3/13/2021

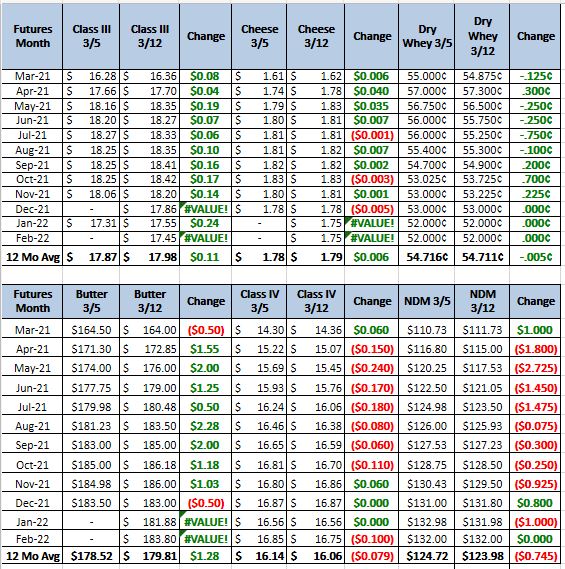

Is COVID over? Texas seems to think so as the state opened up with no restrictions. This has given some lift to the Dairy markets. With signs of going back to normal and increased demand in the food service sector, class 3 put in new highs this week. If there is no surge in Texas COVID cases, other states may soon follow suit leading to higher demand in food service.

Spot Market Recap

Milk Production

In the Northeast, cheese makers are running full production schedules as milk supplies continue with milk to be abundant. Cheese inventories are available for customer needs, as retail orders are stable to strong and food service is slightly improved. In the Midwest, cheese sales are reported as stronger with food service showing some life. Milk is still readily available and cheese production is running full schedules. Even with stronger demand inventories are growing. In the West, retail cheese demand has remained steady and food service demand has a slight uptick. Mozzarella cheese has continued to move well but inventories remain heavy and buyers are receiving multiple offers, especially for cheddar-style cheeses. Milk remains widely available as cheese production is running at or near capacity.

The Butter market is steady after last weeks rally, but inventories are heavy. Demand has increased with both export and domestic demand growing. Also retailers are starting do promotions ahead of the spring holidays. Over all the butter market tone is steady to bullish.

Dry whey prices continue to shift higher with booming demand from Southeast Asia. Domestic buyers are working through their inventories and only buying as needed with the price topping 60 cents and ranging as high at 70 cents. Animal feed whey trading was quiet this week as prices went unchanged. As demand outpaces supply, the dry whey market tone remains bullish.

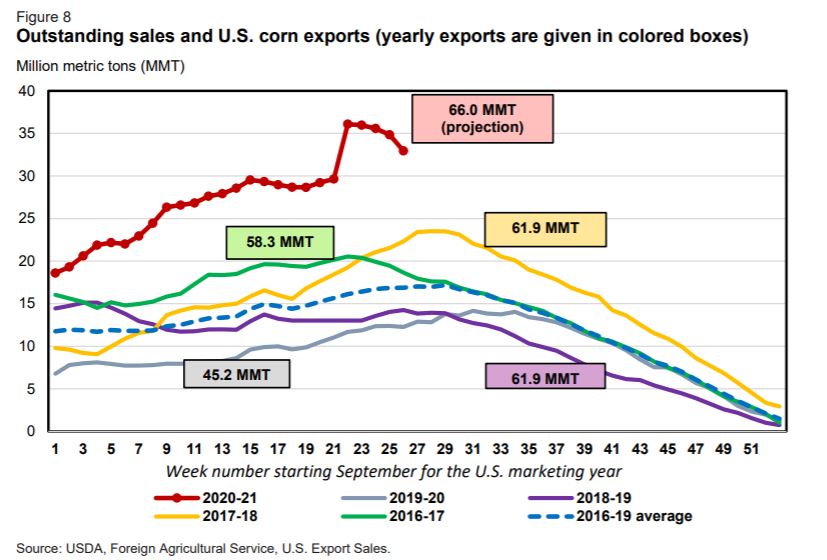

On grains, commodity hedge funds are liquidating their investments and moving money toward the stock market. Also the stocks report this week left corn and soybeans unchanged which the trade was expecting a draw down as China has continued to import substantially more grains then last year, (see graph below). Higher fuel prices have also given some life to the ethanol industry. If these factors remain on their trajectory I expect grains to regain their loses from this week and may push into new highs all the way through May. Recommendation: Wait for a setback in May corn to 5.20 currently at 5.39 and buy futures. Or book additional needs with your feed supplier and buy a 20 cent out of the money May put, or longer term trade Sell the 5.00 September Straddle at 80 cents and buy 6 September 6.00 calls 15 cents each ( for a big move higher in the corn price) cost of this trade is 10 cents .

With grain prices moving higher cost of producing milk is moving up as well. There has been a definite correlation between the milk price and the grains price in the past. That could partly explain why the future prices on class III have moved up so strongly. In the past this has been the case because, as grain prices have moved higher, dairy farmers have cut back on feed and this in turn produced less milk. This has not happened as of yet as milk is widely available throughout the country. Without a cut in milk production we are going to need to see a jump in demand to maintain the future prices. We could see this from government contracts but for now the new administration is reviewing the programs it has used this last year. I would recommend continuing with put spreads on class III. I like buying the 1800 put and sell the 1650 put. These are going to be around 40 cents, if you are comfortable with selling calls you can get that 40 cents back by sell a 2000 call. If we can be of assistance give us a call.