3/25/2022

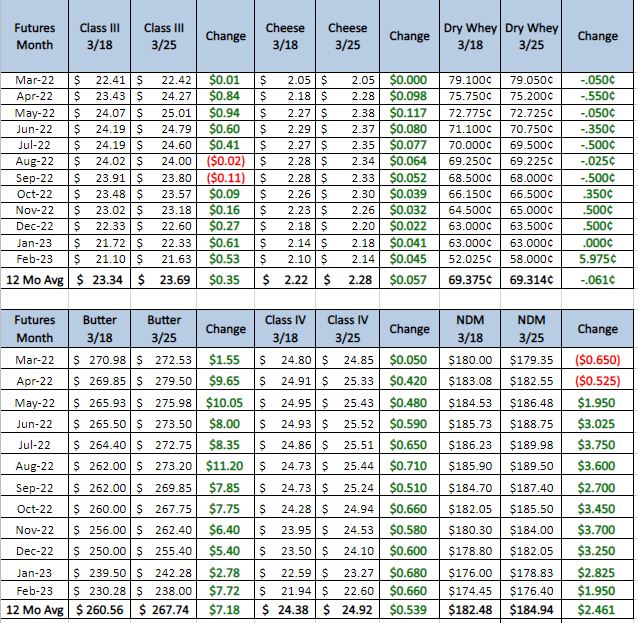

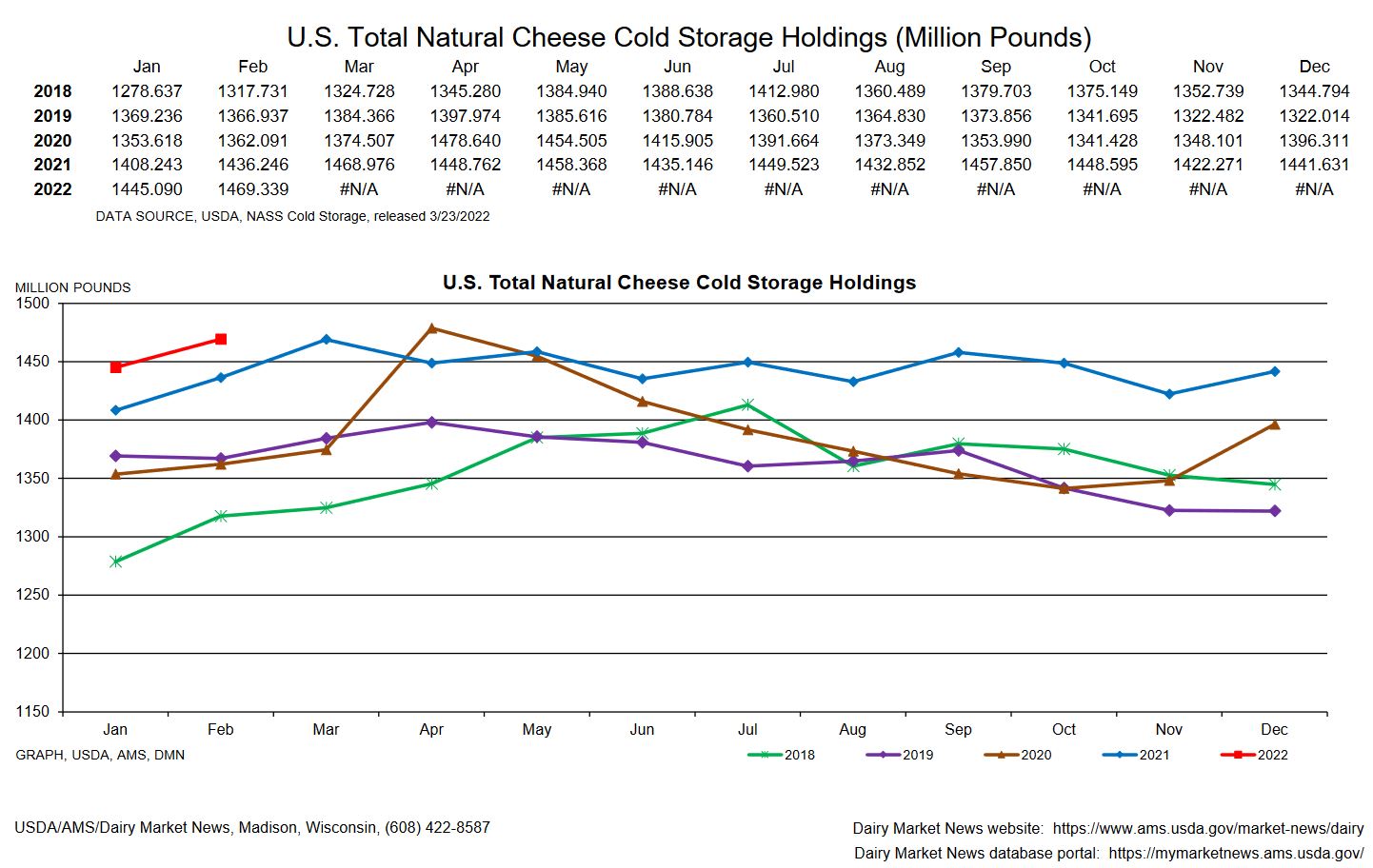

Class 3 futures push above $25 as cash cheese pushes to new highs on the year. As the market tries to gauge what the world supply and demand will look like the the next year the demand side has been the driver. The mind set in the current market is make sure you have it just in case you can not get it later. Kind of like in the beginning of 2020 when there was a run on toilet paper. With Cold storage for cheese moving up 2 percent from last month and up 2 percent from last year there should be enough cheese to meet needs, unless the worlds production capabilities dramatically change.

Weekly Spot Prices

Weekly Future Prices

Cheese demand is noted as hearty in all regions. Until recent weeks, hesitant customers were awaiting potential downward pressure on prices. Now, they are actively seeking out cheese to refill pipelines, and get ahead of bullish price movements. Western suppliers are busily filling orders for Asian buyers, as domestic cheese prices remain a bargain to global values. Labor and hauling remain problematic, although cheesemakers who can run full (or near-full) schedules are busy. Milk remains available for Class III use, as prices are discounted for spot milk in the Midwest from $2 to $1.50 under Class. Last year’s spot milk price range was $5 to $3 under Class III and 2020 prices reached as low as $6 under Class during week 12. (USDA Cheese Highlights)

Dry Whey: International demand for dry whey has continued to soften, as U.S. produced loads are being sold at a premium to loads coming from other countries. Contacts report that this decline in demand is contributing to an increase in spot availability. Domestic demand for dry whey is steady. The price range for dry whey was unchanged at the bottom, while the top moved lower. Stakeholders say that prices near the top of the range are primarily tied to certain indexes. Both ends of the price series shifted lower by 2 cents. Loads of dry whey continue to face delays due to port congestion and a shortage of available truck drivers. Dry whey production is steady, though plant managers report that labor shortages are causing them to run below capacity. (USDA Dry Whey updates)

We are hearing about commodity buy from Asian markets is very strong. This is across all commodities with very little concern to the price. This has helped support prices as they have pushed higher. This may be do to the fact that China’s winter wheat crop could be the “worst in history” according to China’s Minister of Agriculture. Although, with that said, China’s grain output rose 2 percent in 2021 according to the National Bureau of Statistics. At the end of the day, we are having good demand for both feed and Dairy which makes it difficult to lock in even these high prices because input costs keep climbing higher. Recommendation this week is buy some puts. $20 class 3 puts can be bought for around 30 cent this year. This is far below the market but if the world finds out it has enough “toilet paper” all these commodity prices could come down dramatically.