05/22/2020

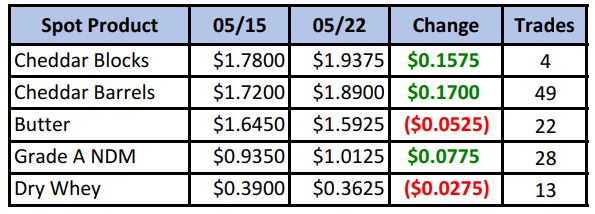

The price of block cheese in the spot market has nearly doubled in 30 days. On April 21st, blocks closed at $1.00¾/lb, but since then has skyrocketed 93¢ to this week’s close of $1.93¾/lb. Barrel cheese has seen a similar rise, with the $1.91 block/barrel average making a new high for the year, reaching its highest level since Dec 2019.

Spot Market Recap

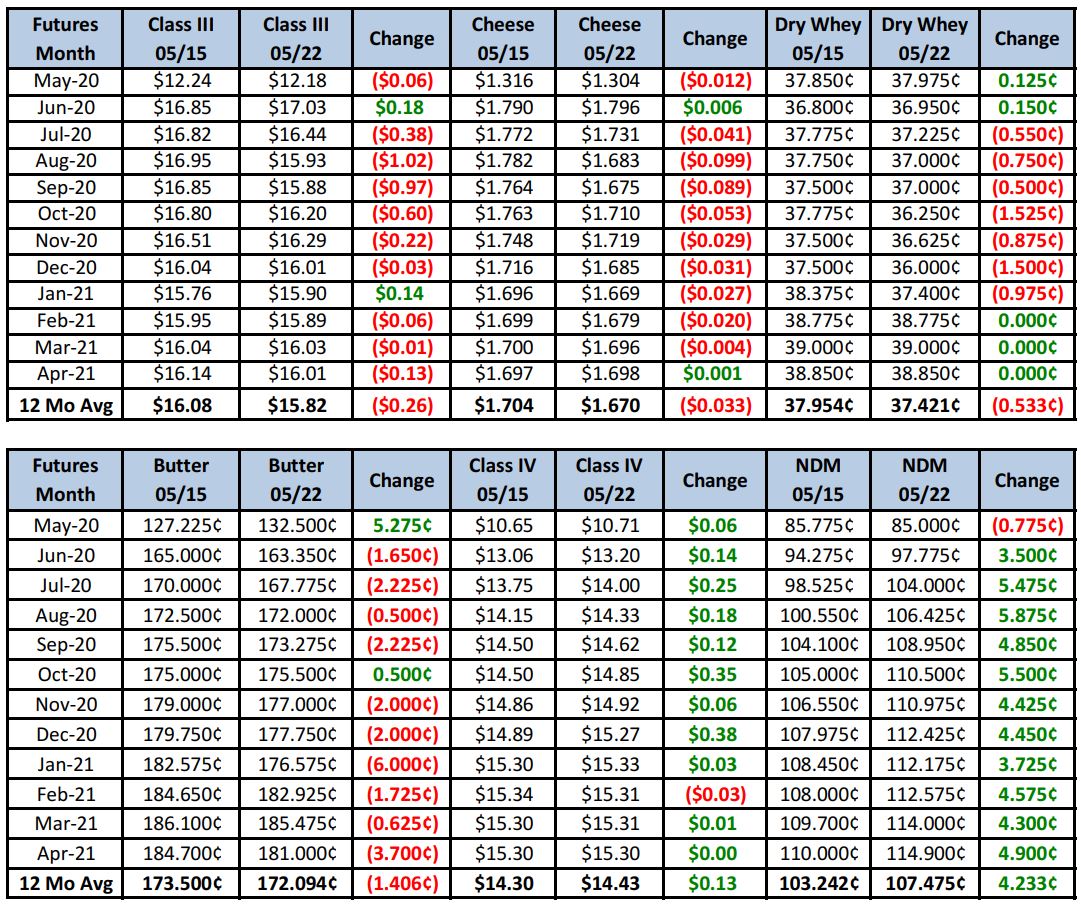

Futures Recap

But unlike the spot market, futures hasn’t had such an easy ride higher. The essential function of the futures market is price discovery, and the meteoric rise in spot cheese prices does not have everyone convinced. Market reports released this week painted a more negative fundamental picture.

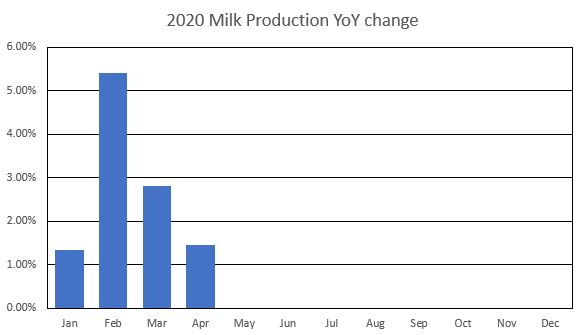

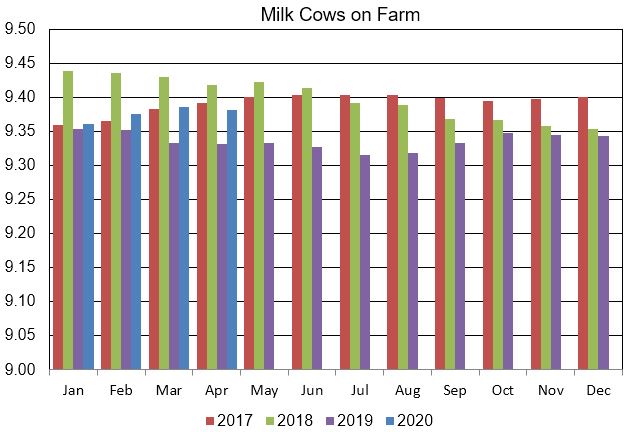

Milk Production in April increased 1.4% while cow numbers decreased only slightly from the prior month, but were still 50,000 head higher than a year ago.

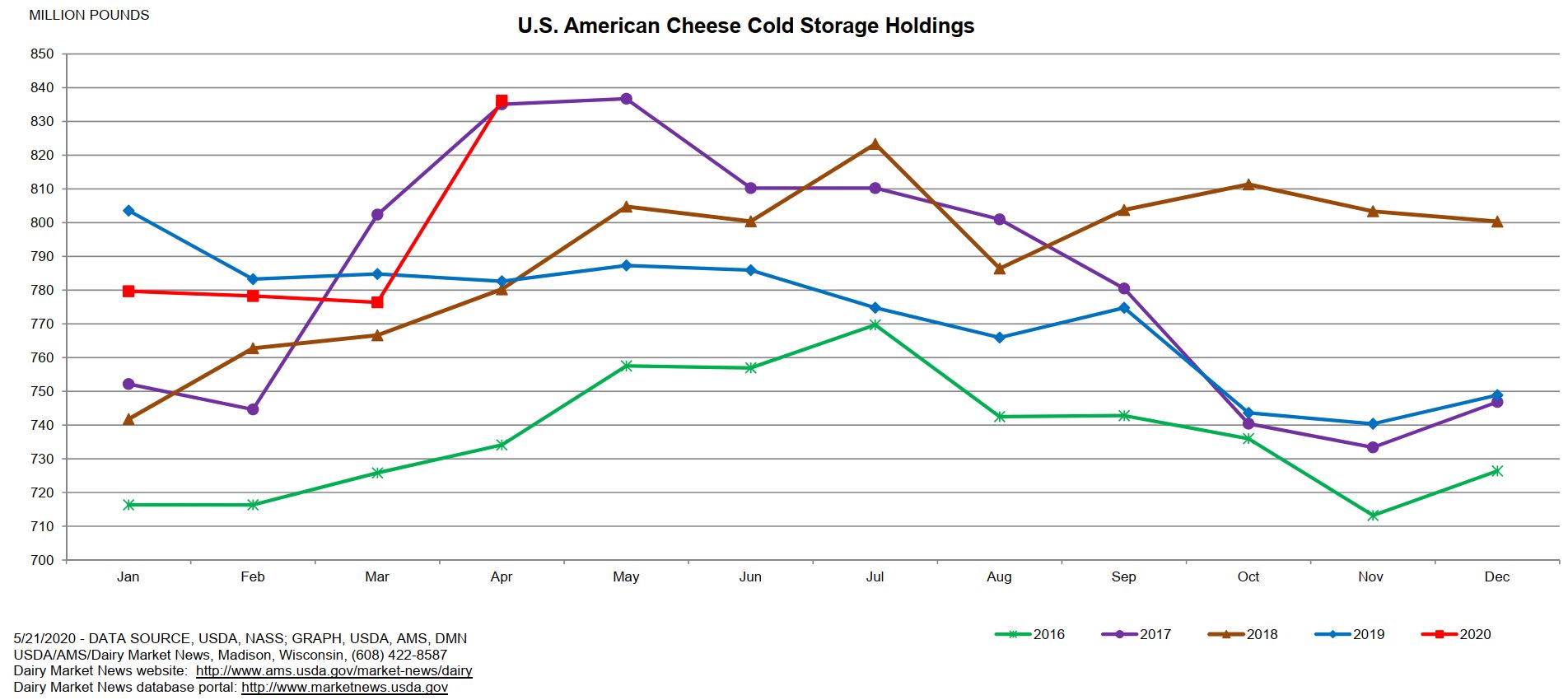

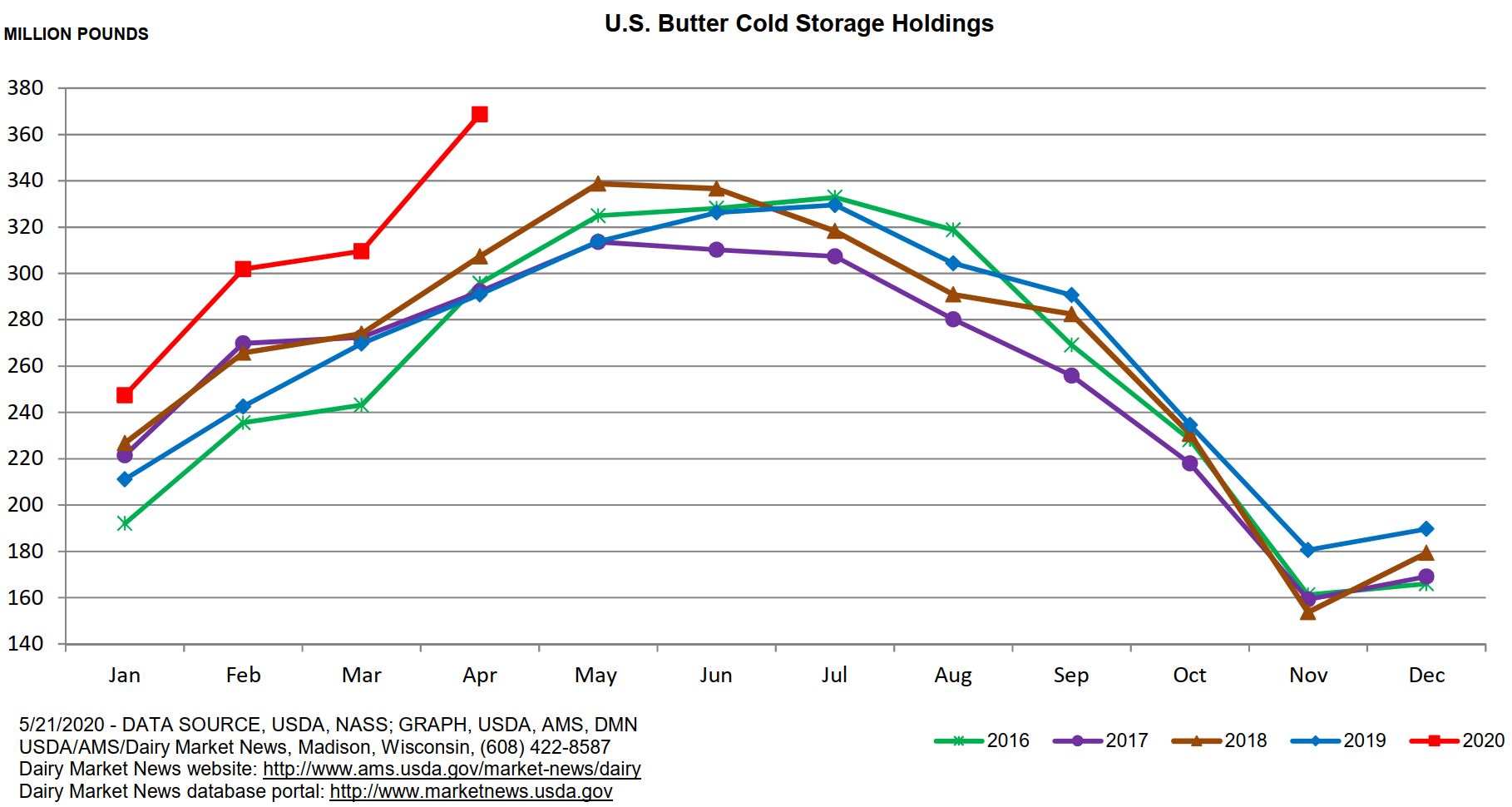

The Cold Storage Report reveal a substantial increase in American Cheese stocks in April to a new record level, while butter stocks, already at record levels, moved even higher.

But, most of this data was either early on in milk/herd reduction incentives and before the large government purchase announcements. How things have changed!

Dairy Market News reports this week the fluid milk is continuing to tighten in the Northeast and is already tight in the Mid-Atlantic. Most milk is heading to Class 1 needs, leaving less for other classes. Milk output is dropping in Florida as warmer temps take a toll on cow comfort. As a result, suddenly cream is scarce in the region. Contacts in the Central region report milk output is atypically lower, a result of increased culling. Components also continue to lag. For the first time this year, there were no spot loads of milk offered at a discount to Class 3, and cheese makers report milk availability has gotten thinner by the week. Cream supplies have also tightened as pulls from ice cream manufacturers continue. Heading West, milk output in CA, AZ and NM is continuing to decline, and overall, milk supplies are very manageable. Finally in the Pacific Northwest, milk is in good balance with processing needs, with plants running normal schedules. Despite the bearish Cold Storage figures, the butter market continues to slowly recover, with improved sales to restaurants and strong demand at retail. The news is even better in the cheese department, with contacts in the East relaying inventories are back to healthy levels. Food service demand is improving with the gradual reopening of restaurants, while orders from Eastern pizzerias and Italian restaurants is strong. In the Midwest, there is even concern from some cheese producers about falling behind current customer demand. The cheese market tone is bullish on improved sales and a tighter milk supply which no longer carries any discounts. Finally, Western cheese plants report that, while warehouse inventories are still heavy, improved demand from food service and government purchases has most of the supply already committed. Buyers are finding that prices are now much higher. NDM prices have firmed across the country, with spot NDM getting back up over $1.00. Active buying from Mexico and less available milk are contributing factors. In addition, with the surge in cheese prices, cheese manufacturers are looking to buy more NDM for fortification.

Based on contacts we talked to this week, we were a bit surprised to see the fierce sell-off on Friday. The 25 loads of barrels that traded in today’s spot market indicate there are holders of product ready to let go at the right price. Will buyers continue to show up next week? Continued government buying, improved food service demand and tighter milk supplies will help, but today’s correction is a reminder that there are always corrections in bull markets.

Last week we commented that increased volatility would provide hedgers with a great marketing opportunity. For those that took advantage of the spike higher this week, that held true. But we think there will be more opportunities going forward. One consequence of government involvement in our markets is the skewing of normal supply and demand signals. That is certainly the case now. We are also growing more concerned about another consequence of government involvement in the form of direct payments to dairy operations. For some it is a lifeline to keep running, but we also know that some operations are going to do exceedingly well and will be looking to expand as a result. 2021 milk prices could be setting up for a drop if domestic and global demand is unable to increase at similar levels. For this reason, hedgers may want to consider beginning their 2021 marketing with some light sales for the year at the current average of $16.22. When faced with the possibility of sub $11-12 milk just a few weeks ago, this looks like a decent hedge. For some, a $16.22 base price would yield over $17/cwt mailbox with components/quality premiums. Let us know if this is of interest to you.