2/27/2021

A light at the end of the tunnel. There is a shift in most states to lifting restrictions and easing public dining restrictions. Texas is the first state to fully open up and do away with restrictions, and with COVID numbers continuing to slow we may see other states start to follow suit. This has picked up food service orders and with retail demand remaining higher then average, spot cheese prices saw a nice bump up this week.

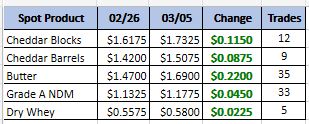

Spot Market Recap

Milk Production

In the Northeast, cheese production is running close to full capacity with ample milk available in the region. Food service sales are steady with restaurants ordering supplies. Retail orders remain good as schools and institutions look to remain open for the rest of the school year. Current cheese prices are steady. In the Midwest, cheese production is active as milk is widely available on the spot market. Current spot prices are $2 to $7 under class. Cheese sales have recently pulled back from the peak, but as restrictions ease, most cheesemakers expect food service orders to pick up. Block availability has grown as buyers are reluctant to take on extra loads. In the West, cheesemakers have plenty of milk to run active production schedules. Inventories are building but demand has been good and much of the cheese is already sold. Due to the rise in the international prices, export interest is strong. However this interest is attached to current cash price. With future prices above cash, sellers are not willing to lock in at current cash prices several months out which has limited export contracts. Overall the cheese market tone is supported at these levels.

In butter cream, supplies are abundant with very active churning schedules. Butter inventories are heavy but food service and retail demand is increasing. With the anticipation of spring holiday demand prices have moved higher. U.S. butter prices are competitive in the international market and exports are increasing. Over all butter is in balance at the present time.

Dry whey prices have continued to move higher as production is not keeping up with demand for both edible and animal feed whey. The current rebuilding of swine herds in Southeast Asia is having a direct effect on the domestic markets and prices. Dry whey is still in the midst of a bullish run,

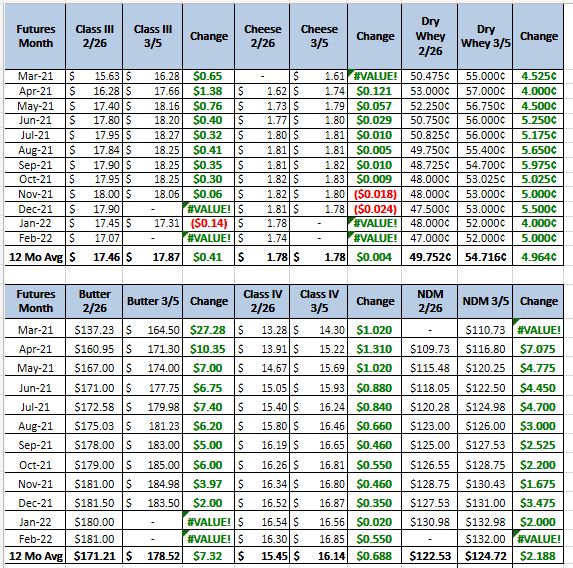

Bellow is the Global Dairy Trade Price chart.

I would say the overall dairy market outlook is improved from last week. This is due to stronger demand in the food service side, and the prices in the international market rising. With that said we still have more than enough milk production to keep manufacturing running full blast and we still have not hit spring flush. With class III future price quite a bit higher then cash our export interest may not hold. I still feel that we will need some government support to maintain the future prices as we get closer to them. With this in mind I would recommend some put spreads. Buy the $18 puts sell the $16.50 puts May 21 – Nov 21 for 40 cents, and if you do not mind limiting the top sell a $20 call.