04/09/2020

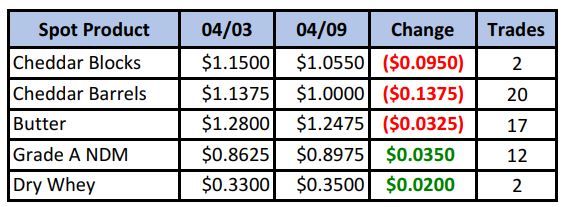

Gas can be bought for 99¢/gal in some parts of the country, and apparently cheese can too, with a load of barrels trading under $1/lb during Thursday’s spot session. The block/barrel average pushed in to new lows, settling at $1.03/lb, a level not seen since February, 2003.

Spot Market Recap

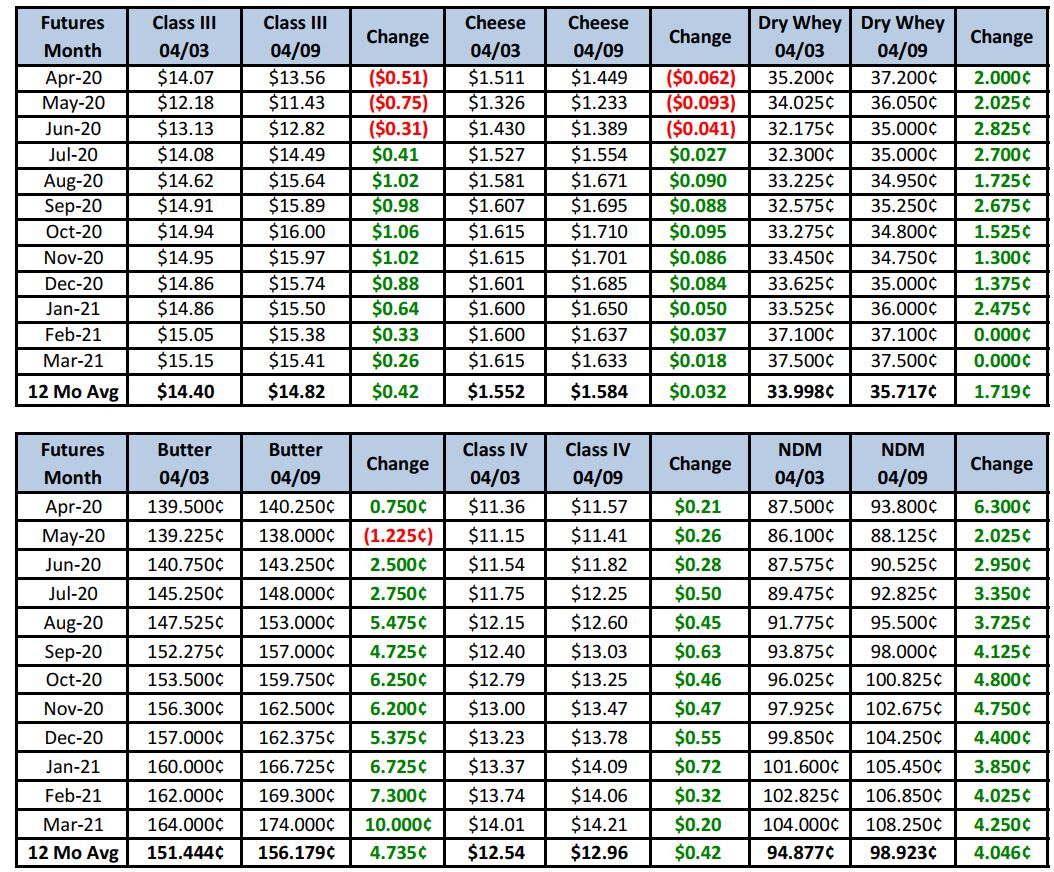

Futures Recap

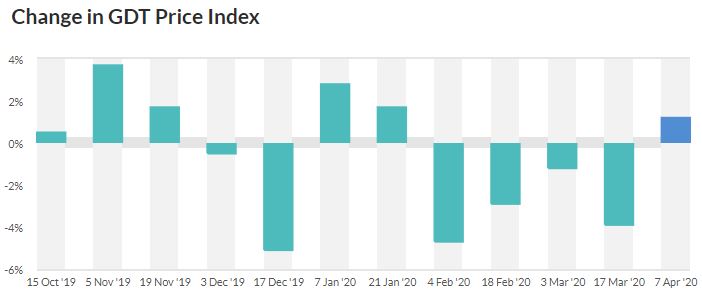

There was a GDT auction this week, but it seems divorced from reality. The dairy price index increased 1.2%, its first move higher since the Jan 21 auction. Cheddar cheese gained 0.2% to a US-equivalent $1.99/lb, which seems laughable in light of domestic prices at almost half that level.

Processors the world over are trying to adapt to the new reality of higher “in-home” consumption against a massive food service decline. A joint IDFA/NMPF proposal to supplement dairy income suggested that current supply is 10% higher than demand. It also included an incentive to reduce the herd by a similar percentage to address the imbalance. Markets reacted with extreme volatility, seeing both a limit up day in reaction, followed by a limit down day as spot cheese careened to new lows. Overall there is still a lot of pessimism. Milk production continues to increase seasonally keeping plants running hard. More milk is being dumped. Cull cow prices have plummeted, so even those looking to raise some quick cash will be disappointed. Rabobank released its quarterly update, suggesting dairy will experience three waves of market movement over the coming year; panic-buying (probably already over), followed by muted retail demand, and finally long-term loss of purchasing power by the consumer. That may happen. On the economic front, the number of first-time unemployment claims jumped to 6.6 million, up from an expected 5 million. The longer the “safer at home” policy lasts, the deeper the economic damage being done. And market watchers point out that even after the “all clear” occurs, behaviors will have changed. Sit-down restaurants will not get the foot-traffic they had prior to the crisis. People will be more cautious, at least for awhile, until there is either a vaccine (many months away), or the number of new cases drops very, very low. For that reason, Rabobank expects a difficult period for dairy markets through Q1 2021.

Despite the drop in spot cheese prices to new lows, most dairy futures finished the week well in the green, due to the initial sell-off being so violent last week. In fact, almost mirroring the stock market, July-Dec Class III has bounced almost half way back from the most recent high. At $15.62/avg, it briefly pushed above the $16 level before settling back down. That will now be an area of resistance until a push and settlement above. Producers who can cash flow at $16 base price should consider getting added protection around that level July-Dec, if they have milk yet to hedge. Up front things look nasty. Current spot prices work out to just $9.50 Class III. Yes, $9 milk may be back, which seems inconceivable. We stated last week that the May contract could see a significant drop, due to its proximity to starting its calculation. It settled down $0.75 for the week, but could see even more significant declines if cheese prices cannot gain any traction. And not as much milk is currently covered under the DRP program as when it was initially launched. As of the end of March, less than 30% of the nation’s milk supply had coverage. That could mean very difficult days ahead for those who are open to market prices. A wildcard, of course, could be further government intervention in the dairy markets, but there seems some reluctance so far to do so. The proposal mentioned earlier does not seem to have gained any traction, at least from what we are hearing, but who knows.

Despite all the trials, we are reminded that this is Easter weekend, a celebration for many of the faith. May you and your family be blessed this weekend,

Note: Markets will be closed tomorrow in observance of Good Friday.