08/21/2020

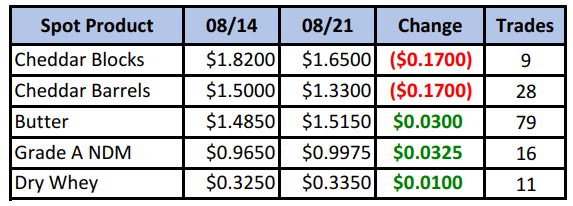

Butter/powder continued to gain on cheese in this week’s spot market as both blocks and barrels failed to gain any traction. Barrels especially felt week, settling at lows not seen since May. Volume was heaviest in butter with a solid 79 loads exchanging hands, with buyers pushing the price 3 cents higher.

Spot Market Recap

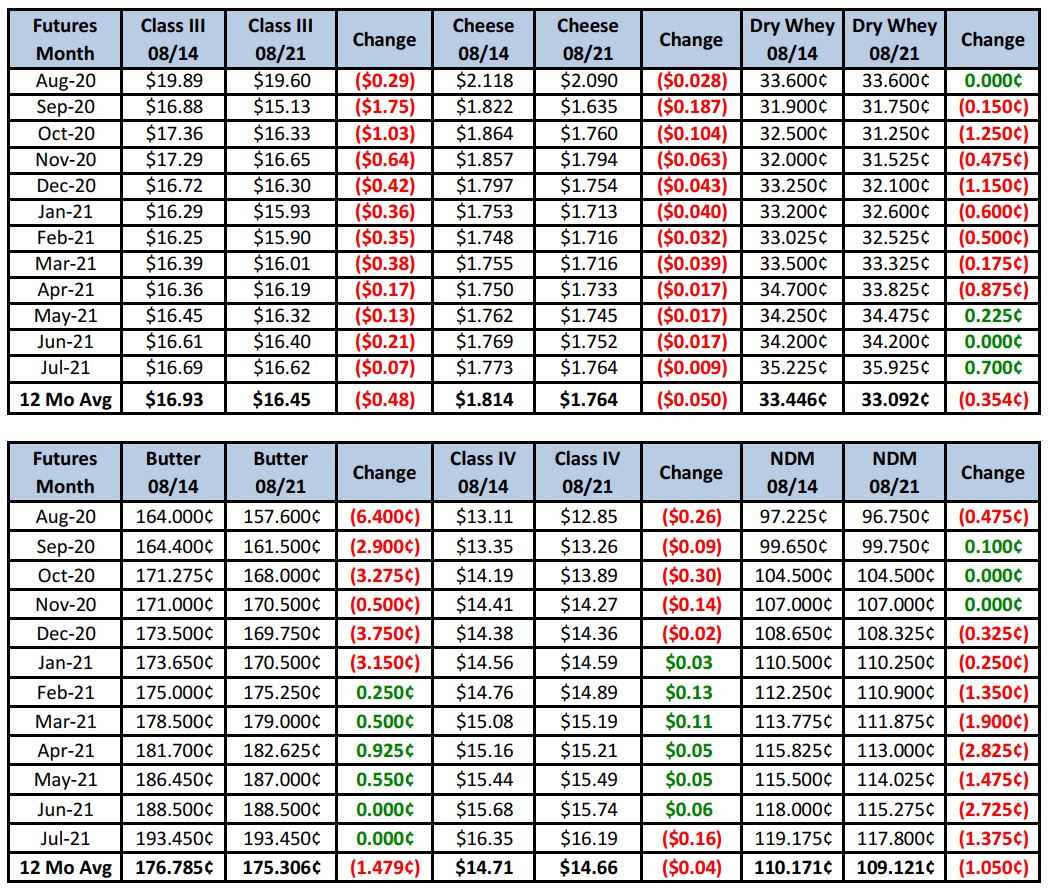

Futures Recap

Quite a lot of data was released this week, none of it very encouraging to the market.

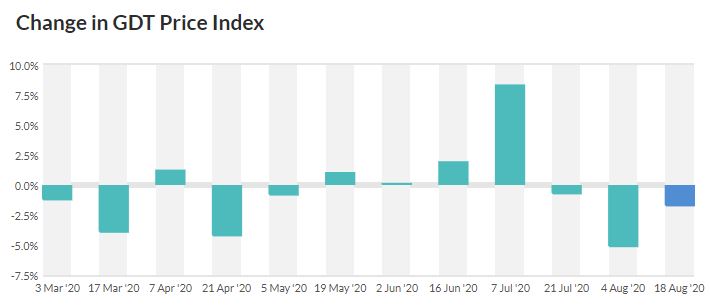

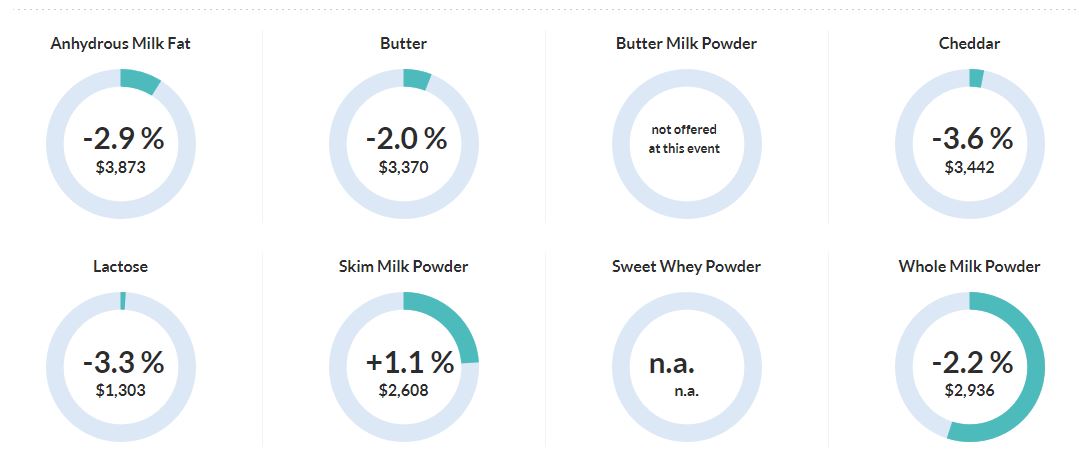

Starting out with this week’s GDT, the Dairy Price Index declined for the third straight event, down 1.7%. Cheddar cheese was the biggest loser, falling 3.6% to a U.S. equivalent $1.56/lb.

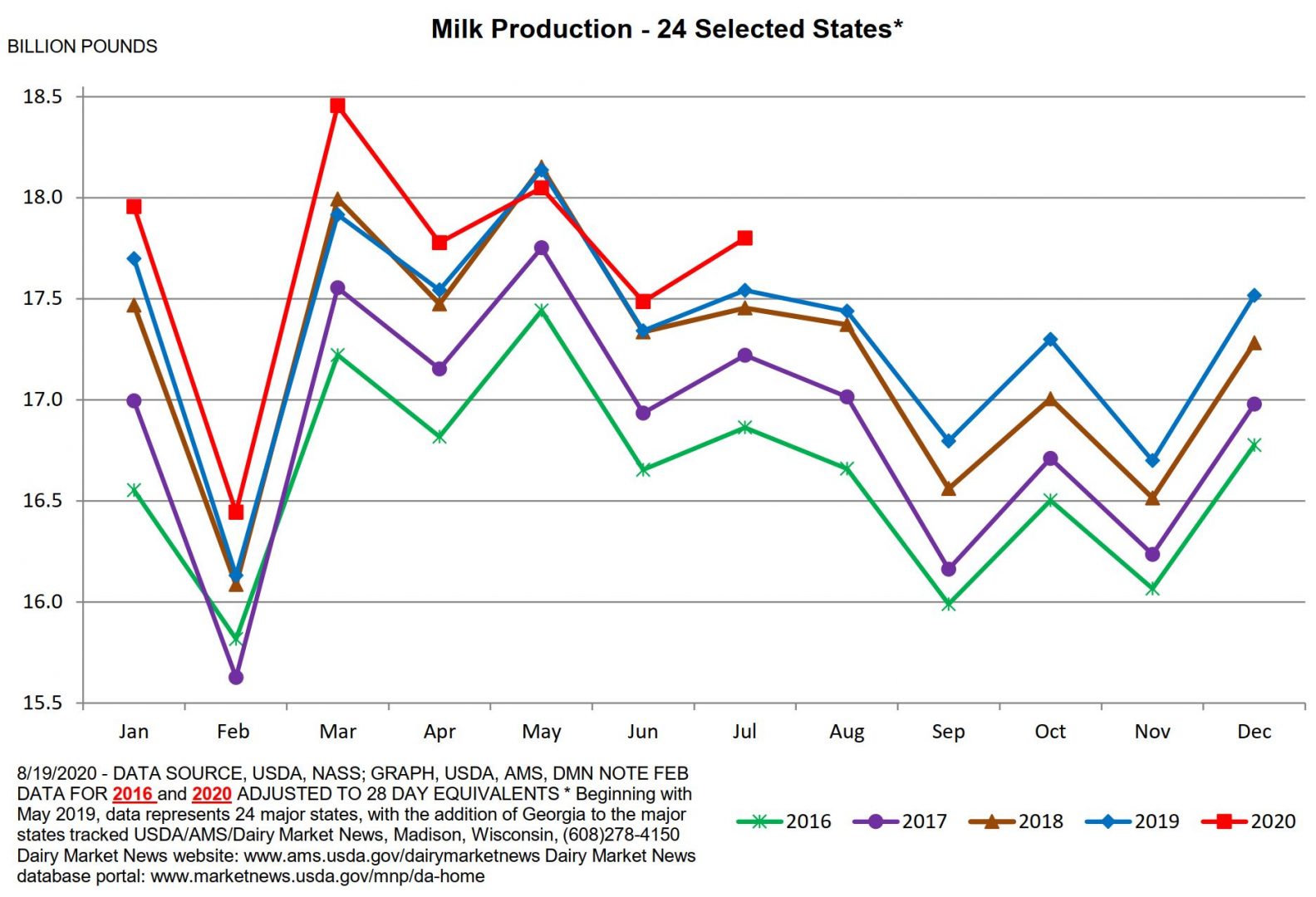

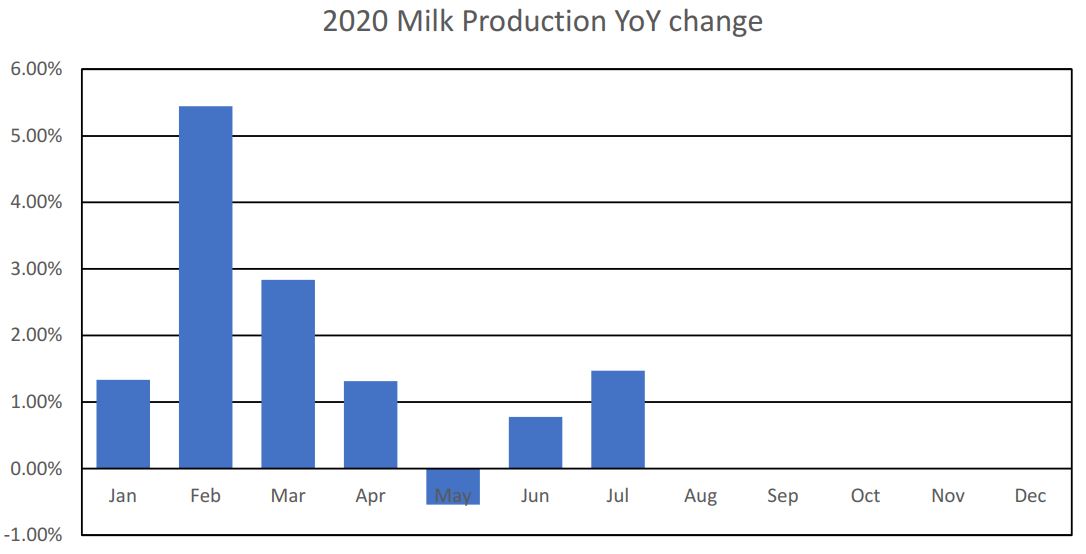

On Wednesday the Milk Production Report was released. USDA revised last month’s June output higher, with July production up 1.5% over a year ago.

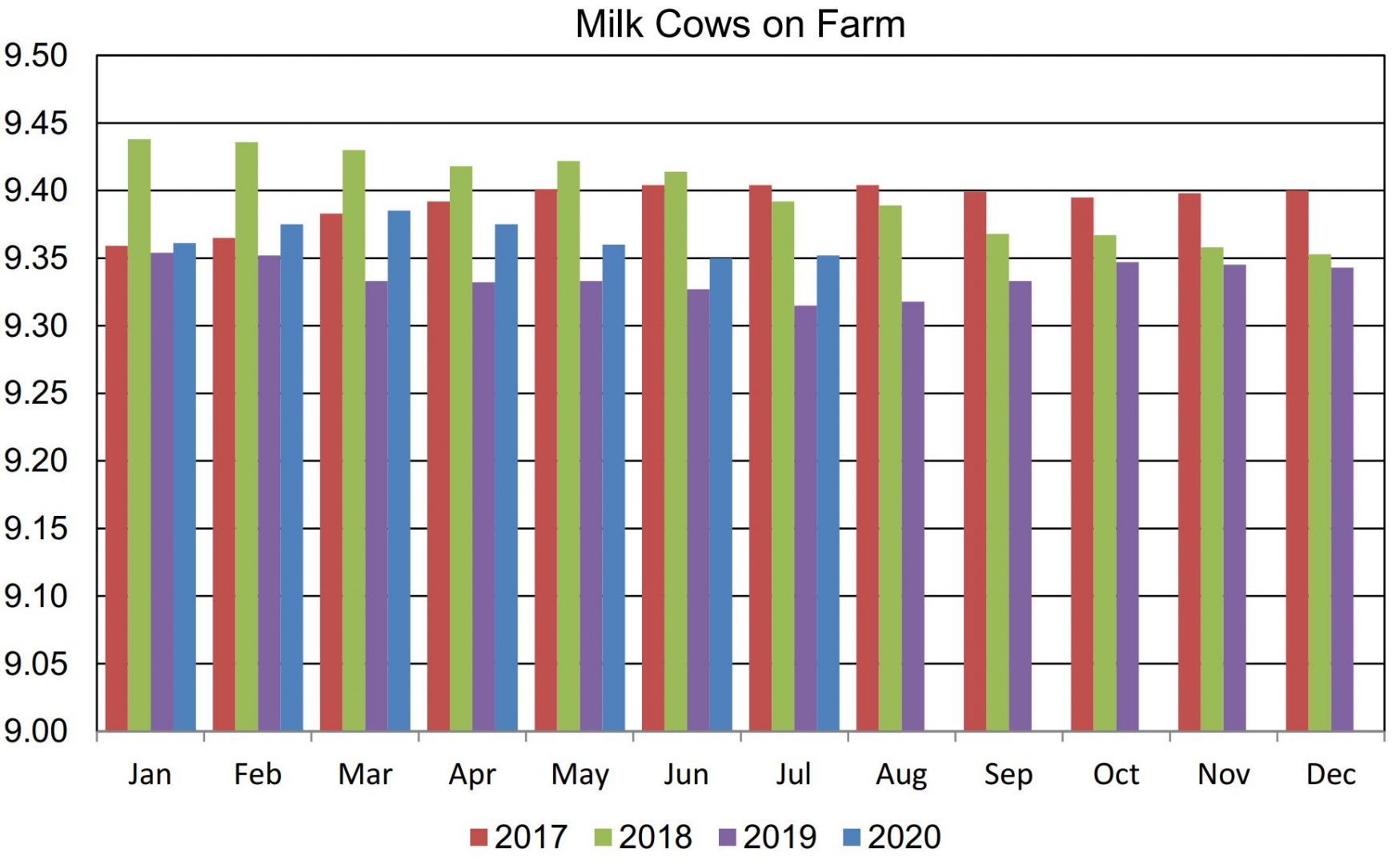

This number was within expectations, but probably the most worrying statistic (though not unexpected) was the fact that the herd size increased 2,000 head from June. This is a reversal from monthly contractions since March. While the total herd size is still below 2017 and 2018 levels, it appears to be once again in expansion mode.

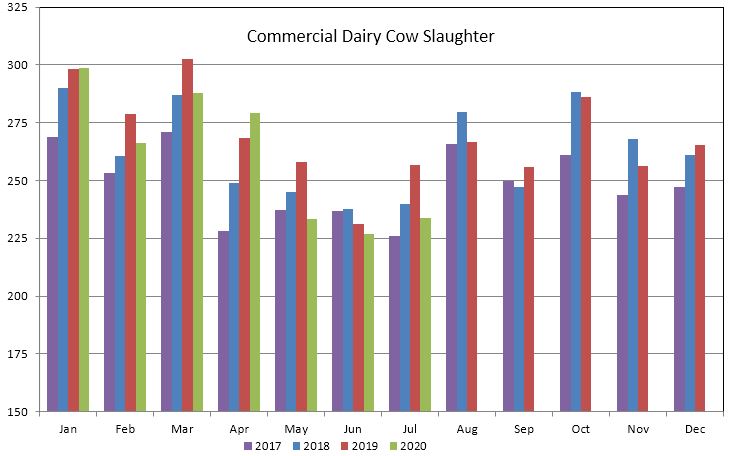

We would expect an acceleration in the growth of the herd size going into the August Milk Production Report due to a sharp decline in culling. The numbers bear it out. Weekly cull numbers have recently been much lower than year ago levels, with the most recent total for the week ending 08/08 down 8.3% vs. the same period a year ago. YTD the weekly numbers are 4.1% (86,000 head) behind 2019. This week’s Livestock Slaughter Report revealed 233,700 dairy cows were removed from the milking herd in July, down 9% vs. a year ago and the lowest July total since 2017.

Dairy Market News reports this week were also largely negative. Cheese production is strong over much of the country while sales have seen some slippage. At the same time, hybrid school openings have resulted in bottling orders down by half, with the extra milk heading into Class III operations. In the Midwest, spot loads of milk traded as low as $5 under Class III. Cheese inventories are not yet an issue, but they are growing, along with concern. For the week ending 08/01, cheese holdings in USDA-selected cold storage facilities grew 2% (1.23 million lbs). Butter holdings over the same period declined 1%. Butter might be the lone bright spot as prices appear to have bottomed out and sales have started to rise for both retail and foodservice needs. Butter manufacturers are expecting a strong fall demand season.

The markets were not kind to Class III futures this week as the brief rally we had last week was more than enveloped with a stronger downside move. The fundamental picture does not look very bright in the short term. Current spot prices work out to just $13.70 Class III. Even assuming NDPSR numbers do not get as low as current spot, September futures are in the crosshairs with a settlement today of $15.13; and that’s down $1.75 from last Friday. Having booked the first week of September pricing, spot cheese prices are going to need to start moving higher in order for Sep futures to continue carrying a premium. We’re not saying that can’t happen, but current fundamentals look pretty bleak.

We do see a few longer term positives though:

1.) Starting in September we should start to see new government solicitations for cheese to be delivered in the 2021 calendar year. No one knows how much yet, so this may or may not be a factor.

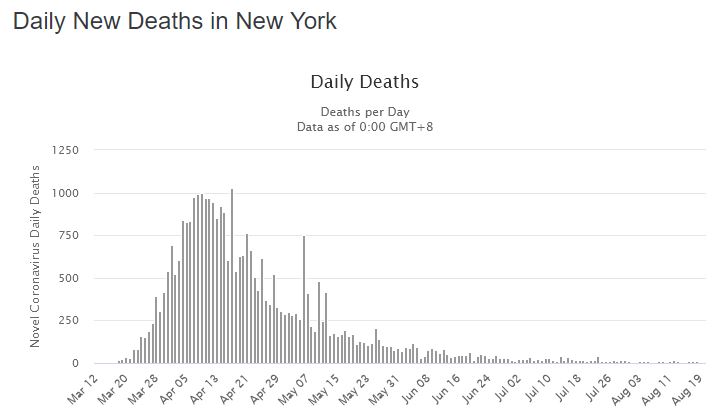

2.) States hit the earliest and hardest appear to be largely done with COVID-19. Case in point, New York, the state with the highest total death toll and which made horrible mistakes in sending infected people to its most vulnerable population in assisted living locations, has seen their daily death rate almost reach zero. Public schools are all opening in this state.

Source: https://www.worldometers.info/coronavirus/usa/new-york/

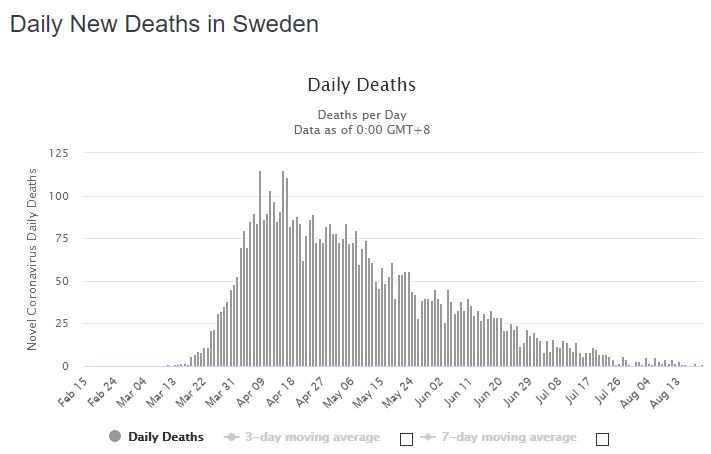

Similarly, Sweden, often ridiculed for their approach, has largely eliminated COVID-19 without lockdowns, mask mandates, closing their borders, closing their schools, or destroying their economy.

Source: https://www.worldometers.info/coronavirus/country/sweden/

What we’re saying, then, is that states currently seeing rising cases and who practiced early distancing, are probably a couple months behind NY. Maybe this pandemic is behind us by Christmas vs. next July. A return to “normal” sooner would certainly help improve dairy demand.

3.) The stock market is pushing to new record highs, some of it on anticipation that COVID-19 is in its final stages.

It’s been a wild 2020 so far and hard to navigate. The increasing herd size is concerning going forward, unless both domestic and export demand get a kick start. Otherwise, lower prices look headed our way. Producers should ensure they have Sep-Dec protected and maybe get a light start on Q1. Technically, September Class III looks like it wants to retest its prior low of $14.51, set on 03/31. Q4 looks like it has some support around $16.25 average, but we would sell a break below that level if that support is violated.

Give us a call next week if you want to discuss the markets and put together a strategy.

Have a great weekend!