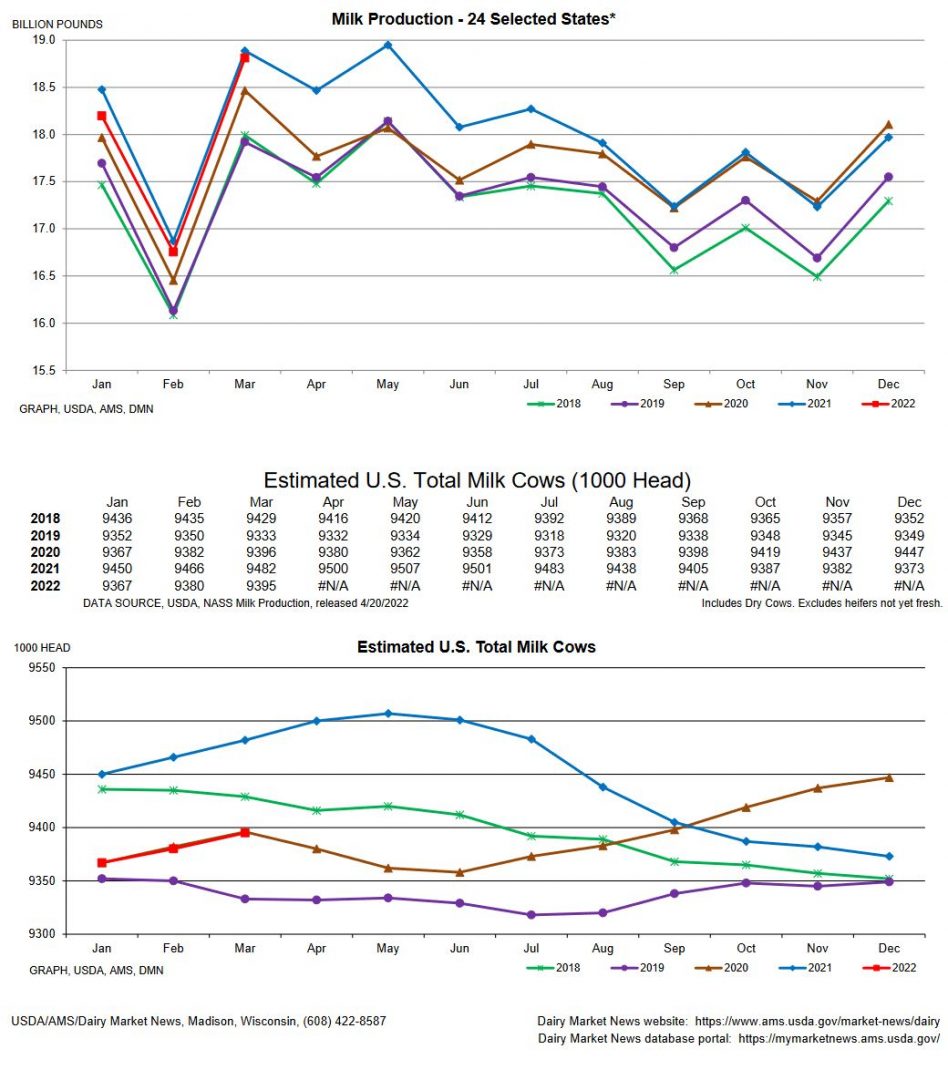

As class 3 knocks on the door of $25 we have started to see some resistance. Class 3 popped over $25 early this week to them sell back off below $24. Prices are still strong and demand is holding but at these prices milk production is starting to move higher. Grain prices and just the ability to get feed has kept milk production down, but as we start to see these higher milk checks show up in producers mail boxes production is likely going to move higher.

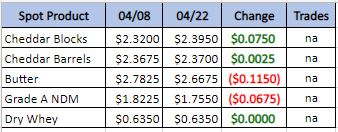

Weekly Spot Prices

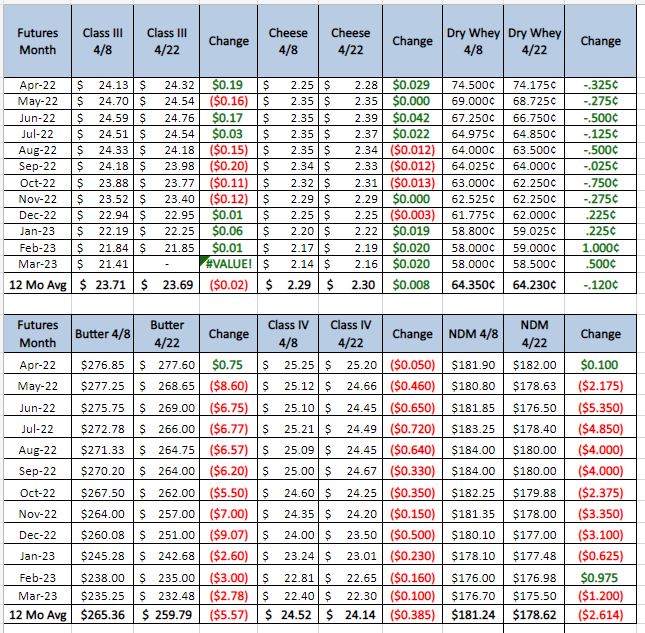

Weekly Future Prices

Cheese inventories are available for spot purchasing in the Northeast and West, though some Midwest stakeholders report that they are slimming some orders to fulfill others. Across the country demand for cheese is strong in retail markets. Stakeholders in the Northeast and West say that food service demand is increasing and international demand is strong. Contacts, in the West, report that port congestion is preventing them from increasing the volume of cheese loads that they are sending to international markets. Wintery weather in parts of the Northeast have caused some load deliveries to face delays. Cheesemakers are running active schedules across the country, though plant managers cite staffing shortages as hindering their ability to increase production schedules. Prices for both barrels and blocks have dipped on the CME this week, though some bullish market participants seem undeterred due to strong demand. (USDA Cheese Highlights)

Butter: cream inventories are mixed throughout the country. Contacts in the Northeast and West report that strong ice cream production is pulling on regional cream supplies. Demand for butter is steady in retail markets, while retail sales are, reportedly, slowing in the Northeast and West. Stakeholders say that rising grocery store butter prices may be contributing to decreased consumer demand. Inventories vary across the country Some Western butter makers say that they are selling spot loads to purchasers in other regions where inventories are tighter. Contacts report that staffing shortages remain present in the Central and West region, though production is steady. Meanwhile, butter production varies throughout the Northeast. Bulk butter overages range from 5 to 15 cents above market, across all regions. (USDA Butter Highlights)

Dry whey: International inquiries for dry whey are trending higher. Contacts report that some export purchasers are looking to purchase loads as dry whey produced domestically is being sold at a discount to loads produced in international markets. Domestic demand for dry whey is steady. Spot purchasers say that dry whey inventories are plentiful. The price range for dry whey saw mixed movement this week. Mostly price series was unchanged at the bottom, while the top moved higher. Contacts report that port congestion and a shortage of available truck drivers continue to cause delays to load deliveries. Plenty of liquid whey is available for drying operations as cheesemakers are running busy schedules, in the region. Dry whey production is unchanged. Plant managers say that they continue to focus their schedules on higher whey protein concentrates and permeate. (USDA Dry Whey updates)

Milk production was still below last year but is still pushing multi year highs. Good domestic and international dairy demand has held prices at current levels. Cow numbers are starting to grow as prices in class 3 and class 4 provide good margins even with the elevated input costs. I expect this trend to continue. There will need to be continued strong demand in both domestic and international markets to sustain these prices. Recommendation this week: buy some DRP, or buying 30 to 50 cent puts, then enter some orders to sell puts $2 lower for the same price. It will take a drop in the market. to get it done, but you will end up with a put spread for a much cheaper price. These high prices look like they are going to stick around for now, but the market moves fast and it could easily drop $4 to $5 on some easing in demand.