4/8/2022

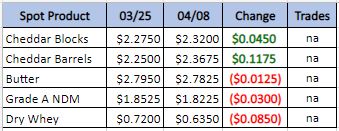

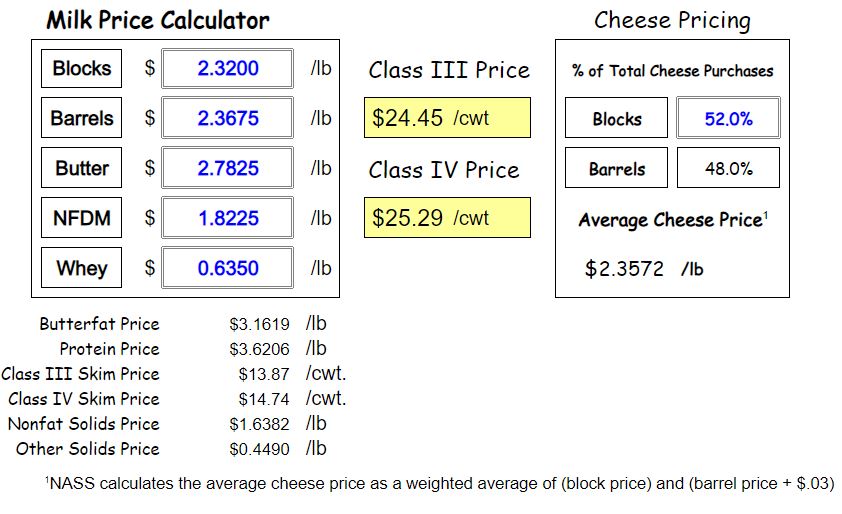

Class 3 futures push back toward $25 again and this time cash is leading the way. With new highs in cash; blocks at $2.32 and barrels at 2.3675 class 3 prices out at $24.45.

Weekly Spot Prices

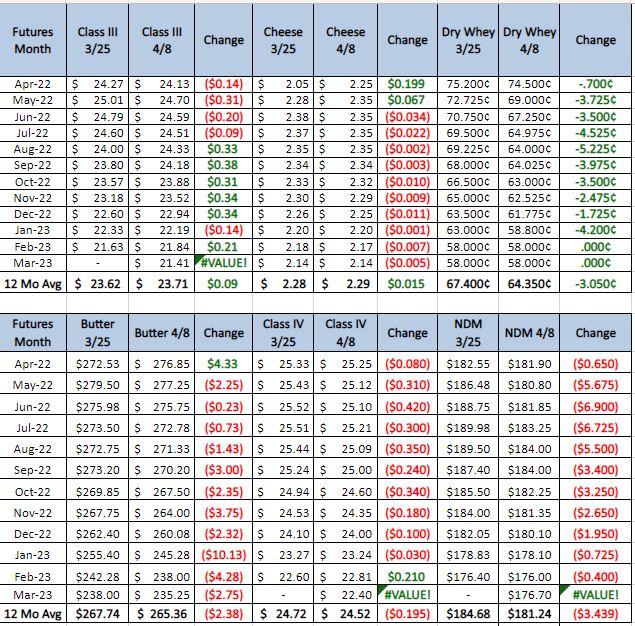

Weekly Future Prices

Cheese demand is steady throughout the country. Contacts report that export demand for cheese is strong, as loads produced domestically are priced favorably compared to cheese produced internationally. Port congestion is causing delays to some export loads departing from the West coast. Purchasers in Asia are looking to lock in loads for shipment in early 2023. Spot cheese inventories are available throughout all regions. Milk is available for cheesemakers to run busy schedules. Labor shortages are impacting cheese production in all regions, but producers in the Northeast and West are reporting strong output. Some Midwestern cheese plants have reported that labor shortages are contributing to some unplanned down time, but other nearby cheese plants are processing loads of milk intended for these plants. (USDA Cheese Highlights)

Butter: Cream inventories are mixed, with contacts in the Northeast reporting tighter cream availability. Butter makers in the Central region are sourcing supplies of cream locally and from the West. Domestic demand for butter is steady to higher across the country. Contacts report that internationally produced loads are being sold at a premium to butter produced domestically. This is contributing to strong export demand, though some sellers in the West say that port congestion is preventing them from moving more butter to international markets. Butter production is mixed; contacts in the Northeast report lighter output, while butter production is steady in the Central and West regions. Across all regions, bulk butter overages range from 5 to 15 cents above market. (USDA Butter Highlights)

Dry whey prices moved lower this week across the mostly price series and the bottom of the range. Contacts report that prices tied to certain indexes have caused the top of the range to move higher. Market prices for dry whey have been trending lower, on the CME. Wednesday’s dry whey CME price was 6 cents lower than a week ago. Contacts report that export demand for dry whey has been low in recent weeks as domestically produced loads of dry whey have been priced at a premium to internationally produced loads. This has caused spot inventories of dry whey to build and has, reportedly, put downward pressure on dry whey prices. Domestic demand for dry whey is mixed. Some spot purchasers are hesitant to buy loads of dry whey due to the recent downward swing in prices, while others are reentering the market amid lower prices. Dry whey load deliveries continue to face delays due to port congestion and a shortage of truck drivers. Dry whey production is unchanged, as plant managers are focusing their time on the production of higher whey protein concentrate and permeate. (USDA Dry Whey updates)

We are starting to see the export market back off on whey. This has caused a 20 cent drop from the highs in the whey price at the start of the week. At that point some domestic demand stepped back in to raise it back up to end the week above 63 cents. I think that whey is the one market signal we could see to lead a correction to class 3. This is a major export for dairy and if we see weakness here it could spell signs of weakness in the export market as a whole. Recommendation this week for class 3 2022, buy the 23.00 put sell the 27.00 call. Pay an average of 35 cents.