01/24/2020

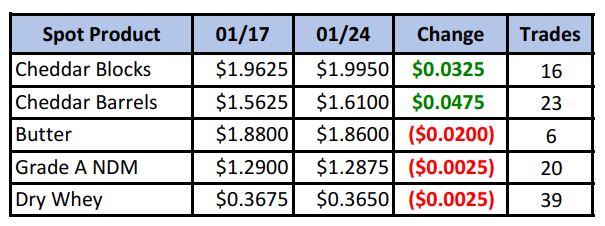

Both blocks and barrels finished the week higher, as unusual, anti-seasonal buying behavior continued in the spot market. Some chinks in the rally may have appeared, however, as Friday’s settlement saw a decline from Thursday’s highs. Volume was heaviest in dry whey, perhaps an indication of improving demand from China.

Spot Market Recap

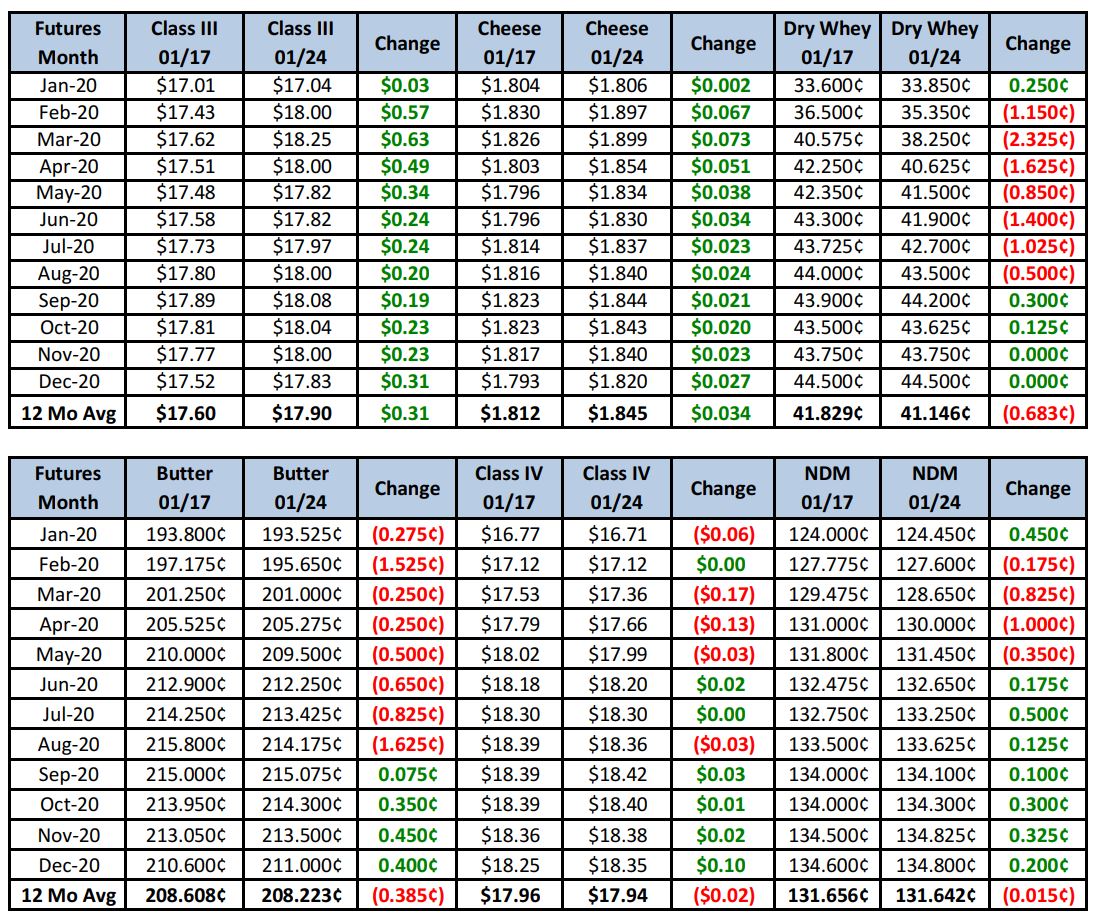

Futures Recap

After showing some bullish technical signs last week, the market roared to life this week, with the annual average gaining a stunning 31¢ to close at $17.90 average. Feb-Apr saw the highest daily trade volumes and biggest gains as bidders were relentless in their efforts to build a long position. With milk production and components picking up across the country, and just after the holidays, this is very unusual price action indeed. Digging through our network, we heard various explanations. There are rumors that an Australian company was/is buying barrels due to lack of supply, reports of milk production issues in New Zealand and India, and the fact that cheese sales are just darn good for this time of year. There is some evidence of strong sales. Dairy Market News reports that some Northeast cheese makers’ Class III sales are fully committed, despite higher milk volumes and stronger cheese output. We spoke to a large plant in the Midwest that also confirms sales of their upper-tier cheeses are strong, which limits their ability or need to make cheddar. The West seems to have the most regional cheese availability, but sales for both blocks and barrels are described as “active”. Wednesday’s “Weekly Cold Storage Holdings” report also reflects strong cheese demand. Stocks at selected storage centers have declined a strong 9% (7 million lbs) over just the first 20 days of January. Butter output remains very active across the country as cream volumes are abundant. Stocks are more than adequate to meet most needs. Dry whey output is increasing alongside growing cheese production, but buying is active and more export interests for Western U.S. producers has relieved some overall pressure on the market elsewhere in the country.

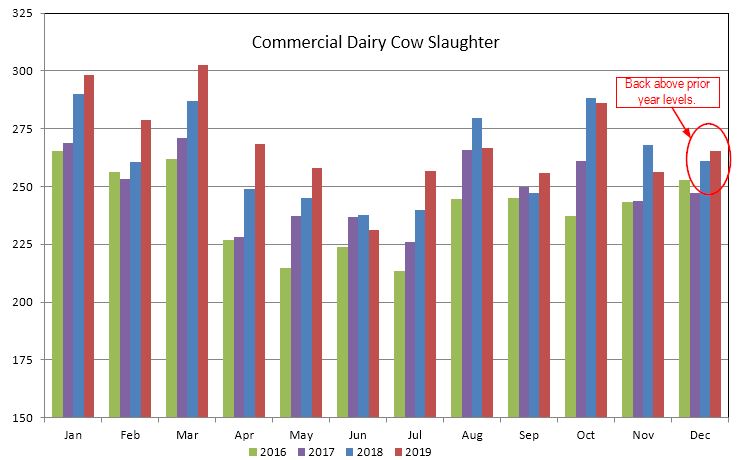

Several USDA reports were released this week as well. The Livestock Slaughter Report revealed the dairy cow cull for December was exceptionally strong. 265,400 head were removed from the milking herd during the month, up 1.6% over December ’18 and the highest December total since at least 2006. It was also the first time since September that levels were above the prior year.

The Cold Storage Report was a mixed bag for the markets. Butter stocks at the end of Dec were 6% higher than the prior year, but American cheese stocks were 7% below year ago levels, while total cheese stocks were down 2%. The report was interpreted as price negative for butter, but price supportive for cheese.

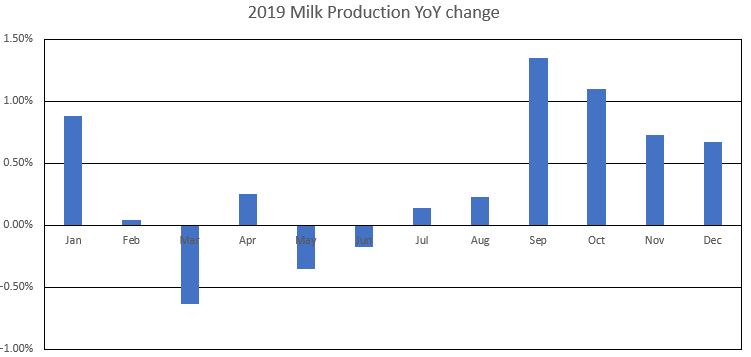

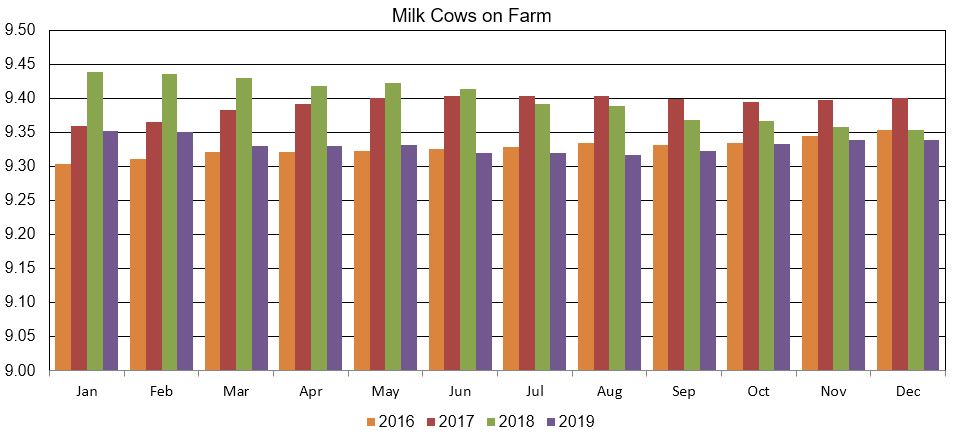

Finally, the much anticipated Milk Production Report was released Friday afternoon. December milk production in the U.S. was 0.7% higher than Dec ’18, while cow numbers were unchanged from Nov. At 9.339 million head, the herd at the end of Dec was 14,000 head smaller than a year ago.

The report for both cow numbers and production came in below expectations so was viewed as price supportive. Worth notice as well was the fact that output in Wisconsin declined 1.1% on 8,000 fewer cows and 10lbs lower milk per cow. Feed quality issues as well as continued small farm closures are continuing to affect the America’s Dairyland, and will likely limit growth in cheese output.

On the macro front, the discovery of coronavirus and its potential spread, and the fact that more than 40 million people in China are on lockdown had a negative affect on the stock market and the energy sector, as it’s seen as a hit on travel and consumption, right when China celebrates the New Year. That seemed to drag grains lower as well.

With all that going on, today’s sell off may be corrective in nature. Cheese demand appears to be very good. We’d expect some ups and downs over the next month or so as we head in to peak production in the U.S. There will be no shortage of milk for processing. But if the economy and demand remains strong, we could be set up for a Q2 and beyond rally once we get through the flush. For that reason, we think further downside in the short term is likely, but limited, and may serve as a buying opportunity for long hedgers. We would recommend dairy operations sell rallies in Q1, but use DRP and/or PUT options Q2 and beyond to leave their upside open.

Have a great weekend!