04/03/2020

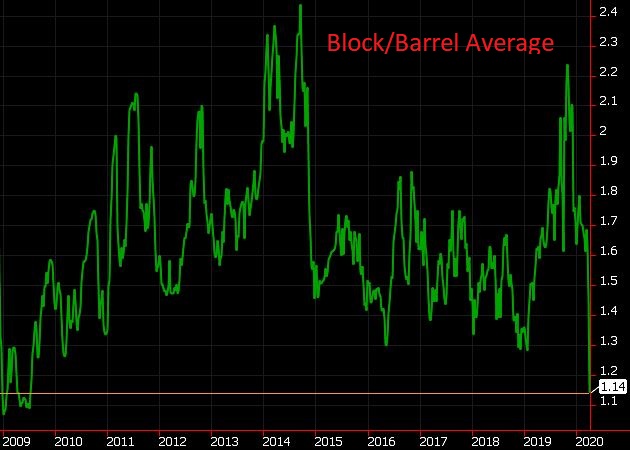

If last week’s drop in spot prices was sensational, it was only working up momentum for this week. Cheese and butter prices were crushed back to levels not seen since the era of $9/cwt milk in 2009. The premium blocks carried to barrels was squeezed to a mere 1¼¢ as the block/barrel average settled at $1.14/lb, last seen in July, 2009 (see graph below).

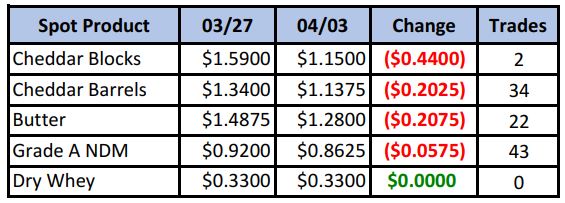

Spot Market Recap

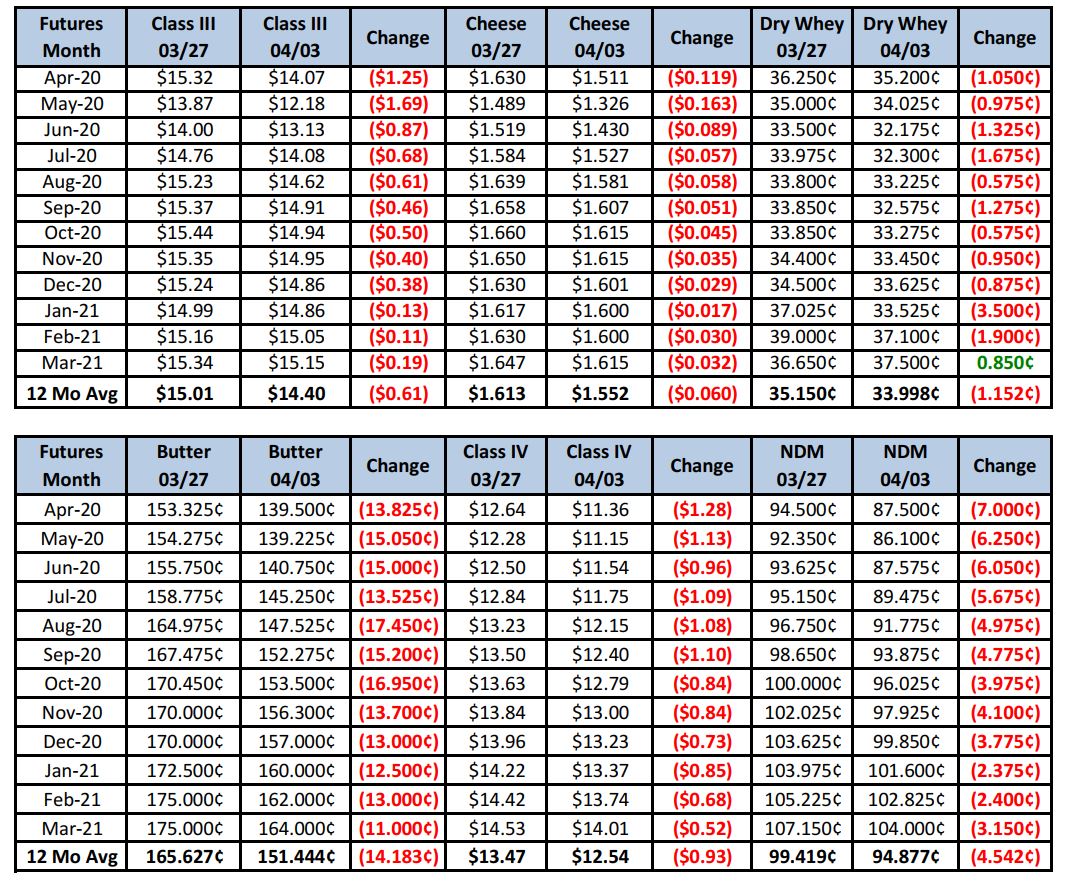

Futures Recap

April and May Class III futures were the biggest losers, but all of the 2020 contracts suffered large declines. Butter futures as well saw rare double-digit losses for the week. Current spot prices work out to about $10.55 Class III and $10.67 Class IV. With the May calculation period looming in about a week, May Class III futures touched limit down a few times today before settling just above that level at $12.18. Even so, if cheese prices can’t find any traction or fall even more, May will be headed much lower and will drag the nearby months along.

While the initial reaction in America was to binge shop for essentials, leaving us to think that demand to restock would support prices, the almost overnight drop of food service demand to near zero from restaurants is not being offset by increased retail demand. One specialty cheese plant we work with is indicating sales have completely fallen apart. Rumors last week turned into news stories this week that dairies are now being asked to dump a percentage of their milk. We can confirm this through clients of ours from CA to WI. Meanwhile, cheese buyers we spoke to said cold storage is getting full. It will not be long before warehouse availability becomes scarce. The bottom line is the dairy product line is like a garden house that someone has kinked (demand), so it has backed up very quickly.

Dairy Market News reports this week contained nothing positive. Milk output continues to increase across the country seasonally as we head further in to spring. Processors of all types: dryers, churns, vats, are all running at or near capacity as Class I sales have leveled off. The Dairy Products Report was released this week and didn’t help either. After adjusting for the extra day this year in February, butter output increased 5.2% vs. Feb ’19, while American cheese output was up 2.5%.

We’re not suggesting selling at current prices, yet it appears we will be heading for quite a tough spell in the near term unless something changes. Weekly cow slaughter levels have been lagging last year. Through week 14, dairy cow slaughter is down 38,500 head (-4.1%) compared to 2019. As more farms continue to dump milk, farm paychecks are going to be hit with a double whammy of low prices and the shared pain of lost revenue. We would expect the cull rate to increase dramatically over the coming weeks if the ship does not right itself.

On the economic front, the stock market fell 23% in Q1, its worst quarter EVER. Unemployment claims jumped by nearly 7 million this week while non-farm payroll numbers fell 700,000, and this was just the start of the impact of the economic slowdown. Until the “re-opening” of the economy is started, expect those numbers to grow and milk prices to remain near multi-decade lows.

Stay safe out there.