06/19/2020

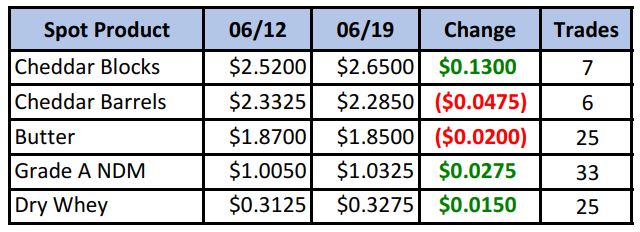

After declining 2¢ on Monday, spot blocks held steady until ripping 15¢ higher on Friday to set a new all–time high record settlement of $2.65/lb. Trading was light for both blocks and barrels as sellers didn’t seem too interested in pushing prices lower, or couldn’t due to lack of product. Spot butter made a mid-week low of $1.80 on Wed, before bouncing back much of the week’s loss. Meanwhile, spot NDM looks like it wants to stay above $1 and even dry whey pulled off a gain for the week, both on decent volume. Speaking of volume, the CME announced that it was increasing max daily volume from 40 loads to 99. Is the spot market preparing for the advent of much higher volume? Time will tell.

Spot Market Recap

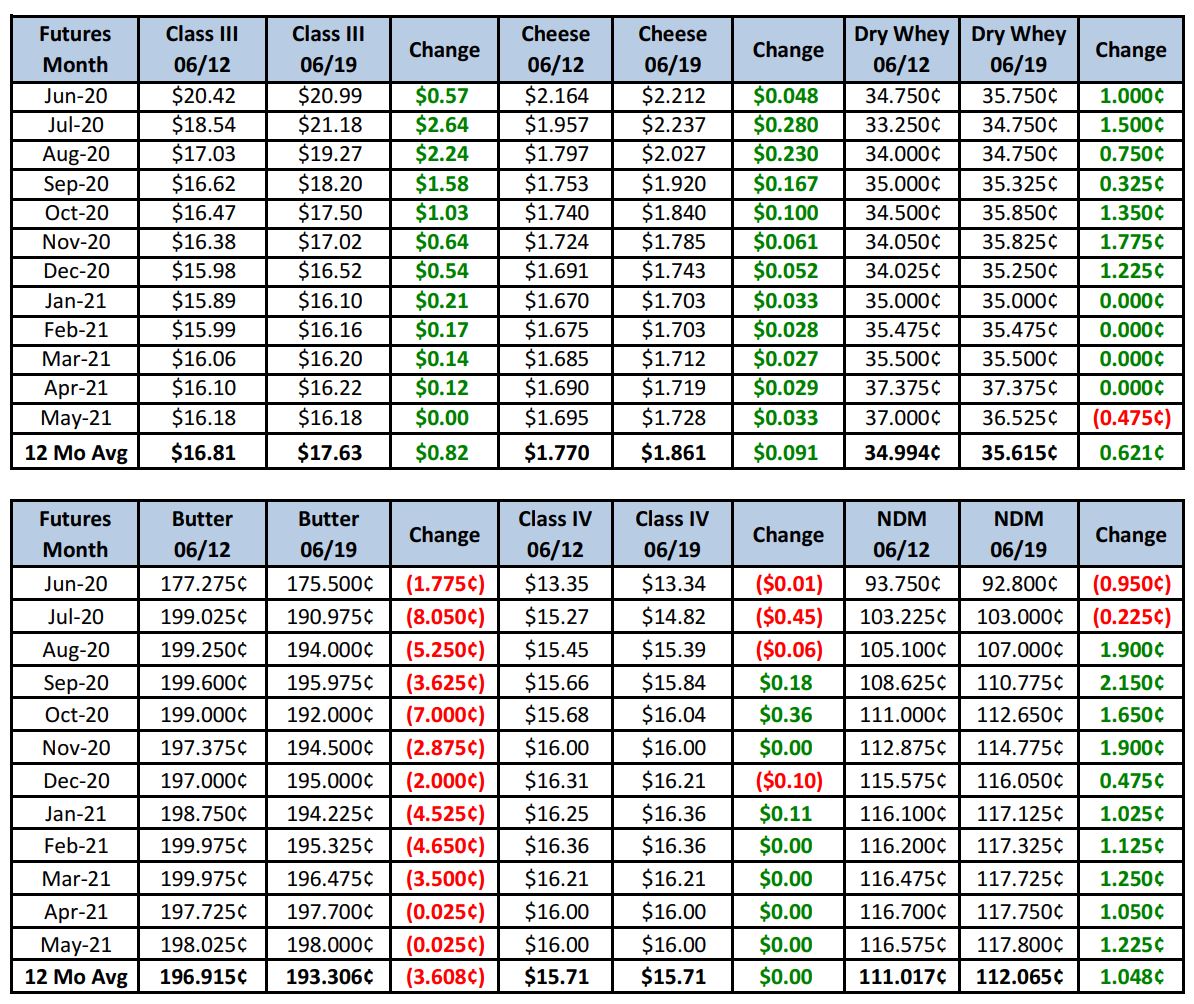

Futures Recap

After writing last week about the technical breakdown and possibility of a bounce, bounce we did, and then some. July and August Class III’s both up more than $2/cwt in a week, with $1+ gains in Sep and Oct.

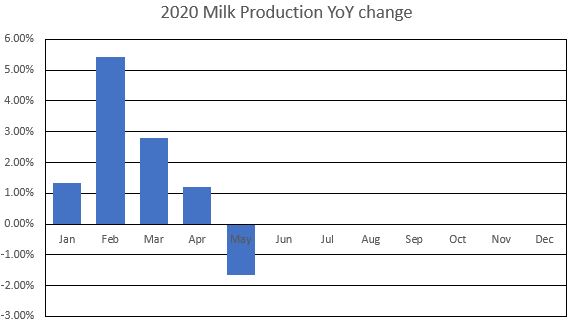

So why the huge rally? Last Friday after the close, USDA announced it was extending it’s “feed box” program and spending another $1.16 billion on fresh produce, meat and dairy. We haven’t seen anything yet on how much will be allocated to dairy, but in the last round (which is still going on), $120 million/month (or about 5% of cheese/butter output) was spent on dairy. That 5% jump in demand from government buying, combined with a decline in milk output from aggressive culling and coop incentive programs, plus the reopening of restaurants has resulted in a perfect trifecta of a tighter milk/cream supply, while demand continues to increase. The new extension on the government program probably means it will last longer. Helping as well was this week’s Milk Production Report, which, while coming in near expectations, confirms what many had predicted. Farmers removed cows and dumped milk. U.S. milk production in May declined 1.1%, the first monthly drop since June 2019.

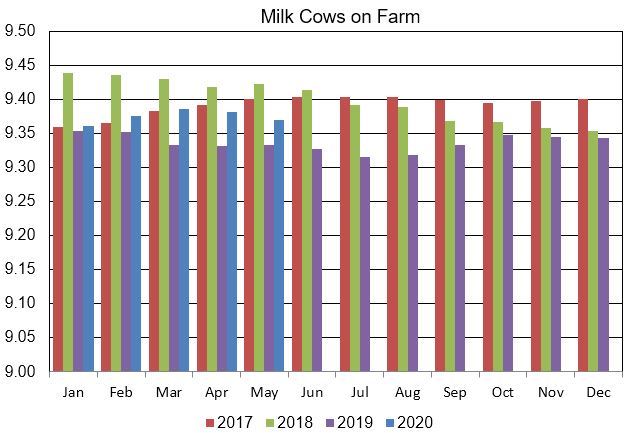

Cow numbers are still 36,000 head higher than a year ago, but fell 11,000 head from April to May, putting the herd back to Feb levels.

Notable declines were cow numbers were seen in key cheese-making states such as WI (-3.1%), CA (-1.5%) and NM (-7.2%).

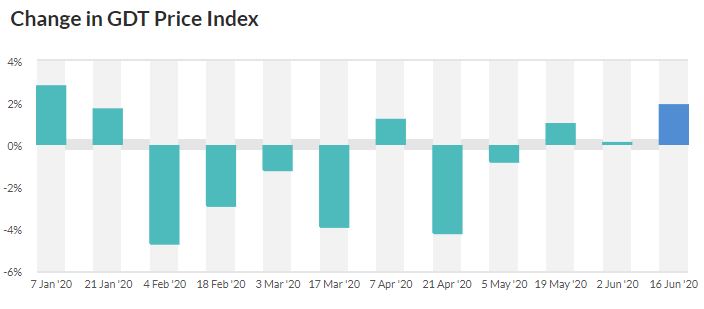

Even the international picture brightened, with the most recent GDT auction on Tuesday seeing the Dairy Price Index rise 1.9%. That’s the 3rd consecutive increase and the largest gain since Jan.

Dairy Market News reports milk output in the NE continues to decline seasonally. Milk is tight in the Mid-Atlantic and bottlers are getting the lion’s share of the milk, with little left for manufacturing. More of the same in the SE, with Class I use dominating milk production. NE cream markets are firm. The Central region is still reporting spot loads above Class. Cream is tight there as well, with both ice cream and cheese plants pulling on supplies. Heading West, in CA, milk output is down and not always enough to fill spot demand. Component levels are declining as well. AZ output is flat from last week, but there is no surplus milk available and processors are running slightly under full capacity. Warmer weather is affecting milk yields in NM and output is flat from last week. Milk output has plateaued in the Pacific NW, with milk supply in balance with demand.

Due to cream being tight across the nation, butter output is lower as it is not cost effective at current cream prices. Some plants are microfixing in order to meet current demand. Retail sales remain healthy. Some butter contacts remain concerned about availability in the fall.

Cheese output across the U.S. is busy, but tighter milk supplies are forcing plants to fortify with NDM. Fresh cheese is especially limited as strong sales are being reported by pizza shops. Current demand is higher than plant output capacity in some instances. There is debate over how long high prices will last as exports have slowed due to being less competitive on price, potentially easing the current tight situation. Others argue tighter milk supplies and and government buying will sustain higher prices. Weekly cold storage numbers suggest the pull on cheese is for real. Stocks at USDA selected storage centers declined by a strong 7% (6.9 million lbs) over just the first 15 days in June.

Current spot prices work out to about $23.64/cwt. With July Class III futures completing just its first week of pricing, there is certainly more upside potential if spot prices hold or go even higher. The sleeper could be August Class III though. If the new government buying program lasts another 30 days, we will be into the August calculation period at some lofty levels, forcing futures quite a bit higher. But current volatility makes longer-term prognostications near impossible. With help from mother nature, we could see high prices well into fall. But if a large player wants to temporarily push down the block or barrel market, they probably can. We’re reading more about COVID-19 hot spots showing up around the country and in other parts of the world. We don’t think they will overwhelm our healthcare system, but if further restrictions are placed on travel and restaurants shut back down, you can bet it will affect our market. We could be in for some real whip-saw action going forward.

Producers/hedgers should NOT try to pick a top, in our opinion. Hedge the front months with PUT options, leaving your upside open. But in 2-3 weeks, if Q4 and Q1 2021 have been pulled significantly higher, you might want to sell some milk there. Let’s see as we get closer.

Have a great weekend!