06/12/2020

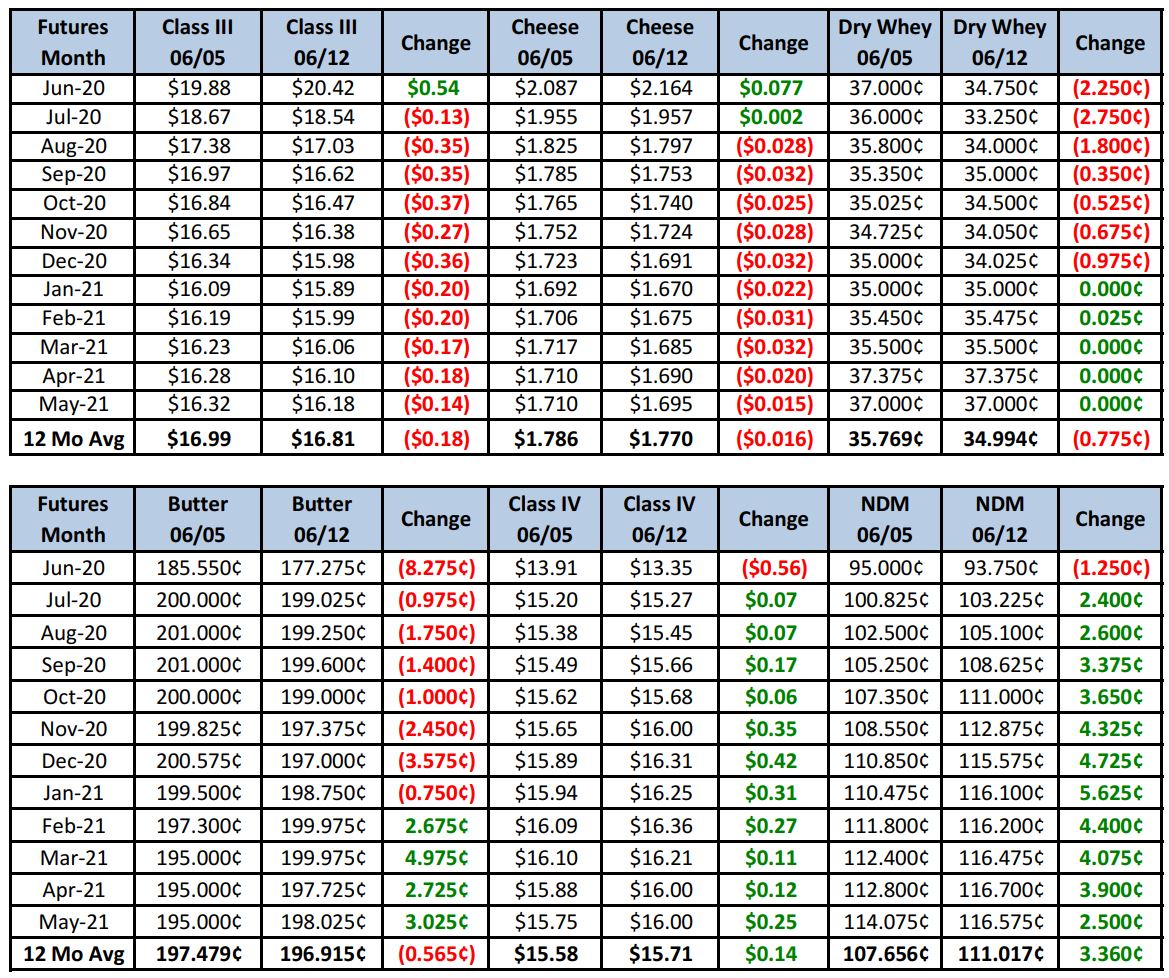

Spot cheese prices saw their first weekly decline since mid-April, and sellers were quick to pounce. Class III futures experienced fairly heavy selling Aug-Dec as hedgers grabbed more coverage. Spot NDM was the sole component settling the week higher, as demand for that category improves.

Spot Market Recap

Futures Recap

The fundamentals continue to paint a rosy picture, but technically, the market has turned short-term bearish. First the fundamentals:

Dairy Market News reports milk output in the NE is lower and supplies are tightening in hotter weather. Milk production in the SE is also declining with most output destined for bottlers. Ice cream manufacturing is strong, pulling on available cream supplies and lending support to prices. In the Central region, some balancing plants are at lower capacity than expected, even though Class I demand is slow. Cheese production is taking the bulk of output, leaving the milk supply rather thin. Heading West, lower milk output in California has resulted in demand outstripping supply. Several milk buyers are looking for loads on the spot market, but bringing in out-of-state milk has been difficult. Arizona milk production is flat, with a seasonal decline in components. Milk is no longer being sent across state lines and the supply is in balance with needs. Even in the Pacific Northwest, milk receipts to plants are generally in balance with needs, and milk is easily finding a home within the region. The cream market is strong as ice cream production is strengthening. Many butter plants are selling cream instead of churning as it is more profitable for them to do so.

Speaking of butter, food service requests are increasing as restaurants slowly reopen. Some processors are microfixing to meet continued strong retail demand. Churning is light due to tight cream supplies.

Cheese supplies are tight in the NE for many operations. Plants are receiving adequate milk supplies to fill immediate orders, but an increase in cheese sales is keeping inventory levels balanced to lower. Demand for aged cheddar from specialty shops is good, and restaurants continue to purchase on regular schedules. Cheese output is active in the Midwest, but spot loads of milk are sparse. Managers in the region say they are using more NDM to fortify production. With prices at or near record high levels, some buyers are starting to push back and are more hesitant on purchases. In addition, some depleted pipelines have now been refilled. But fresh cheese is still moving well. Cheese sales are gaining momentum in the West as food service and government purchases continue to ramp up. Block cheese is described as “very tight”, and cheddar is particularly hard to find. Many processors have their clients on allocation programs, even as they make all the cheese the can. Strong cheese purchases are reflected in this week’s cold storage numbers, with cheese holdings in selected USDA storage centers declining a strong 8% (7.9 million lbs) in just the first eight days of June.

But as good as the fundamental picture looks, we’ve done some serious technical damage that will continue to weigh on the market. Front and center is the July Class III contract, which begins its pricing period next week. As cheese bidders became less aggressive in the spot market, offers began to appear with more confidence, before walking prices down some. We’re still at near record levels, with a block/barrel average of $2.43/lb, but the market is nervous up here (as it should be). July Class III futures finished the week down just 13-cents at $18.54, but that was after an intraday high of $19.85 set just 2 days ago, a gap of $1.31. Many wondered, including myself, why July didn’t justify being priced over $20, considering the nearness of its pricing period and spot prices working out to well north of $23. But the markets are always anticipating the future, and once again they were correct; at least so far. Looking at a daily chart of July Class III futures, there is a strong level at about $18.00, which was prior resistance back in Jan/Feb, and which should now act as support if the bull market isn’t over.

And though we have had a small decline in spot cheese prices, they still work out to about $23.10/cwt. What we’re saying, then, is that July Class III futures are predicting a massive drop in spot prices, to around the $1.95/lb level. That’s still near $2 cheese and still a historically high number, so yes, it’s very possible we see this. But it’s going to need to happen rather quickly. If spot cheese manages to remain stubborn and we see only gradual declines, July Class III futures will be forced to rally hard in order to close the over $4 gap with spot. We have no clue which way this goes, only that something big is going to happen. Either we see a very large decline in spot cheese, or we’ll see a very large rally in July Class III futures. Watch the low $18 level in July Class III, which would be a 50% retracement from the prior low to high, to see if buyers start stepping in. If they don’t, a much bigger price decline is probably in store.

Dairy operations should continue to look at hedging the front months, which are most vulnerable to a large decline in spot prices. Further out we would remain patient.

Have a great weekend!