3/20/2021

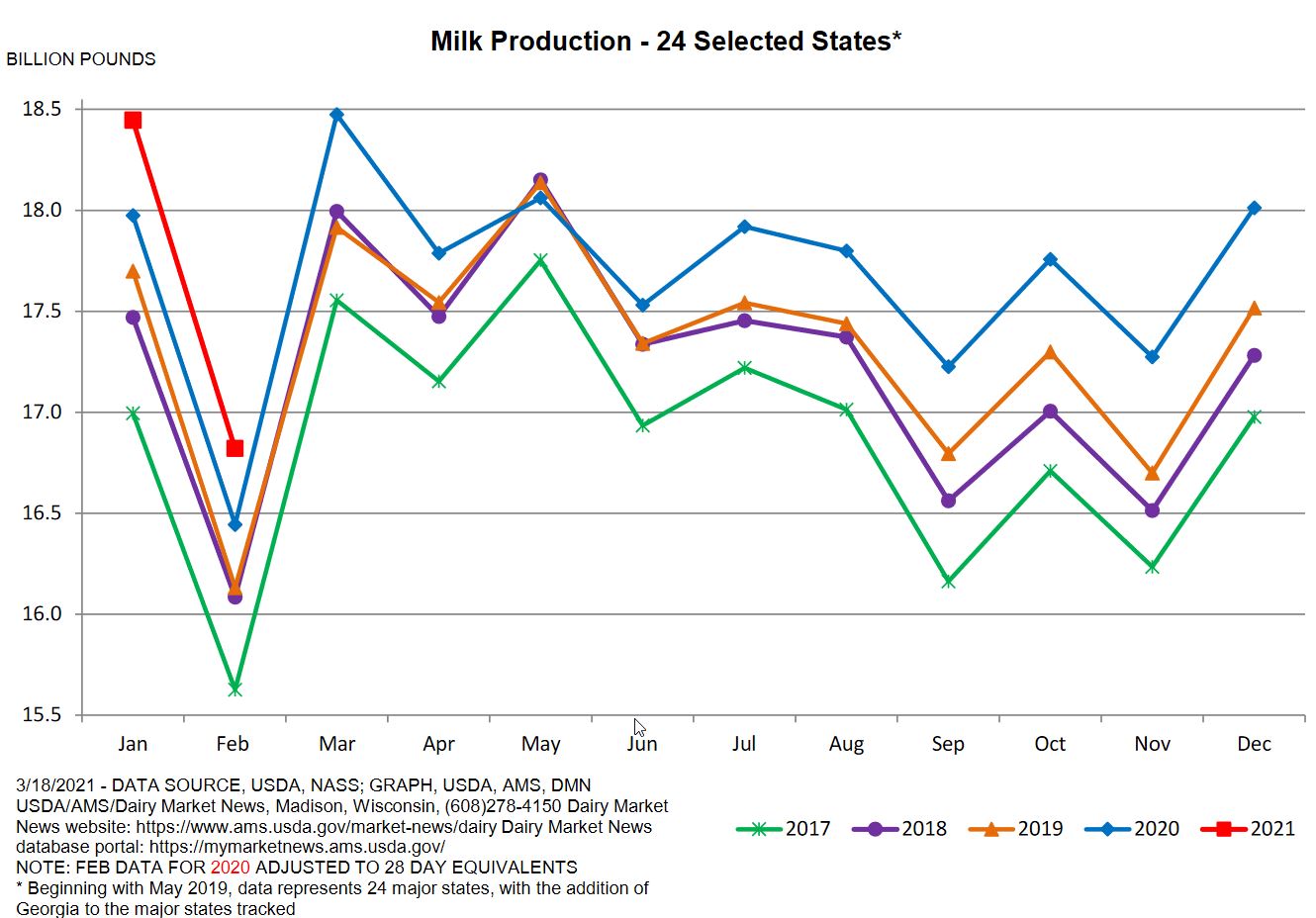

Improving demand, no government intervention, and milk production up 2.3 after adjusting for leap year all are in this weeks report. Are the $18+ futures justified? There were predictions as high as 4% increase in milk production at the start of the year and we may still head in that direction. In February, we had one of the worst storms roll through the middle of the country, forcing farms to dump milk and lose production as temperatures set new record lows. This did not seem to hold up production much as cheese and butter both added to inventories. As the country thawed out, restrictions on restaurants began to lift. This development has given a much needed lift to food service demand.

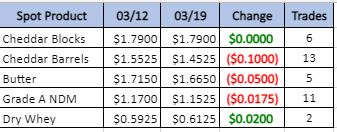

Spot Market Recap

Milk Production

Cheese Northeast’s steady milk supply is flowing into manufacturing and has inventories available for spot and contract demands. Retail demand is sold and food service sales are slightly improved. Restaurants have lifted capacity restrictions, leading to increased demand. In the Midwest, food service has picked up as well as export interests and school lunch programs. This has all led to cheese inventory tightening up, but manufacturers are still able to meet customer needs. With spring holidays right around the corner the market tone is somewhat bullish. In the West, retail demand for cheese is starting to slow. Food service, on the other hand, is picking up. Inventories are more than adequate to meet demand at this point. There is plenty of milk, and cheese markets are running at near capacity. As the price has moved higher, export demand has pulled back. Over all the market is stable for now.

In Butter the West has ample supply of cream with the central and east regions a little tighter. With that said, butter inventories are heavy and fresh butter is plentiful. Retail demand is strong with spring holidays right around the corner and food service is a little improved. Export interest is stable and the over all tone for butter is positive.

Dry whey prices continue their upward movement this week, as prices continued to find their way into the 60 cent range. Domestic and export demand is thriving and feed whey buyers are starting to buy more of the off-spec whey and paying near the 60 cent range. With some sporadic production in 2021 the tone in the market is running bullish.

Planting to start early for Corn & soybeans with the potential for higher yields. The grain market has been giving up some ground this week. Government revenue protection for corn will push more acres that way, and with that it will be difficult to plant record acres of Soybeans. Also Rapid planting progress usually means more corn acres get planted. Currently, soil moisture for the Dakotas and Minnesota is mildly dry , but the NOAA predicts normal rain chances this spring which should narrow the dry areas. I would recommend buying Soybean meal needs thru August working with your local feed supplier and then protecting the cash SBM position with July SBM put spreads. July 390/370 Meal put spread for 6 dollars a ton. (100-ton contracts).

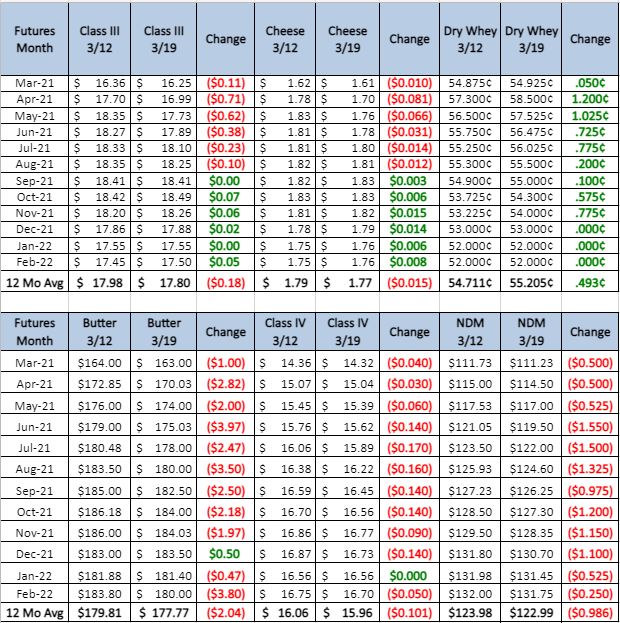

The class 3 market held for most of this week with Friday finally showing some weakness. Cheese demand has been improving and the production report was not as bad as many feared it would be. But inventories are still ample for needs and any increase in price has made a notable pull back in export demand. We still have yet to hear anything from the government on further buying and, should they decide their money is best spent in other ways, the $18 prices on future months will soon disappear. I would look to put spreads and selling rallies to cover the remaining 2021 year and even look to add some in 2022. We have only 2 years in the 20 years that averaged above $18 so traditionally those are pretty good numbers. If we can be of assistance please give us a call.

I will be traveling next weekend so there will be no report next week.