3/18/2022

The war in Ukraine is still the main mover in the markets. With the uncertainty of milk and grain production and/or demand in Europe; we have seen a roller coaster of prices based more on head lines in the news, and less on fundamentals in the market. This erratically movement creates opportunities but with out a clear direction and the large swings as of late you need a strong stomach and a large bank account to take advantage.

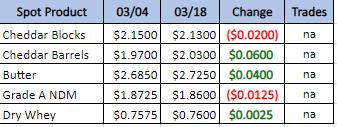

Weekly Spot Prices

Weekly Future Prices

Cheese markets are seeing good demand from domestic and international markets. Both retail and foodservice note improvements, as warmer conditions and loosened COVID restrictions impact consumer demand level. Pulls on milk supplies by cheesemakers are strong throughout the regions, leading to fairly active production schedules. Cheese markets continue to demonstrate strength. Cheddar block and barrel prices have been mixed on the CME this week, but prices for both are currently north of two dollars. Spot availability is steady. Export demand for cheese is strengthening, driven largely by lower prices offered for U.S. produced loads of cheese in comparison to other internationally produced loads. (USDA Cheese Highlights)

Butter: Cream is still available to butter makers for the time being. That availability, however, is starting to tighten as busy seasonal Class II and Class III cream-based production pulls hard at cream supplies. Butter output varies from plant to plant, but many manufacturers are keeping active schedules and ramping up production. Butter inventories are mixed, with reports generally ranging from tight to adequate. Unsalted butter remains trickier to source than salted, though. Food service sales are strengthening as warmer weather and relaxed COVID safety precautions beckon to more restaurant patrons. Retail orders are increasing ahead of spring holidays. Across the country this week, bulk butter overages range from 7 to 16 cents above market. (USDA Butter Highlights)

Dry whey spot inventories are becoming more available, as international demand continues to fall below some industry stakeholders’ expectations. Contacts report that U.S. loads of dry whey are priced at a premium to loads from other countries, reducing demand for export loads. Domestic demand for dry whey is steady. The bottom of the price range for dry whey and both ends of the mostly price series moved lower this week. Prices at the top of the price range increased, though contacts say that these prices are tied to certain indexes. Port congestion and a shortage of available truck drivers are causing delays to load deliveries. Dry whey production is steady, despite reports that labor shortages are causing some drying operations to run below capacity. Plant managers say that they are focusing their schedules on the production of higher whey protein concentrates and permeate. (USDA Dry Whey updates)

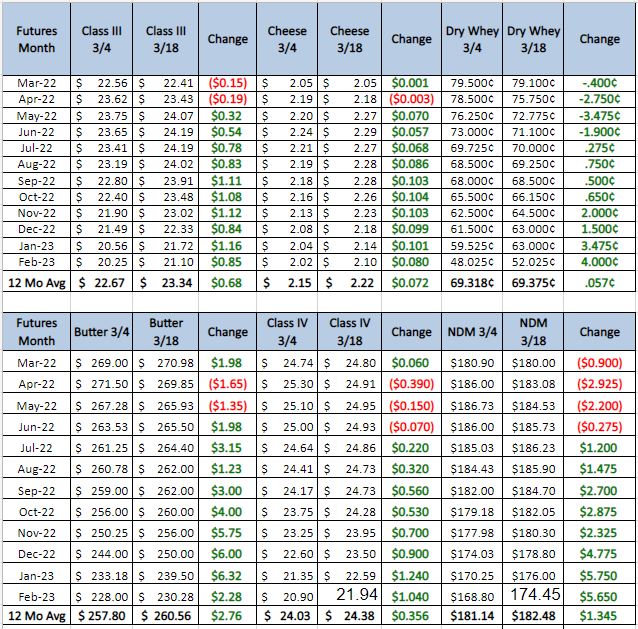

Very few fundamentals has been going into what this market is reacting too. It is more the uncertainty of what milk production will look like with high feed costs. We could see less production coming from the EU because of the disruptions of feed and fuel. This has come together to push most of 2022 above $24. This could be the new reality if Europe can not get the natural gas it needs to run its cheese plants; and the rest of the world turns to the US to meet their cheese demands. On the other hand looking at the current demand prospective. We are starting to see slowing demand on Dry whey. As that demand starts to come off from the international market. The domestic market will be less willing to pay the elevated prices we have seen this last year. The difference in dry whey price from one year ago to now adds $2 to the class 3 price. Therefore you could be looking at $22 class 3 instead of $24 class 3; just because of the whey price. Recommendation: buy 2300 put, sell the 2000 put, and sell the 2700 call for May 22 – Nov 22; look to pay 10 to 20 cents.