5/5/2024

Cheese held gains this week as strong demand in the Midwest region kept sellers out of the spot market. End users are fill the pipelines for the summer and fall needs. This has tightened current inventories and move the spot price higher. With a smaller dairy herd and a good chance for sustained heat this summer, production is likely to be lower. The question going forward will be can the current demand keep cheese tighter into the summer heat or will this just be another head fake that producers should be selling into.

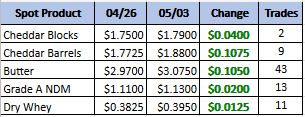

Weekly Spot Prices

Weekly Future Prices

Cheese: Cheesemakers continue to relay steady to stronger production schedules across all regions. The March Cold Storage report released last week revealed that March 2024 natural cheese stocks were up slightly from February 2024, but down from March 2023. In the Northeast, cheese inventories are said to be comfortable. Retail cheese demand is steady in the region. Cheese manufacturers in the Central region say demand is strengthening. Some processors shared having to turn away customers. Some contacts shared requests for

cheese volumes beyond what a customer has already contracted may not be able to be accommodated. Milk availability has tightened in the region. In the West, cheese manufacturers share strong production schedules. Milk volumes are available for Class III processors at the moment, but contacts indicate milk availability may tighten in the upcoming weeks. Cheese inventories are comfortable. Domestic cheese demand is said to be stronger, while international demand is steady. (USDA Cheese Highlights)

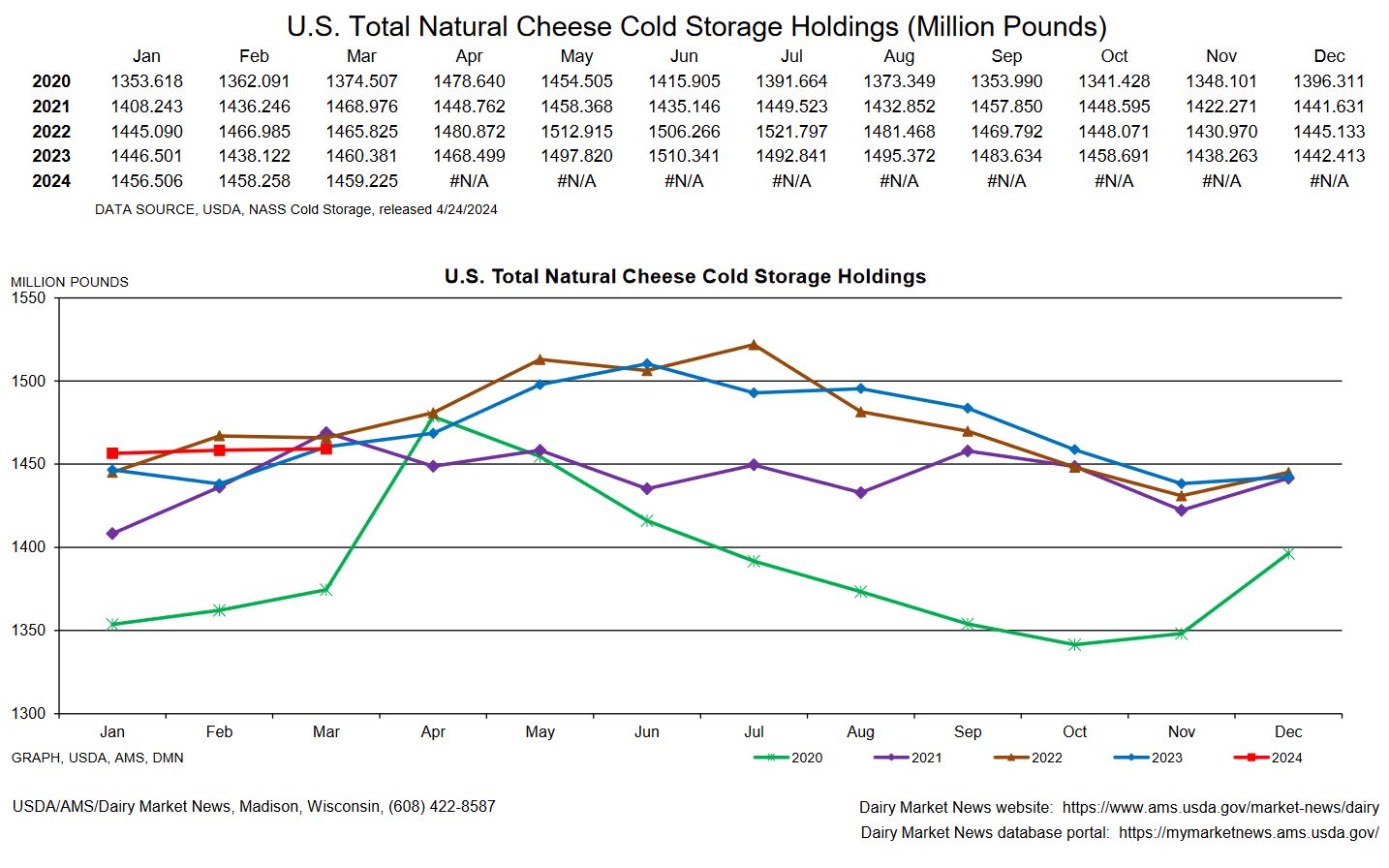

Butter: Domestic butter demand is generally steady from retail and food service sectors. However, for unsalted butter loads, demand is stronger. Cream volumes are comfortable across the nation and able to accommodate manufacturing needs. In the West region, butter production is strong. In the Central and East regions, butter production is steady. Some butter makers have tight availability with unsalted butter loads for spot buyers. In the cold storage report from last week, March 2024 butter stocks were up 6 percent from February 2024 and up 2 percent from March 2023. Bulk butter overages range from 2 to 10 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Dry whey prices moved slightly lower for both ends of the range. The mostly price series was unchanged. Cheese making remains busy, which is providing plenty of liquid whey for drying. Manufacturers convey steady production schedules. However, some producers anticipate lighter sweet whey production to increase as whey protein concentrate production capacity issues are worked through. Some manufacturers have the majority of their anticipated Q2 sweet whey production committed to established obligations. That said, loads are available to accommodate needs of contract and spot purchasers. Demand from domestic buyers is steady. Export demand is moderate. (USDA Dry Whey)

Demand is picking up as buyers look to fill pipelines going into the summer grilling season. Cold storage shows cheese demand keeping inventories in check as 2024 marks one of the slowest increases in cheese storage in the last couple of years. I this mostly to due with a drop in production as the dairy herd has shrunk. This has spird buyers into the market in the last couple of weeks and pushed the spot prices higher then they have been sense last September. Recommendation, sell the first couple of months and look to do put spreads further out. Volume on the spot market has slowed down this last week and it is currently pricing in the low $18s. Therefore, without renewed buying interest $19 class 3 looks like a sell.